There's a 50%-margin monopoly hiding inside the airline industry that'll print cash for the next ten years

DISCLOSURE: You’ll walk away from today’s article with a framework, a new thesis and 3 actionable stock trades.

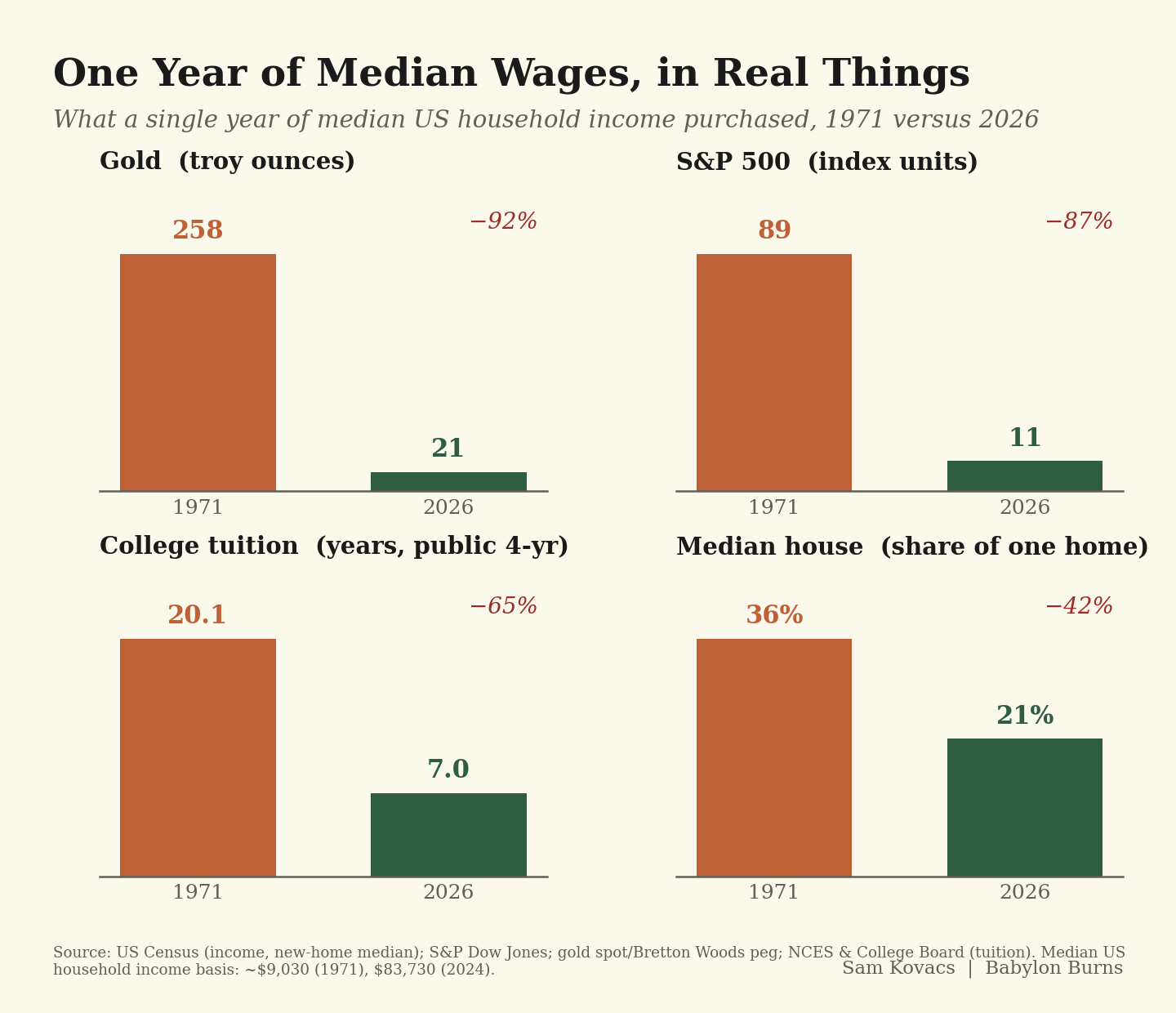

Mark Twain quipped that you should buy land because they ain’t making any more of it. That’s unlike dollars, which they never stopped making more of.

On August 15th 1971, Nixon abolished the gold standard and ushered in the era of fiat money.

This marked the beginning of money being printed in excess of growth in the real economy.

Whilst in 1971 a household’s median annual wages could buy 36% of the median American house, today that number is down to 21%.

The household’s wages could buy 89 units of the S&P 500 in 1971, only 11 today.

The Household could buy 258 ounces of gold, or pay for 20 years of public college tuition, vs 21 ounces and 7 years today.

To make it worse, a household today works 30% more than in 1970s. More women have joined the workforce, only for the household to be worse off still.

Now of course, this is good for those who own houses, stocks, gold, and operate universities. And not so good for those who save US dollars (or any of the other major currencies by the way).

It’s because when they print money in excess of what is needed to grow the economy, they reduce the value of money. It’s as simple as that.

But, there are things which cannot be printed. Things that are relatively scarce

Scarcity is the heart of economics. Price is set where supply and demand meet. If demand is scarce relative to supply, price craters, if supply is scarce relative to demand, price explodes.

It is why, in last week’s article within which I presented my framework, resource scarcity, is identified as one of the secular themes which will dictate the regime within which we are.

Resource scarcity evokes oil, lithium, gold. And those are all interesting, they are geological scarcity.

The discussion then often segues into Bitcoin, Swiss Francs, or any other discussion on sound money.

And that is fine. To be clear, I love the idea of Bitcoin, what it represents and its potential. But it is an asset which can only be traded only on sentiment. And sentiment, through price action, currently shows a textbook distribution, along with the price dipping below both its prior cycle all time high, and below its 200 week average price.

The risk reward isn’t anything I’m excited by here.

Which is the point I want to make: investors shouldn’t be married to an asset, but they should be married to the ideas which made that asset desirable. In this case it is scarcity.

And I think that investors should take the following frame:

When there is an enforced control point which prevents supply from expanding to meet demand, there is scarcity.

That scarcity can be structural (Rolex or Hermes keeping supplies tight to manufacture high prices) or it can be tactical (DRAM prices exploding as demand moved faster than you can build fabs).

Identifying sustained scarcity which hasn’t been priced, is a great way to produce returns.

Today I will walk you through an industry which has structural demand and faces scarcity throughout the next decade: the aerospace after market.

The aerospace after market

“The engine is the heart of an airplane, but the pilot is its soul." - Walter Alexander Raleigh

Whilst the quote above is undeniably beautiful, the truth is that there is an oversupply of entry level pilots.

Commercial aircraft on the other hand, are not so plentiful.

My wife and I get to fly quite a bit. In any given year, we might spend between 7 and 10 days (200 to 240 hours) in airplanes.

Below is my 2026 H1 summary, which at the very least, should reassure you that you are reading global macro commentary from someone who has seen a fair bit of the globe.

Some flights go wonderfully well. Some, less so. Problems can come from two areas: poor service, or old, less comfortable planes.

We’ve noticed there are a lot more old planes than we would have liked. As is often the case, an offhand comment from my wife sent me down a rabbit hole.

It turns out it is because the world cannot build new aircraft fast enough, so it is forced to keep the old ones flying.

Planes which were supposed to be retired years ago are still in the air because there is nothing to replace it, and this will be true for most of the next decade.

And old airplanes (not unlike old humans) need more maintenance. And the heart of the airplane, as Mr Raleigh reminds us, is its engine.

Engines are a unique business model. They are generally sold to airlines around, or even below, cost. The manufacturers essentially give the engines away. This makes sense, because engines should be thought of more as multi-decade subscriptions.

During the 30 years that an engine remains on the aircraft, it must visit a shop every few years for an overhaul, which costs millions of dollars in parts and labor.

In most cases, the manufacturer controls the parts and is the only party legally permitted to certify maintenance work or supply the components.

The airline is captive, and has no choice but to pay (or have a grounded airline).

It’s a pure Gillette razor and blade model, where you’re willing to not make money upfront so that you can then cash in for a very long time.

But unlike Gillette, there is a regulatory component which constrains these operations to a small subset of players which dominate the market. Engine maintenance is not discretionary as it is mandated by law, which enables part manufacturers to pass through any increases in costs which they might incur along the supply chain.

The longer an aircraft stays in service, the more it needs maintenance, and the more onerous that maintenance becomes.

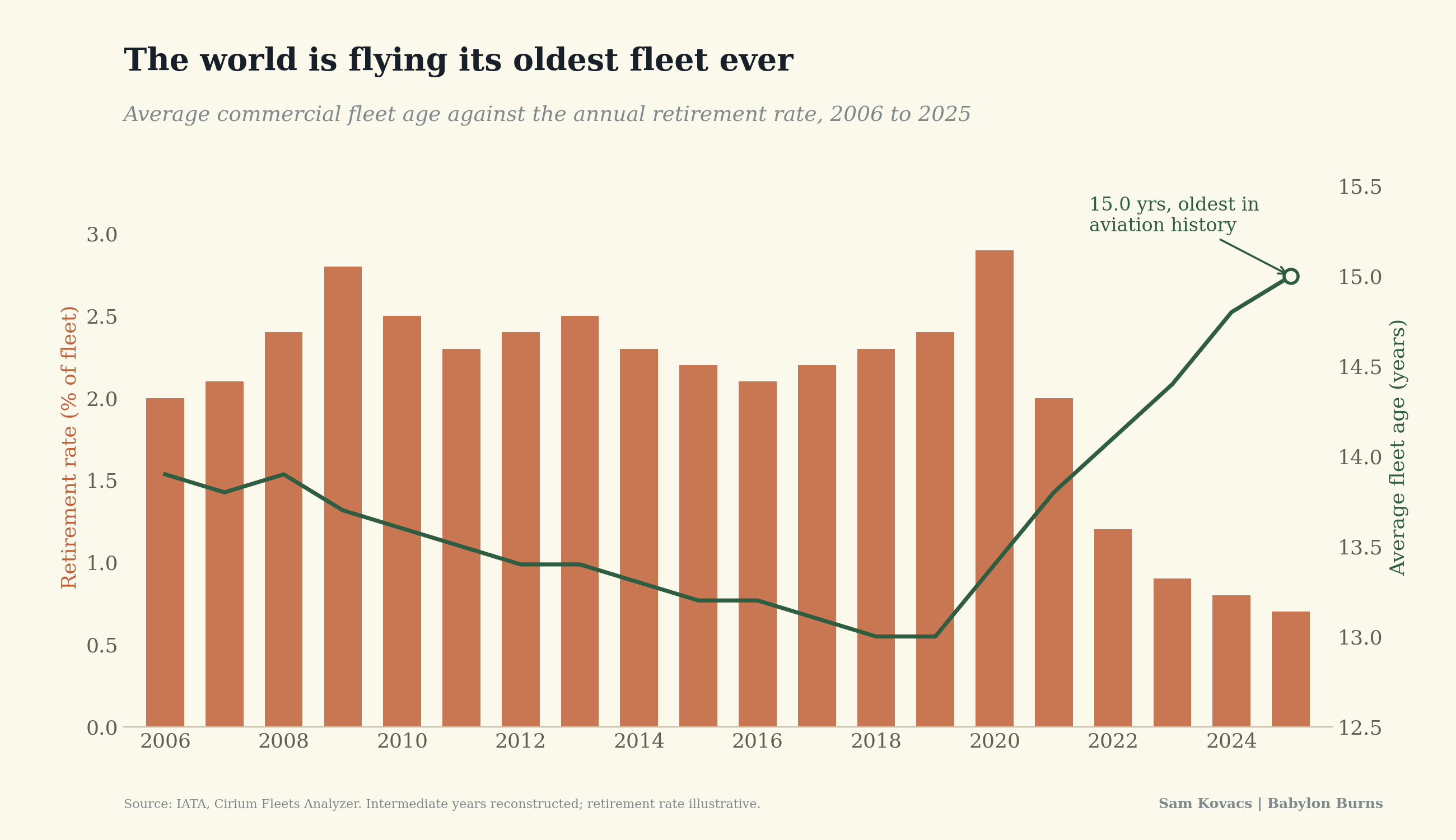

So the big question is simply: is the world’s fleet getting older and will it stay that way?

The answer to both of those questions is yes.

A shortage with no end in sight

The average commercial airplane today is about 15 years old, which is the oldest the global fleet has ever been. Before the pandemic, record deliveries brought the average age down during the 2010s. Since then deliveries collapsed, and with them the retirement rate of aircraft.

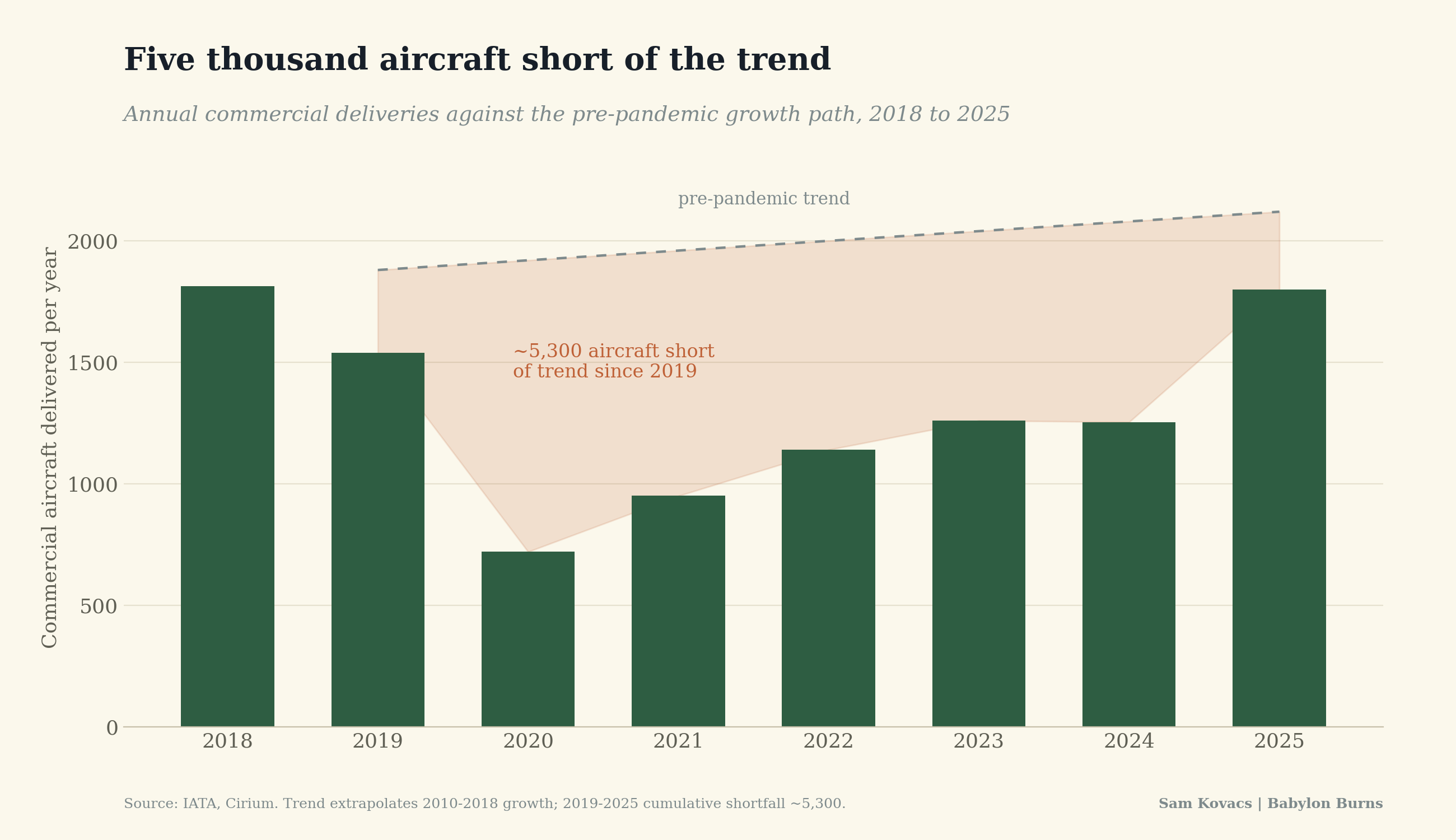

Global deliveries by Boeing and Airbus have undershot targets every single year since 2018, The two companies have been held back by their own supply chain constraints along with labor shortages (see scarcity causing the economic mismatch, here again).

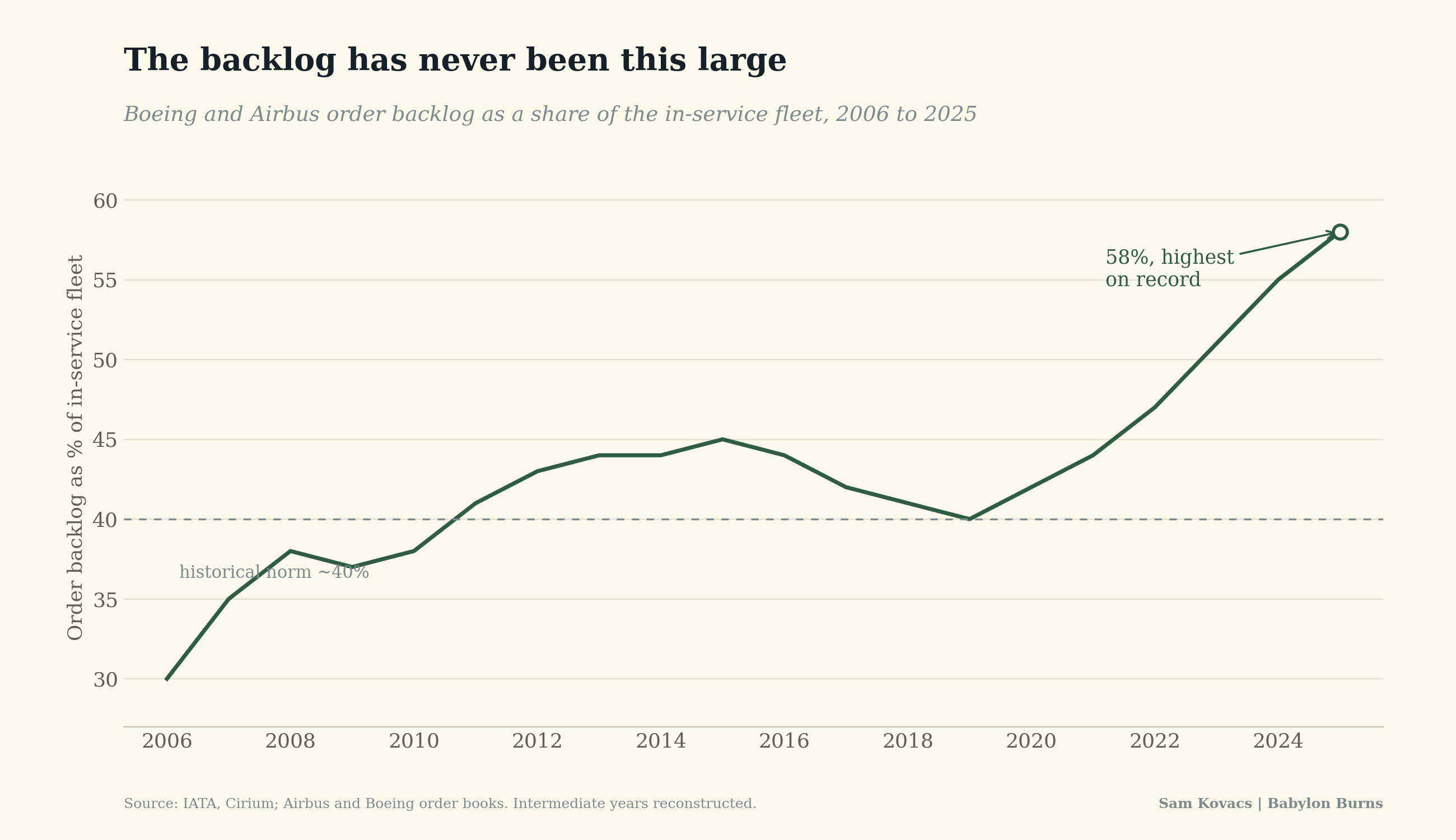

The backlog of orders is now above 17,000 aircraft, which is the largest in history and will take a decade to clear. While production hurdles have been easing, engines in particular remain in short supply and will be for the next decade.

The backlog represents 58% of the fleet currently flying, versus historical averages of around 40%, which is a clean way of visualising that planes that otherwise would have been retired are still flying.

With a record old-fleet, retirements at record lows, production that is struggling to recover and backlog that cannot clear for a decade, it is no surprise that aircraft are being flown more hours than ever in their history in order to cover the shortfall.

The conclusion is quite simple: the installed base that requires maintenance is large and locked. This will not resolve until sometime in the 2030s, in the most optimistic scenarios.

The money flows to engines

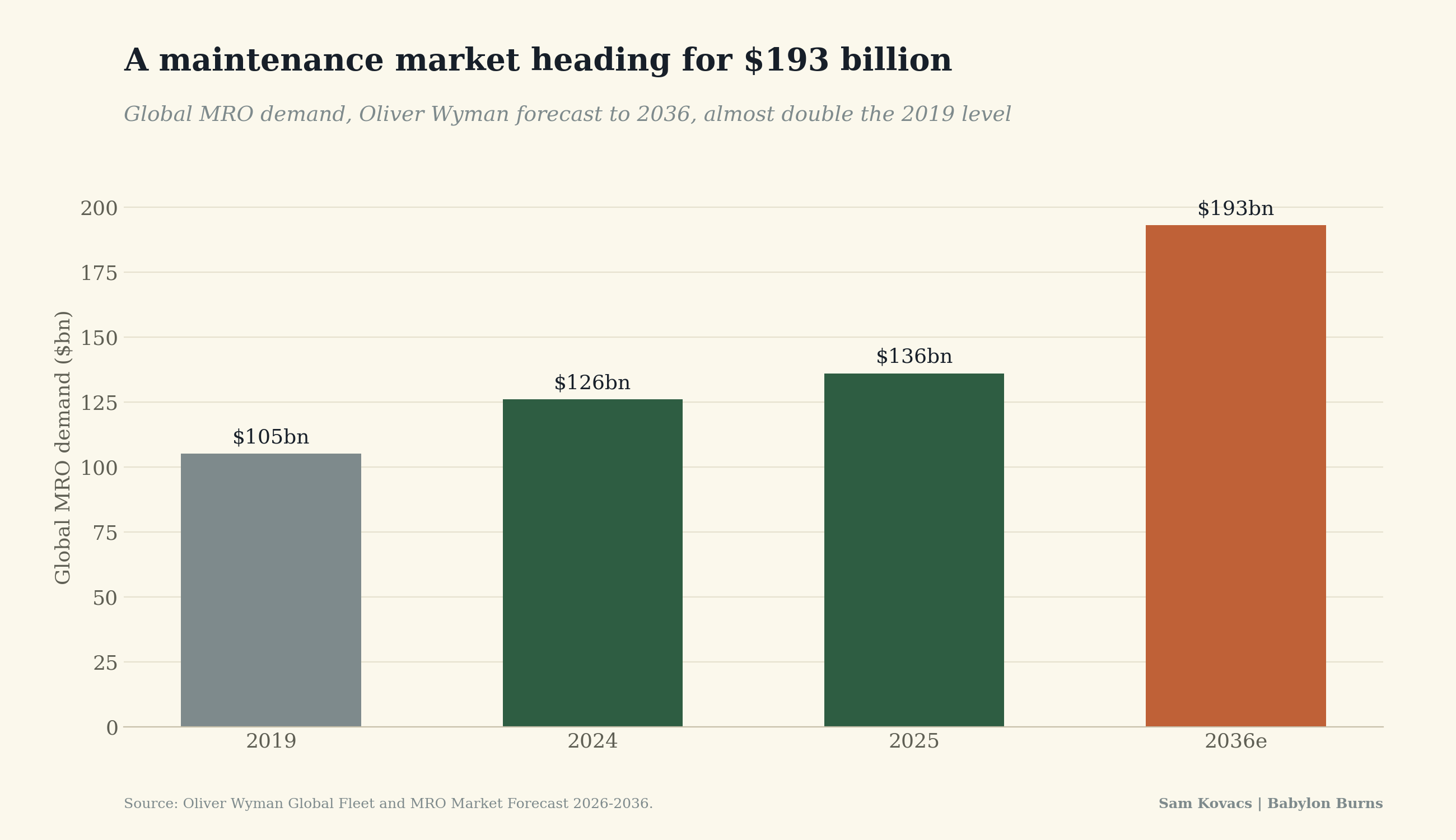

The maintenance, repair and overhaul (MRO) market was worth about $136bn in 2025, and expected to approach $193bn within 10 years, which would be double its level in 2019.

This growth is being driven primarily by aircraft age, causing more maintenance per aircraft, as the fleet itself is growing at the slow, supply constrained rate I highlighted above.

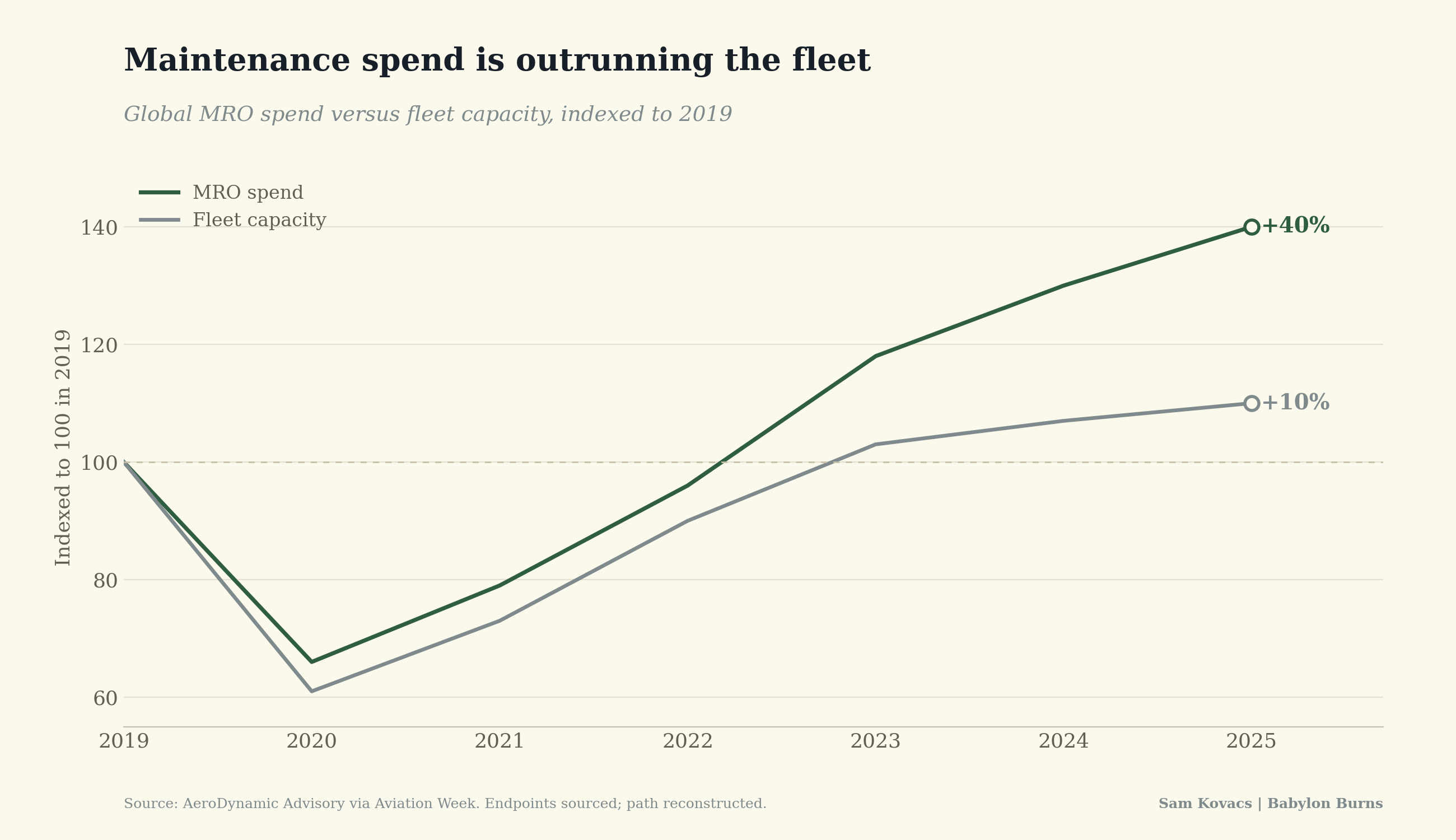

Since 2019, spending on maintenance has increased by 40% while the fleet size itself has only increased by 10%.

Every airplane is becoming more expensive to keep flying, which is the exact dynamic we would expect from an aging fleet.

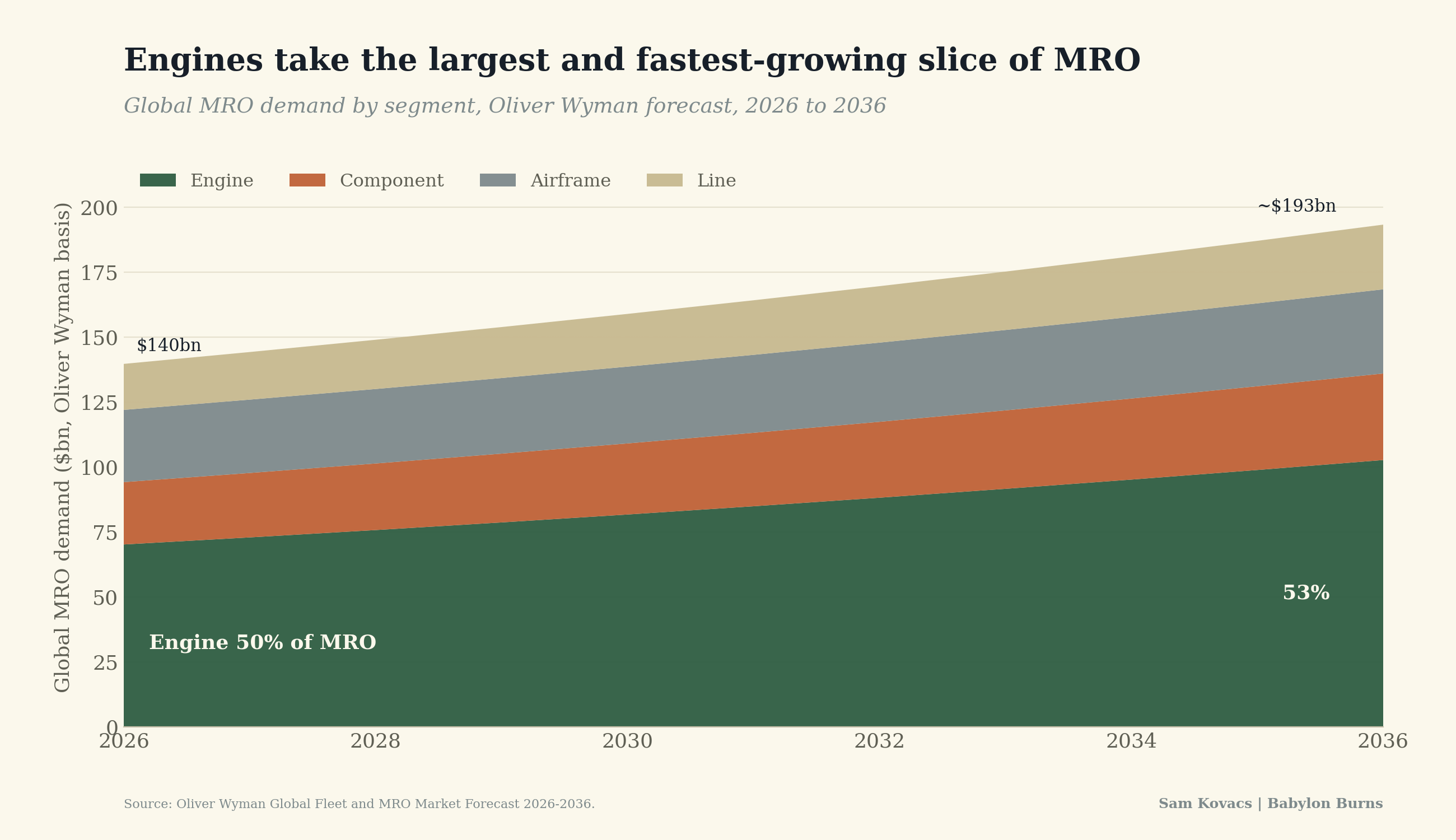

Within the MRO market, the money pools in one segment more than all others: engines.

Based on Oliver Wyman (a management consultancy)’s numbers, engine work is more than half of all maintenance spend, and is the fastest growing segment within the industry.

Of all repairs, engines are the most complex, the most tightly certified, the most mission critical, and as a consequence they are the most expensive part of an aircraft to maintain.

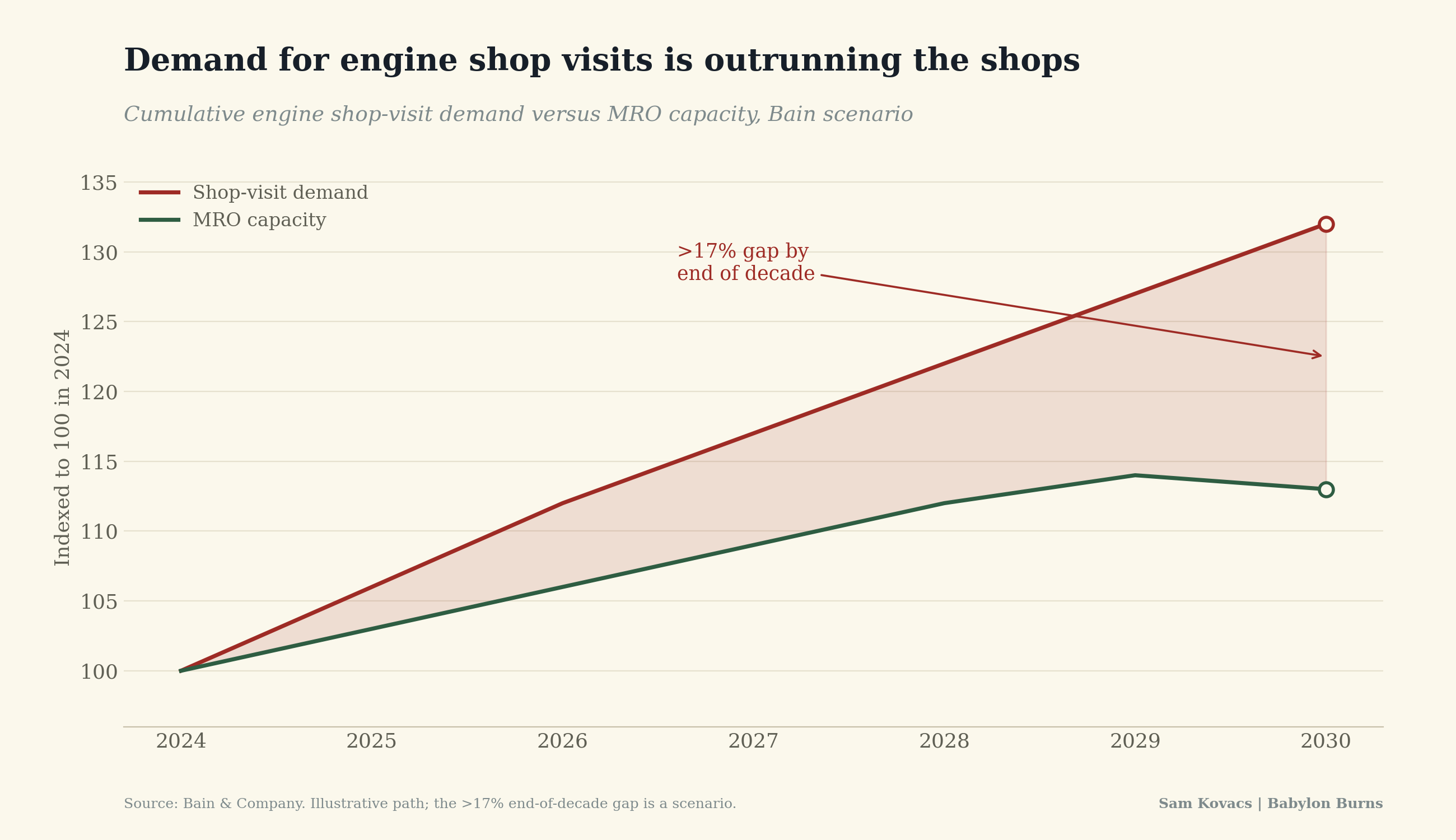

And here is the thing: the shops that are able to do this work are full, and there is simply not enough capacity to meet demand, and there won’t be for years. When supply and demand don’t meet, price moves to clear the market.

Bain & Co suggest that if maintenance capacity grows at its current pace, demand for engine shop visits will exceed supply by more than 17% by the end of the decade.

This is a market which cannot easily clear, because there is a massive regulatory barrier to surmount just for the right to participate.

You cannot maintain or repair parts for certified aircraft engines unless you hold the right certifications and approvals, or even the intellectual property that govern a specific engine.

So whilst the incumbents are struggling to ramp capacity fast enough to meet demand, there are massive regulatory hurdles to new entries.

This creates a long lasting setup for the industry, which will benefit investors who are able to enter these trades at the right time.

And I happen to have identified 3 stocks within the theme which make intuitive sense on the micro level, fit into the macro perfectly, and which have a chart which is looking constructive.

What’s more they are spread across 3 currencies (USD EUR GBP) providing some varied FX exposure. In all my writing, my baseline assumption will be that we are operating in US dollars. The vast majority of my income comes from the USD or currencies which are pegged to it, so it serves as my baseline. Everything will always be done to maximize USD value.

Trade 1: own the engine program

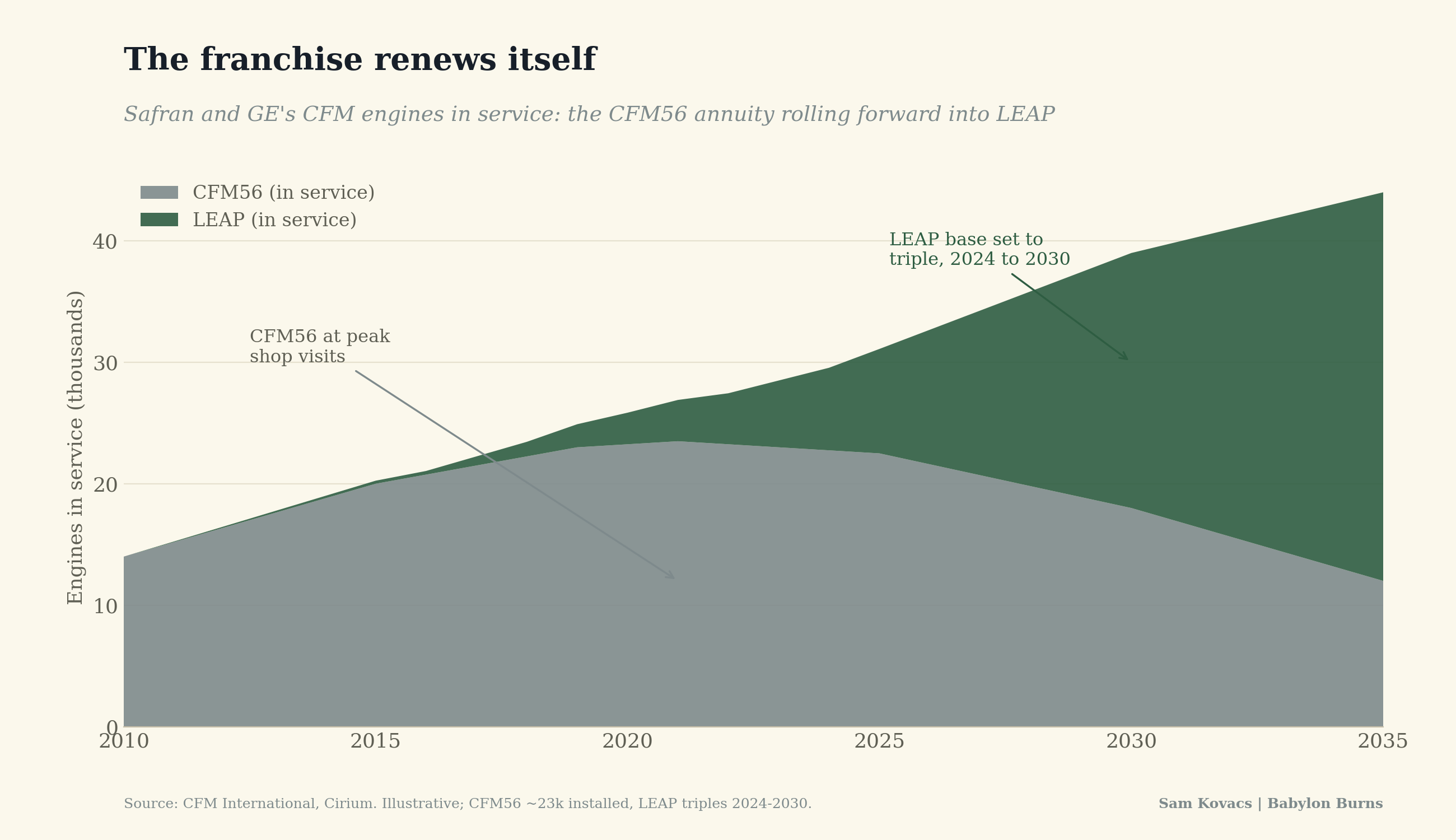

Safran (SAF) is a French aerospace company, listed in Paris, which through a 50-50 JV with General Electric , co-owns the most successful jet engine franchise in history: CFM.

CFM’s previous engine, the CFM56, has been built more than 33,000 times since 1982, making it the most produced jet engine ever. While production has ended, the installed base is going through some of the most lucrative years of its life with heavy, repeated shop visits before the engines are retired.

At the same time, their new engine, the LEAP, is replacing the CFM56 at a 1 for 1 rate on aircraft around the world. The LEAP installed base is set to roughly triple between now and the end of the decade.

That’s the beauty of it, they are the market leaders, and they are not losing market share as the hand-off from the previous engines to the new are happening. Spare parts and service revenue on LEAP engines only began flowing to the income statement in 2025.

Safran generated operating income of above €5 billion in 2025, and has guided towards above €7 billion by 2028. The civil aftermarket, the spare-parts business that is the heart of the thesis, grew at double-digit rates last year.

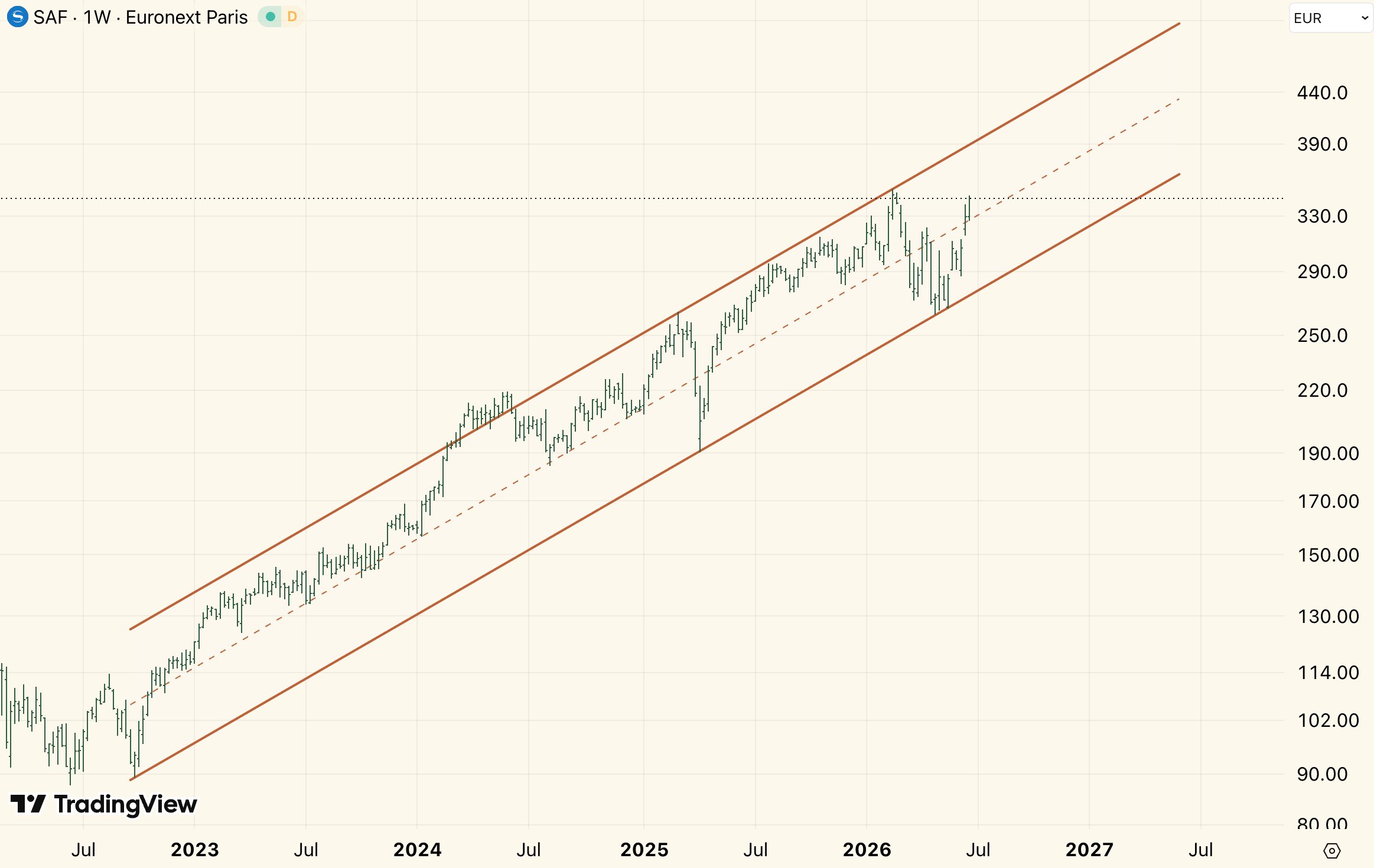

The shares currently trade at €343 which translates to enterprise value of around €142 billion, which is not cheap, giving you a free cashflow yield over 3%.

The market is clearly counting on the current narrative to play out, for the CFM56 base entering its peak overhaul years, the LEAP base tripling by 2030, LEAP spare-parts revenue that only began flowing to profit in 2025, and management’s own guidance lifting recurring operating income.

This is not priced with a steep margin of safety, but nor does it need to be. Your margin of safety comes from the near certainty in the contracted cashflows and its expanding pace.

The stock has been in a structural bull channel since July of 2023, and as it seeks to once again make new all time highs, the path is clear for it to reach €400-500 by next year.

The setup on the chart would be invalidated if it fell to the bottom of this channel, which gives us a stop loss around the €280 level which would need to be raised as months go by to follow up the channel.

Then there is the fact that the USD’s bull market versus the Euro which started in 2009 ended in 2022, and broke below the support last year in 2025.

The chart suggests that the strength in the US dollar is short lived unless it can reclaim 0.9 Euros in short order. If the dollar stays / turns weaker, then a position in Safran benefits naturally from this.

Trade 2: Own the small parts

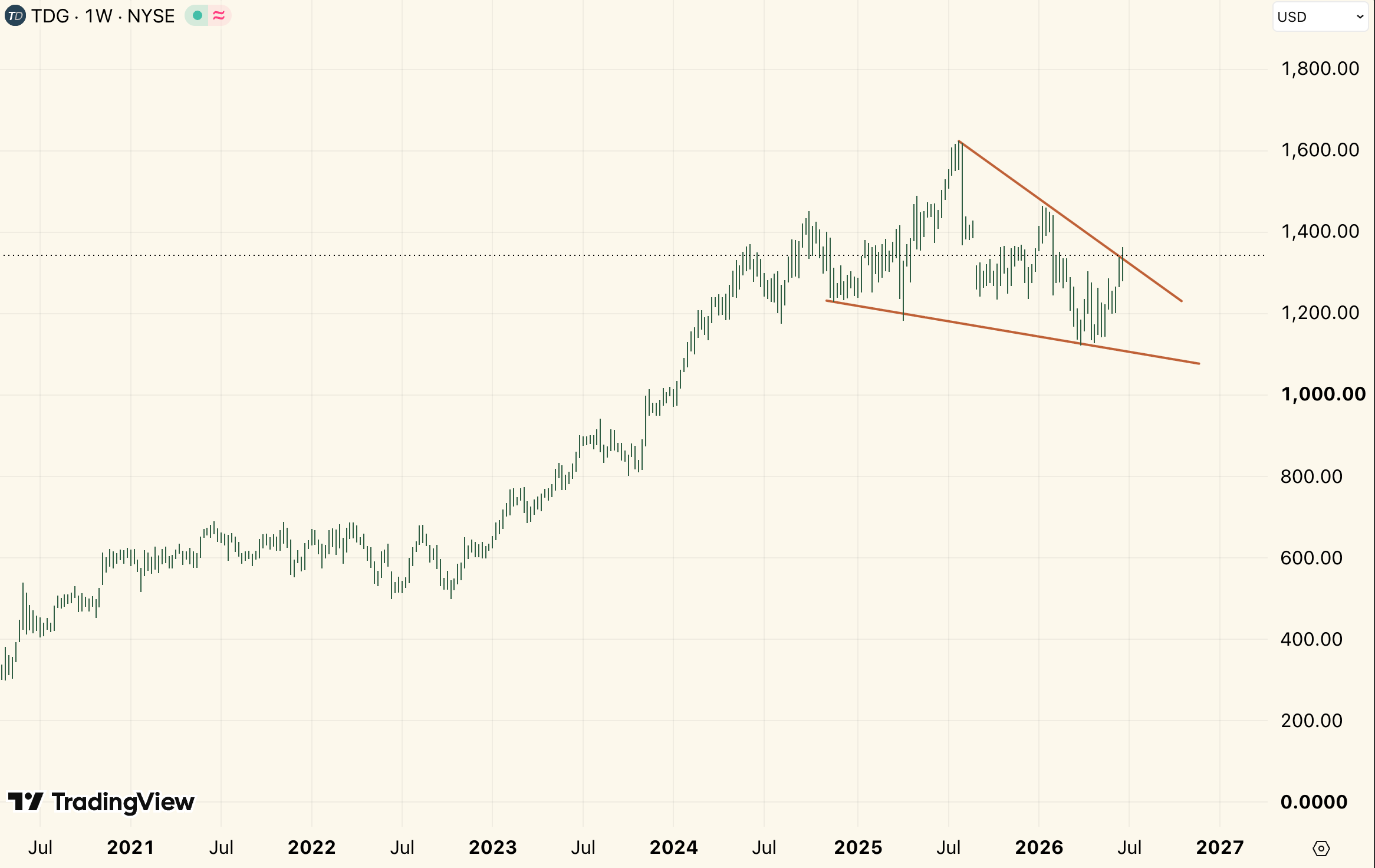

TransDigm ($TDG) is breaking out of its chart pattern as I type this, so lets lead with the chart. You’re looking at a stock which 8xed since the pandemic, topped at $1600 last year in 2025 and has been consolidating ever since in this falling wedge, of which it is attempting to break out of. A close above $1330 on Friday would validate the breakout, and a break above $1400 would get me more excited.

Here the failure mode is if the stock breaks below $1100, which is a similar 18% decline to the failure mode in Safran.

So that’s the chart, now, what does TransDigm do?

This is a company which has built itself around a ruthless insight: there are many small flight critical parts on an airplane which are proprietary and which have only one legal sources. 90% of Transdigm’s sales come from proprietary products which it designed and owns, and 75% are parts where it is the sole source, with no other company certified to issue them.

As is common in MRO, more than half of its revenue comes from the aftermarket, where it has a high margin replacement business.

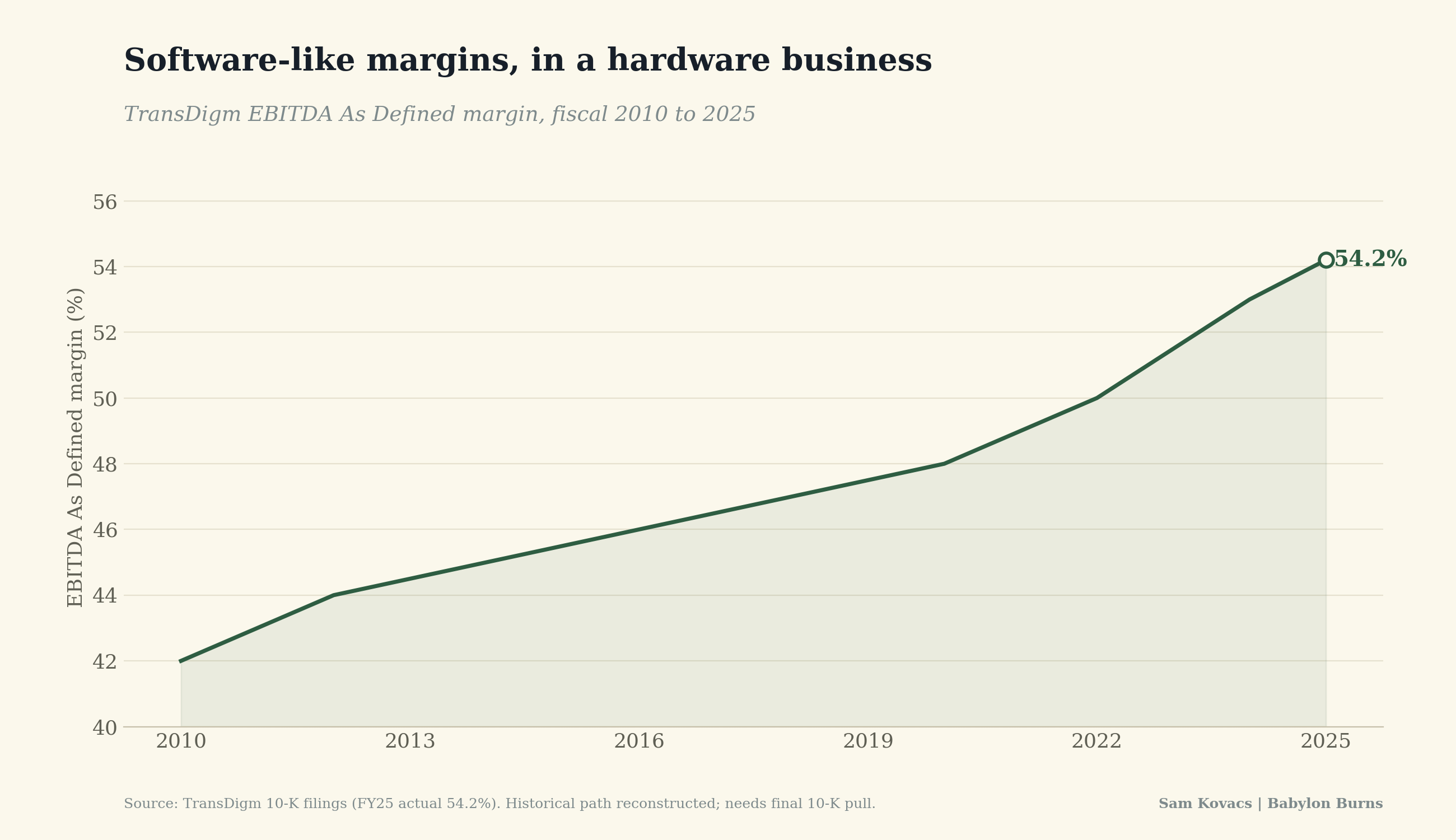

The consequence of this is that it has margins which do not resemble that of a manufacturing company whatsoever.

TransDigm earns operating margins before depreciation above fifty percent, a figure that has marched steadily higher for fifteen years as the company has acquired more sole-source positions and pushed pricing through them.

And think about that because it’s the living proof of the benefits of having a hold on a scarce good for which there is strong demand: you can take price and it doesn’t change volumes whatsoever.

Think about what sole-source means for its customers, the airlines. A grounded aircraft might be waiting on a single small valve that only one company is certified to make.

The part might cost a few thousand dollars. The aircraft costs tens of thousands of dollars a day sitting on the ground. The airline will pay almost any price for that part, almost immediately, every time.

Multiply that across tens of thousands of proprietary parts on an aging fleet that is flying more than ever, and the pricing power becomes self-evident.

TDG raised full-year guidance again in May, to earnings before depreciation of about $5.4 billion, up 14% year over year, with organic sales up 9%. This is not the cheapest entry. At 20x earnings and 5x levered, you are paying a full price for a wonderful machine.

You’re paying for quality, and I think that’s fair.

Trade 3: own the contract

The third pick is one of the strangest, but might also be one of the most interesting for the patient investor, as the market seems to have not been able to value it properly whatsoever.

Melrose is a British company, listed in London, which owns the UK’s aerospace champion, which was formerly known as GKN Aerospace.

Buried inside this company is a pile of contracts which very few people seem to understand, called risk-and-revenue-sharing partnerships, or RRSPs.

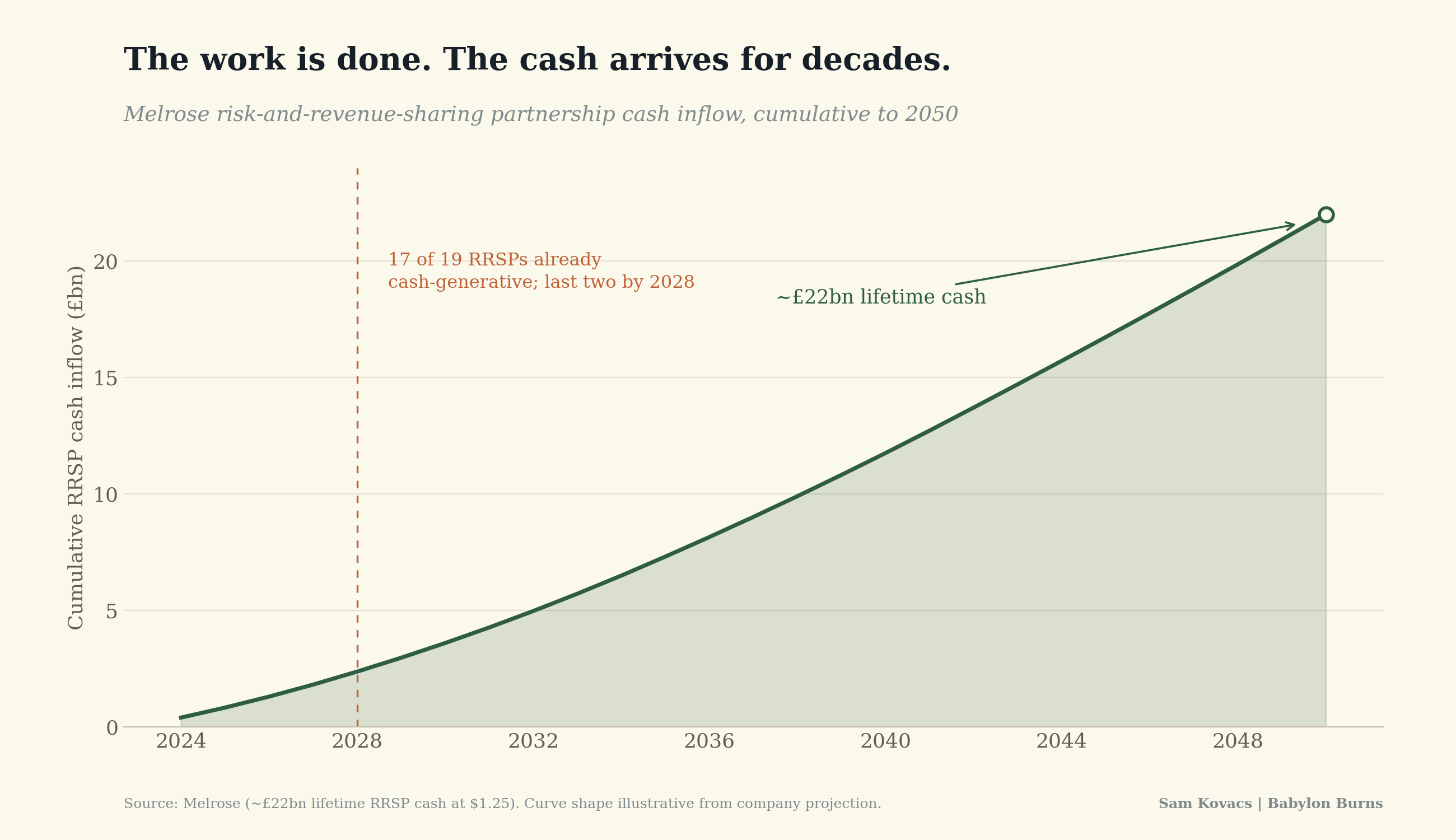

Decades ago, when engine makers wanted to develop new engines, they needed partners to share the large upfront costs. GKN would put up capital and engineering resources to help the engine maker, and in exchange it would receive contractual rights to a share of the programme’s revenue for the entire life of the programme.

These programmes run around 50 years, the cash invested in the partnerships was spent decades ago. Melrose holds 19 of these partnerships, which touch roughly 70% of the world’s flight hours in one way or another. Of these, 17 are already generating cash, with the last 2 turning cash flow positive by 2028.

The company expects to earn around £22 billion of cash from these contracts over their remaining lives between now and 2050.

This is a pure annuity. They don’t need to build engines, to staff a repair shop, or to manufacture any parts. They hold the rights, and the collect their slice of other programme’s for the next 25 years.

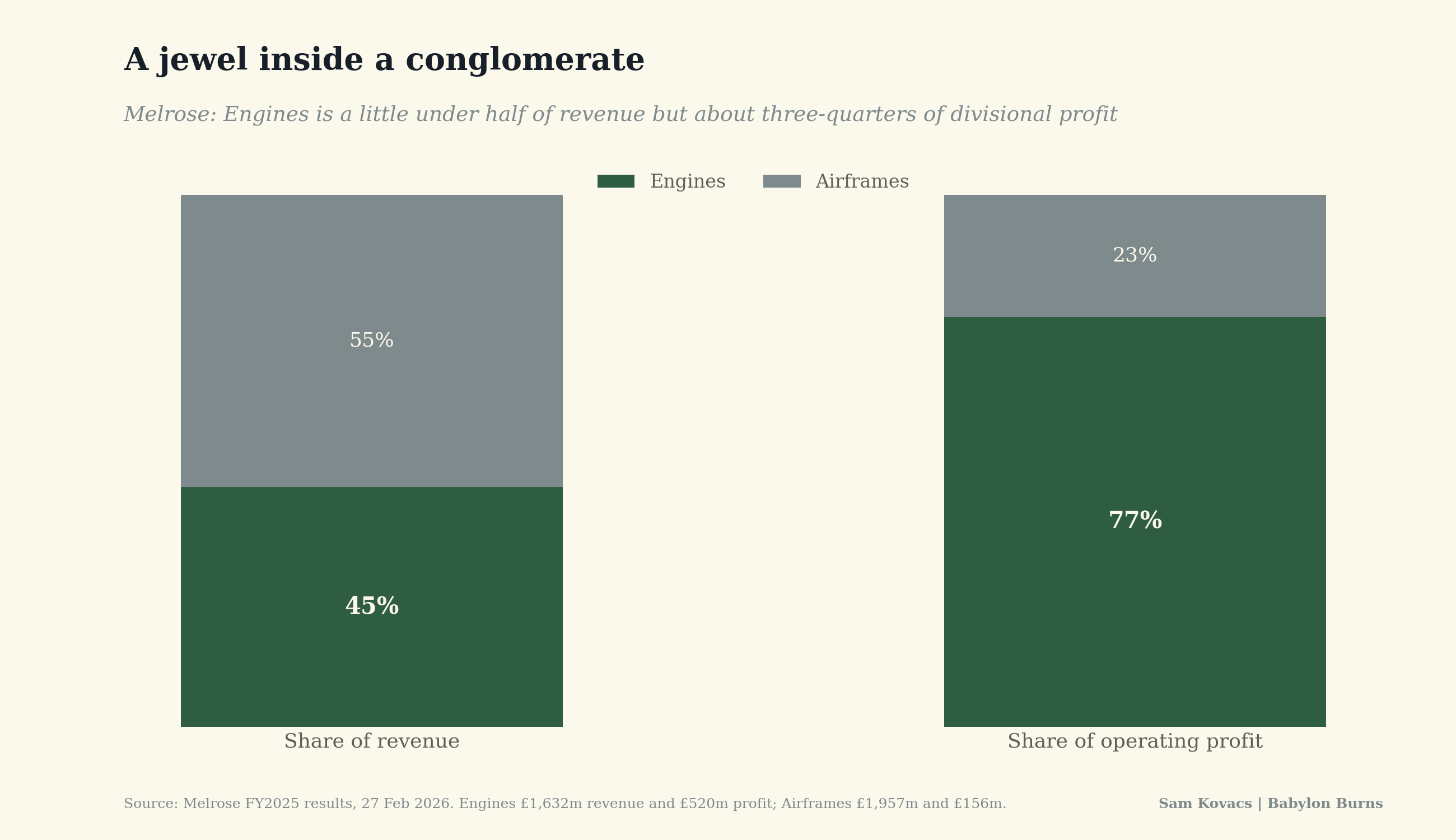

But the market isn’t properly valuing this, as these engine RRSPs are hidden inside a larger duller airframe components business which is more cyclical. The Engines business is a little under half of revenue and about three-quarters of the divisional operating profit.

At about 475 pence per share, Melrose is worth about £5.9 billion in equity, or around £7.3 billion once its £1.4 billion of net debt is added. This is about 11x operating profits, which is well below the two other picks.

Melrose’s whole enterprise value at 475p is about £7.3bn, and that buys three things: the RRSP annuity, the non-RRSP Engines business (OE, repair, government work), and Airframes. Let’s run some back of the napkin numbers.

If we put fair industrial values on the two non-annuity pieces: Airframes earns £156m of operating profit but is cyclical, so let’s call it 9x earnings , or about £1.4bn. Non-RRSP Engines is part of the £520m Engines profit, say £150-200m of it on a better multiple, about £2bn. That is roughly £3.4bn for the rest of the company, which leaves about £3.9bn of the £7.3bn enterprise value sitting on the annuity.

To value that £22bn stream at only £3.9bn, you have to discount it at about 18%. On a sensible breakdown, the market is applying roughly a 15-18% discount rate to a contractual, diversified, revenue-share stream on engines that fly 70% of the world’s hours.

Is that fair? Not, in my view. A fair rate for these cash flows is somewhere around 9-11%. At a 10% discount rate, the annuity alone is worth about £7bn, which is almost the entire current enterprise value by itself, meaning the market is handing you the rest of Melrose close to free.

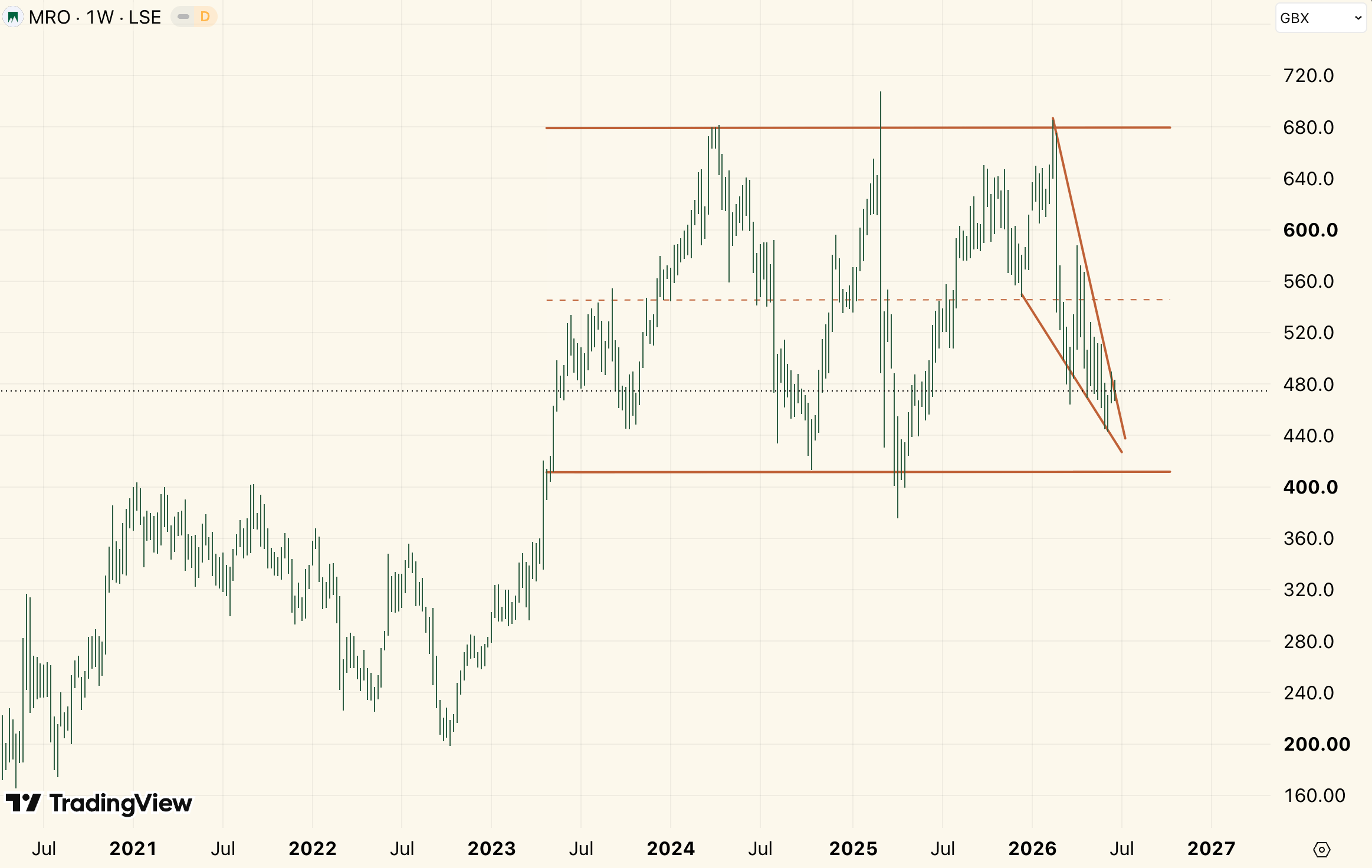

The stock has been range bound between 400 and 680 pence in a classic rectangle, and is now completing a downward wedge, with an attempt to break to the upside.

If it can close this week above 475, it is worth a starter position.

The failure mode here is at the bottom of the rectangle around 400, which is about 16% below the current price. Similarly the top of the range at 680 must be respected as a target, and also would correspond to the value should the annuity be valued at a 10% discount rate.

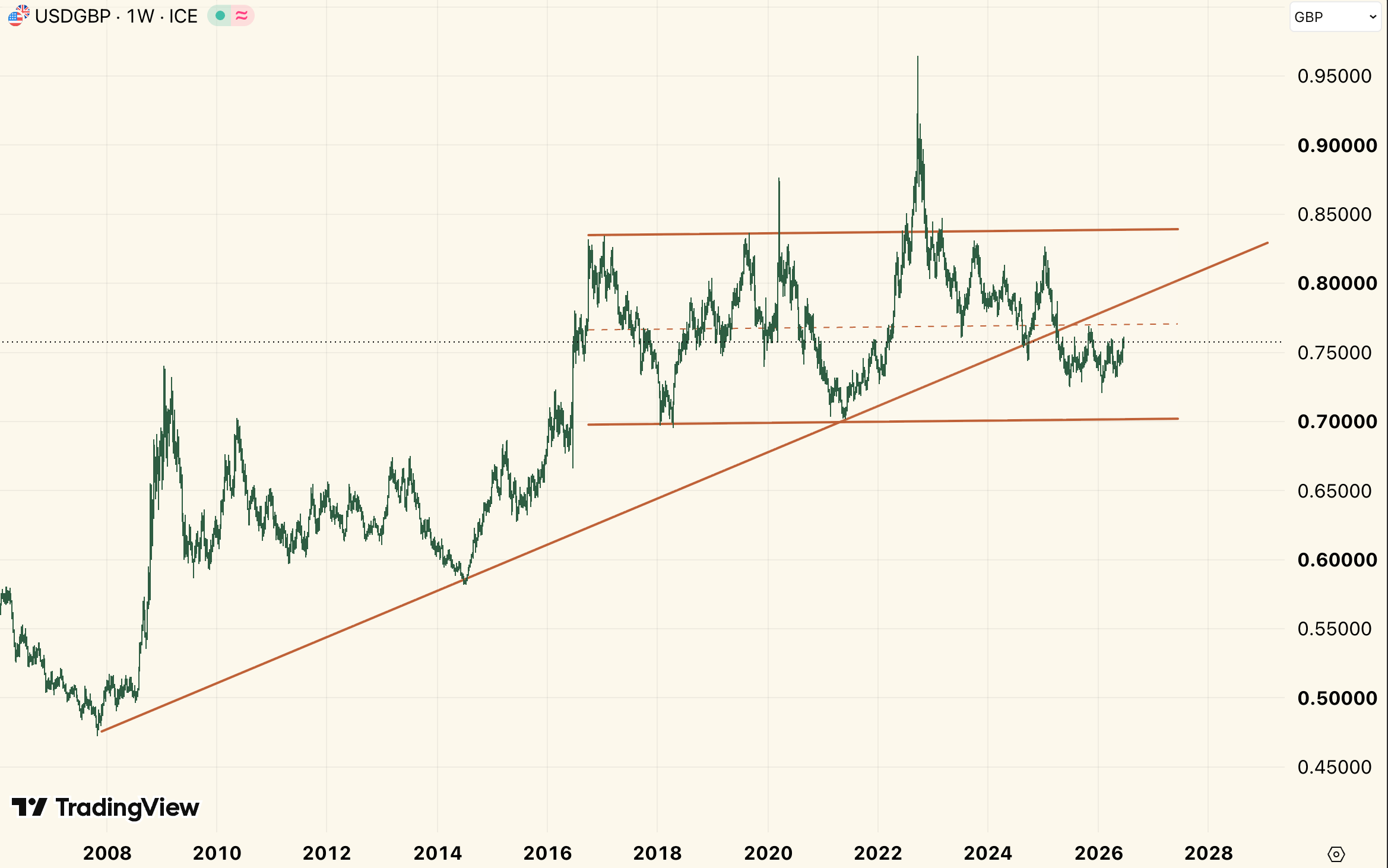

The USD has been range bound between 0.7 and 0.84 since 2017, but in April 2025 it broke below the support of the dollars 2009 to 2022’s bull market.

In my view this likely constrains the dollar into the lower half of the range, between 0.7 and 0.77 GBP in the interim. Here again, I am not afraid of owning a foreign stock (funny to call British foreign when I hold the passport) because the setup favours a weaker dollar, unless the dollar can convincingly reclaim 0.8, which I don’t think it will.

Conclusion and notes on position sizing and the use of TA.

I could have written an article on Micron (and I might). I chose for a second article to write instead on a theme which is less discussed, but nonetheless playing out as we speak.

I believe investors should deploy capital where there is the best risk-return, not where there is the most attention.

The setup in the MRO space looks interesting for these names I highlighted today.

But here’s the thing about investing, it’s not as much about the ideas as it is about the discipline.

In this industry, you’re great if you’re right 6 out of 10 times. You can be right 4 out of 10 times and still be great if you have the right discipline.

It’s easy to get married to a narrative, and narratives are dangerous, because they lure you in. Sometimes there is a 1,000 pound Gorilla ready to pounce on your thesis, and you just don’t see him.

Knowing that there are unknown unknowns which could screw us, we should turn to price as a source of truth, and as our ultimate keeper. Price action tells us the behaviour of all buyers and sellers of a security. If the chart develops into a bullish pattern which is supportive of our thesis, then this gives us a reason to enter the position.

If the chart goes against us and forms a bearish pattern, then that is when and where we exit the trade. This doesn’t mean the narrative or the thesis is wrong, but it might. And you’re much better off quitting at a price which stung you than a price which knocked you out.

If the trade is eventually good, then you can come back later when the chart is more constructive.

This becomes great to help sizing positions of bets across your portfolio. The 3 positions listed here have exit points that are between 16-19% below the current share price. That means that if we invest 10% of our portfolios across these names, then we’d lose 1.6% to 1.9% of our assets if the trade goes against us. That’s on the higher end of what I’d like, but gives us good information as to how a trade could expand if we add to it in the future.

In a portfolio, I’d probably initiate these at 2% each, with the option to add to the positions as the chart validates the breakouts and clears further levels.

What’s next

On 15 August 2026 I’ll launch the paid edition of Babylon Burns.The date is the fifty-fifth anniversary of Nixon closing the gold window in 1971, the act that set this whole chain in motion.

We’re still figuring out the exact pricing, but in the interim have set the pledges at low levels we will honor for anyone who decides to pledge now.

I will continue publishing weekly until then. Expect a mix of macro views and ideas sprinkled across.

Two asks before you go. If you want the next letter when it publishes, subscribe, the free work alone will be worth your inbox.

And if this one was useful, repost it wherever you found it, or send it to one person who you think will like it.

As Babylon burns, we’ll light the cigars.

Sam Kovacs

Babylon Burns is written for informational purposes and not to be construed as investment advice. I write about what I own and how I think. Your decisions are your own; do your own work before acting on anything here.

The scarcity framework is the real contribution here, more than any individual trade. "When there is an enforced control point which prevents supply from expanding to meet demand, there is scarcity." That one sentence is a better investing education than most books. The engine aftermarket stacks three layers of scarcity on top of each other: the fleet is aging faster than production can replace it, the backlog won't clear until the 2030s, and certification requirements block new entrants from competing for the work. All three have to break simultaneously for the thesis to fail.

What makes this structurally different from the AI trade everyone is watching is that none of it depends on a narrative holding. The aging fleet is physics. The production bottleneck is industrial capacity. The certification barrier is regulation. A chatbot isn't going to overhaul a turbine engine. The scarcity here is the kind that technology can't dissolve, which is the opposite of the kind of scarcity most of the market is paying 94x sales for right now.

Hey Sam, good find here. I have a few quick questions:

1. This is a cyclical trade (reminds me of a 'Capital Returns' strategy), but I'm curious why you see this as a trade and not a multi-year investment? Perhaps the stocks are not 'value' as in very cheap, but it feels based on your analysis they could be good mid term holds.

2. As you are trading, is this a spot or leveraged trade?

Thanks!