They sold you a dream and you bought it wholesale...

As Babylon burns, we'll light the cigars.

“Study, get a job, work hard, save for a house, max your retirement account, and everything will be ok.”

But the world on which the 20th century’s financial system was built is fundamentally fractured.

I don’t mean to say this in a “sky is always falling” kind of way. It’s simply that there are certain things, namely monetary stability and geopolitical order, which will never be the same.

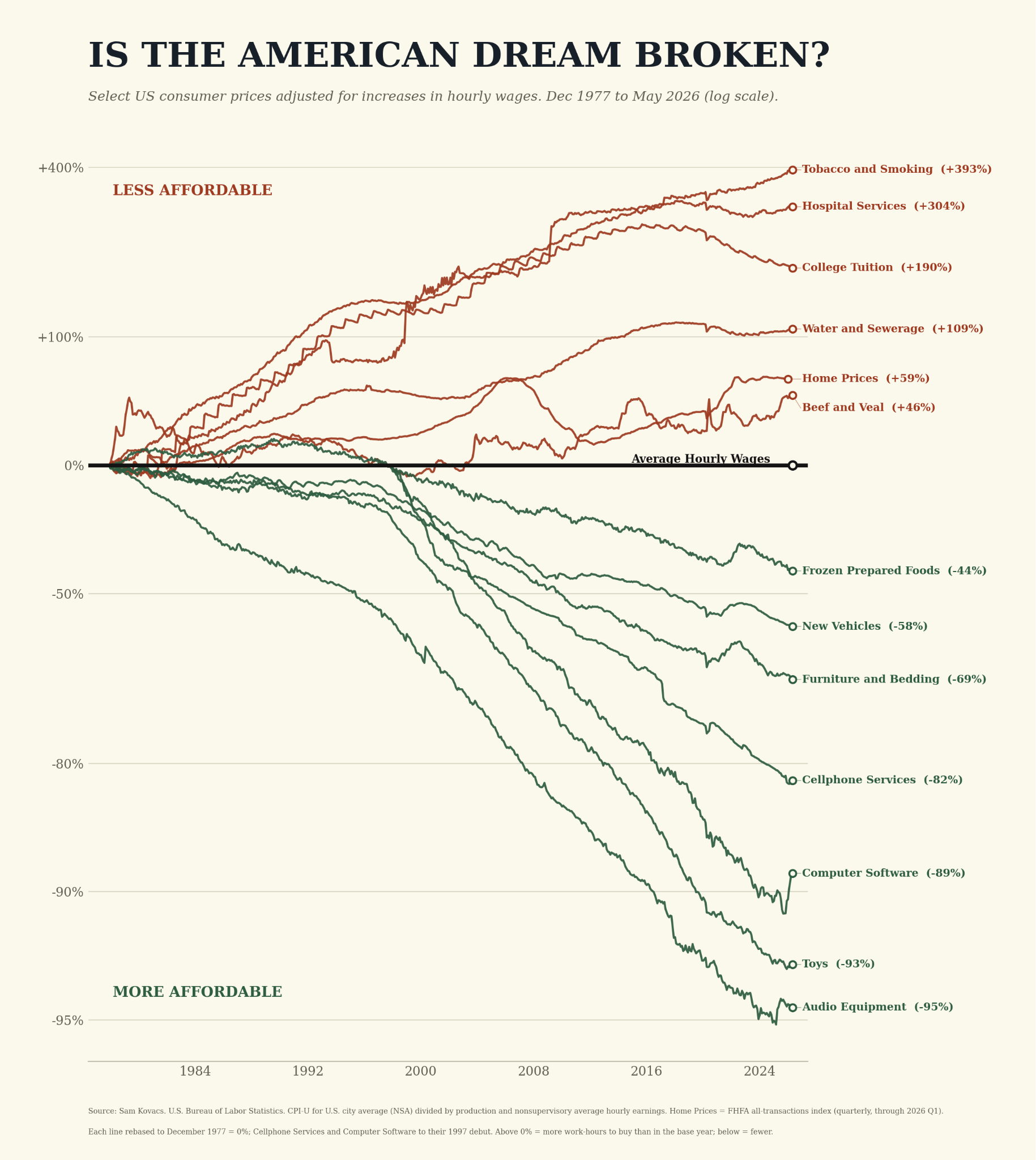

During the past 50 years, the cost of the things which are the hallmarks of middle class American life have gotten out of control, while the nice to haves have deflated, keeping the perception of tame inflation.

And what’s more, the US government is actively working against its own currency.

In February 2022, the United States and its allies did something never before tried against a nuclear power: they switched off its money. Hundreds of billions in Russian central bank reserves, dollars and euros, sitting in the system, earned and saved like anyone else’s, frozen by decree.

Every central banker outside the Western alliance watched it happen and drew the same conclusion at the same moment: that could be us. The realization that the world’s reserve currency came with strings attached hit hard.

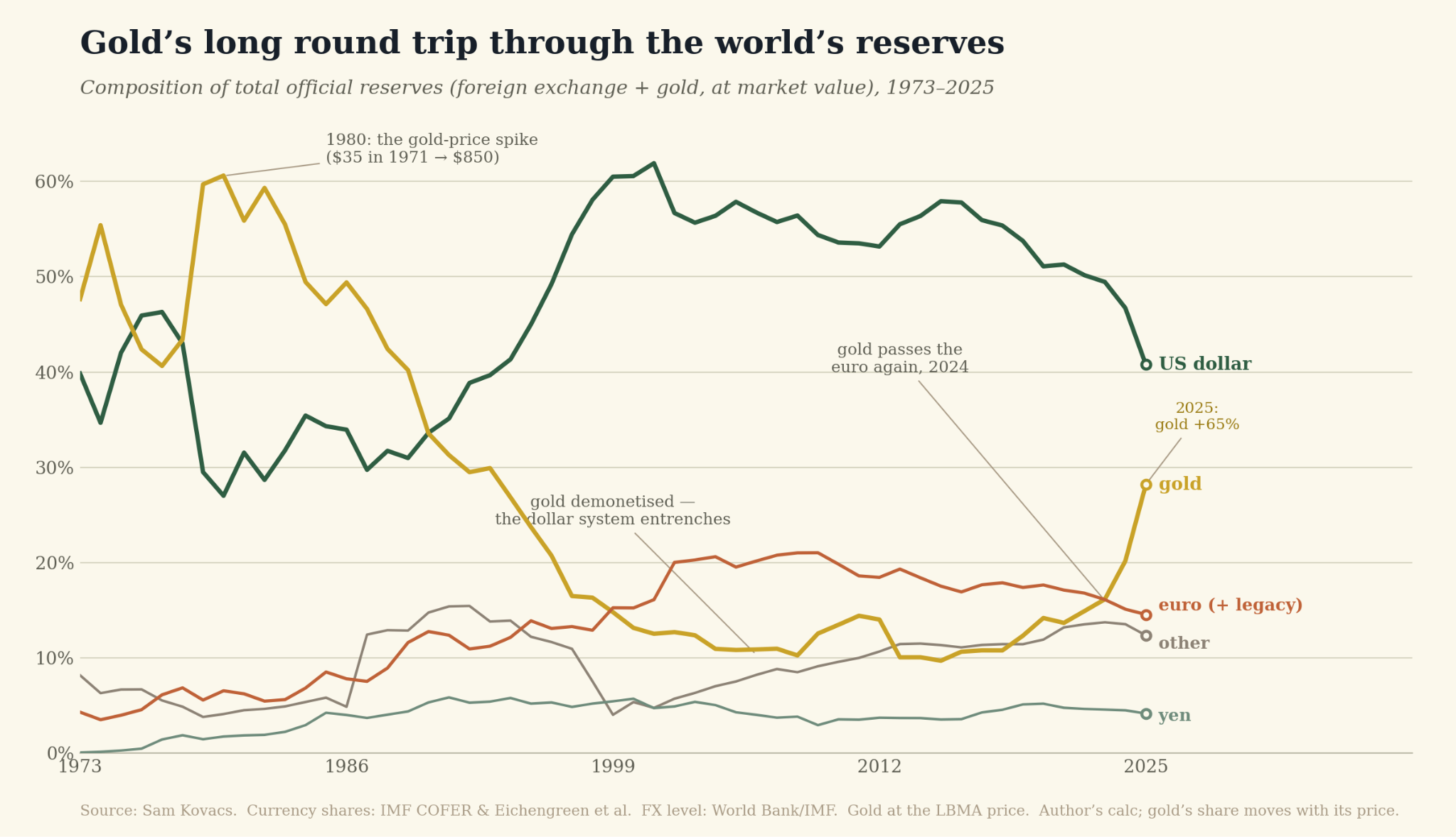

They’ve been acting on it ever since. Central banks have bought gold at double the historical pace for four years running. Foreign central banks now hold more gold than US Treasuries, for the first time since 1996.

Meanwhile, the issuer of the currency they’re walking away from is running a deficit of nearly 6% of GDP, in peacetime, at full employment, with one tax dollar in five going to interest alone.

The United States now pays more to its creditors than for its military.

As you probably know, US debt held by the public is on track to eclipse the WWII record.

The people who manage the world’s money are backing away from the dollar at the same time that America has no choice but to debase it.

Those two themes should dictate investment mandates for the next twenty years.

I’ll be referring to these two themes as debasement and multipolar fracture: the deliberate erosion of money, and the breaking apart of the world order that money was built on.

Everything I will ever publish here is downstream of those two.

Why I’m starting this Letter

I’ve published equity research publicly for eleven years, run a systematic macro hedge fund, and have advised sovereigns on capital and policy.

On 21 February 2026 I sent the report below to a short list of associates and hedge fund clients, which concluded:

The market is not adequately pricing the risk of US military action against Iran. Oil at $66-72 with two carrier groups converging on the region and a presidential ultimatum ticking down represents a significant underpricing of tail risk. The asymmetry favors long energy / defense / shipping.

I left Dubai for Cape Town that week, and avoided the subsequent strife in the Middle East.

I had been going back and forth for the past few years on the idea of starting a global macro newsletter which would synthesize the insights of my living in a dozen countries, advising global south Sovereigns on policy, and my unrelenting obsession with financial markets.

Up until today, I continually deferred.” I’m busy with the fund” ,” I don’t have the time”, “I’m content with my current businesses”, “I’m travelling too much”, “I’m learning how to surf, leave me alone”.

But finally, my good friend George Noble, a former colleague of Peter Lynch’s at Fidelity, convinced me that this would be both valuable to the investment community and for myself.

So this is the first edition, which will set the tone for what’s yet to come.

My frameworks are a mosaic of all the people I’ve read who shaped my thinking, and I’ll name them as we go. Expect the classic sitting on shoulders of giants BS lip service here and there.

Many of these people, unfortunately, are either academics with frameworks but no actionable insights, or they are married to a single asset class.

What I will offer instead, is the distillation of my macro frameworks into an actual active global portfolio, with trades which are shared, sized and time bound.

And one commitment up front: everything recommended in my letters is mirrored with my own capital. I eat my own cooking.

[ SUBSCRIBE BUTTON ]

Debasement

The world you grew up in, one dominant power (the US), one reserve currency (the US dollar), capital going wherever it earned most (mostly US equity) ran so smoothly that we stopped questioning what kept it ticking along.

What kept it ticking along is growth.

Without growth, the capitalist engine would fall apart. And this beautiful engine of ours, really only has three different sources of fuel:: demographics, productivity, and debt.

This is economics 101, derived from Solow’s growth model, and the framework has been modernized and simplified by Raoul Pal at GMI, to whom I owe a debt of gratitude for the elegance of his model.

The West rode population growth and demographics growth for two centuries, and when they sputtered, it had no choice but to choose debt as the growth source of last resort.

But today, even the debt engine is extended, yields less returns than in the past, and is starting to make the whole system lethargic.

Let me explain briefly why every one of these levers has been seized.

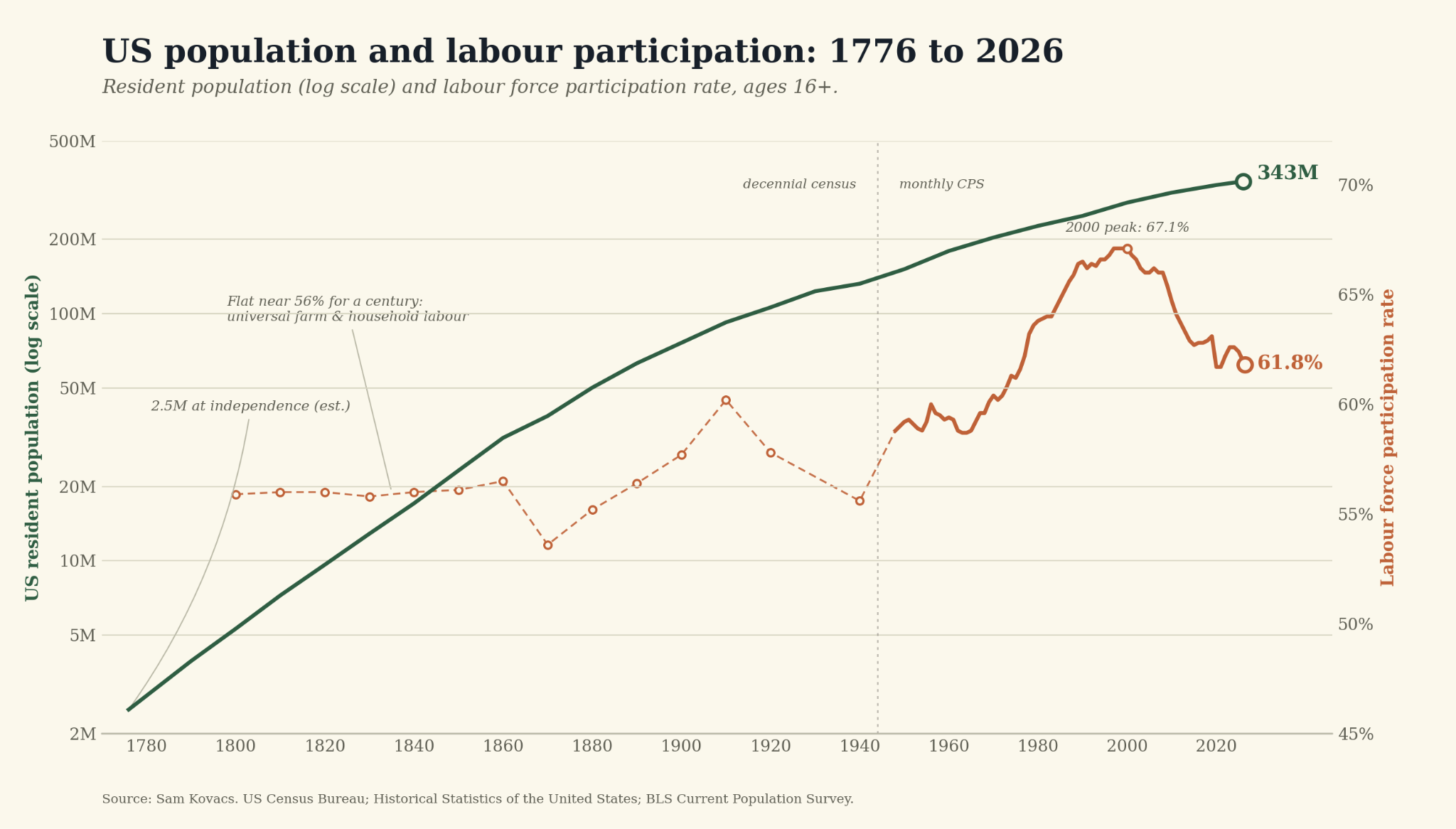

Let’s start with demographics. A growing economy needs a growing workforce, and for most of history that was automatic: the United States went from 2.5 million people at independence to over 280 million by 2000, with the share of adults in work climbing from 50% to 67% over the same period..

Then, both growth and participation changed course. Birth rates across the developed world have sat below replacement since the 1970s, so populations are set to shrink, and participation has fallen back toward 62%. In the US in the 1960s, five workers supported every retiree. Today it’s fewer than three. By 2050 it will be two. Japan’s population peaked in 2008, China’s in 2022. Others are following.

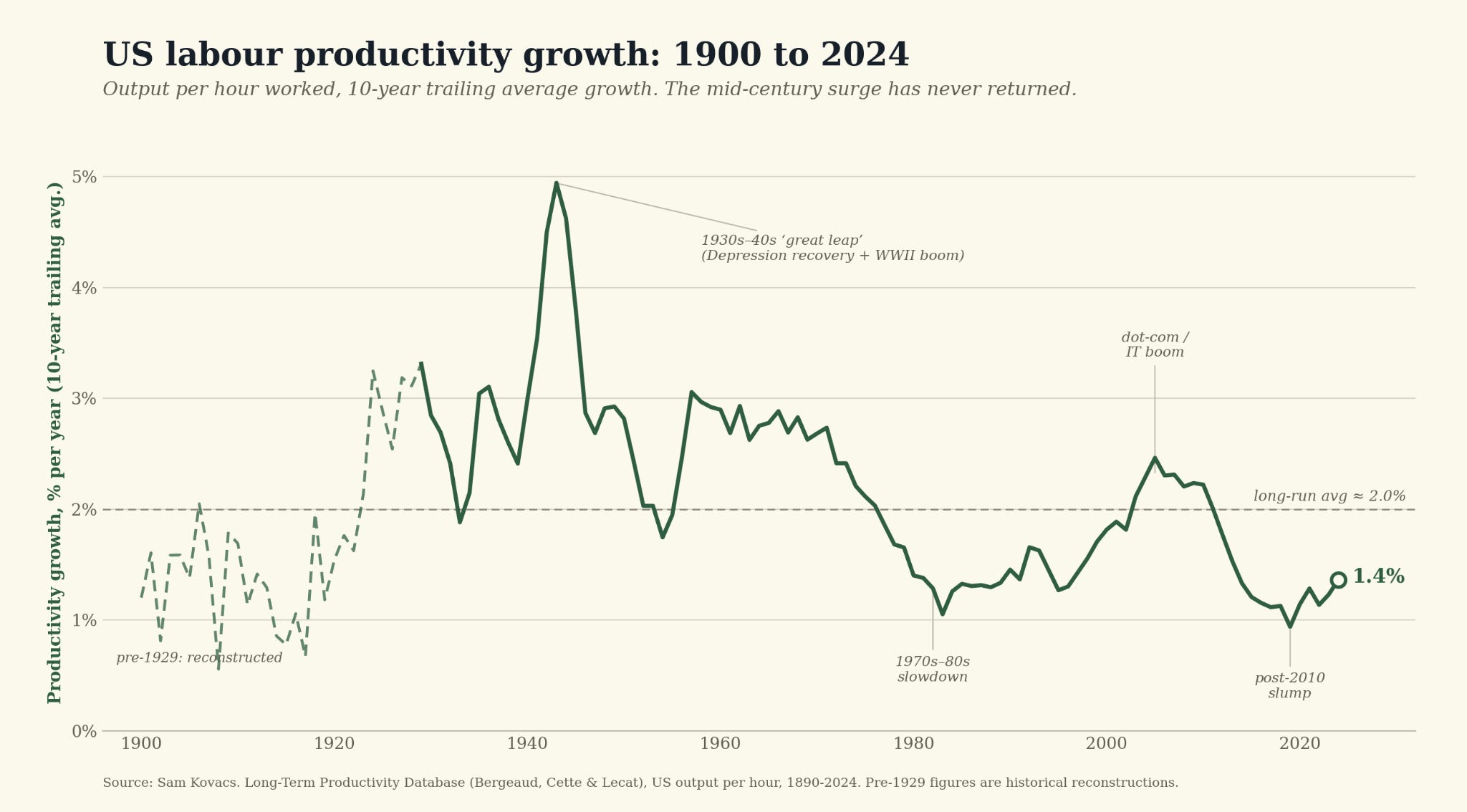

Productivity is the second fuel, and it’s been sputtering for fifty years. Between 1870 and 1970, output per worker grew about 2.8% a year, doubling every twenty-five years: a man’s son produced twice what he did.

Then it slowed, even as the technology got more impressive. We built the computer, the internet, the smartphone, and now AI, yet measured productivity growth fell to around 1.5%. Solow’s old line still holds: “you can see the computer age everywhere except in the productivity statistics”. Maybe AI will finally change this. I hope it does. For now, it’s not there in the data, and some research is suggesting that within organizations AI has failed to increase output. My gut is that this is because they are trying to plug AI into archaic workflows rather than rebuild the workflows natively around AI. We might be witnessing something of a productivity paradox whereby productivity declines or stalls at first as we go through a period of upskilling, retooling, and reorganization. Either way, the verdict is that productivity isn’t and hasn’t been what it was between 1870 and 1970.

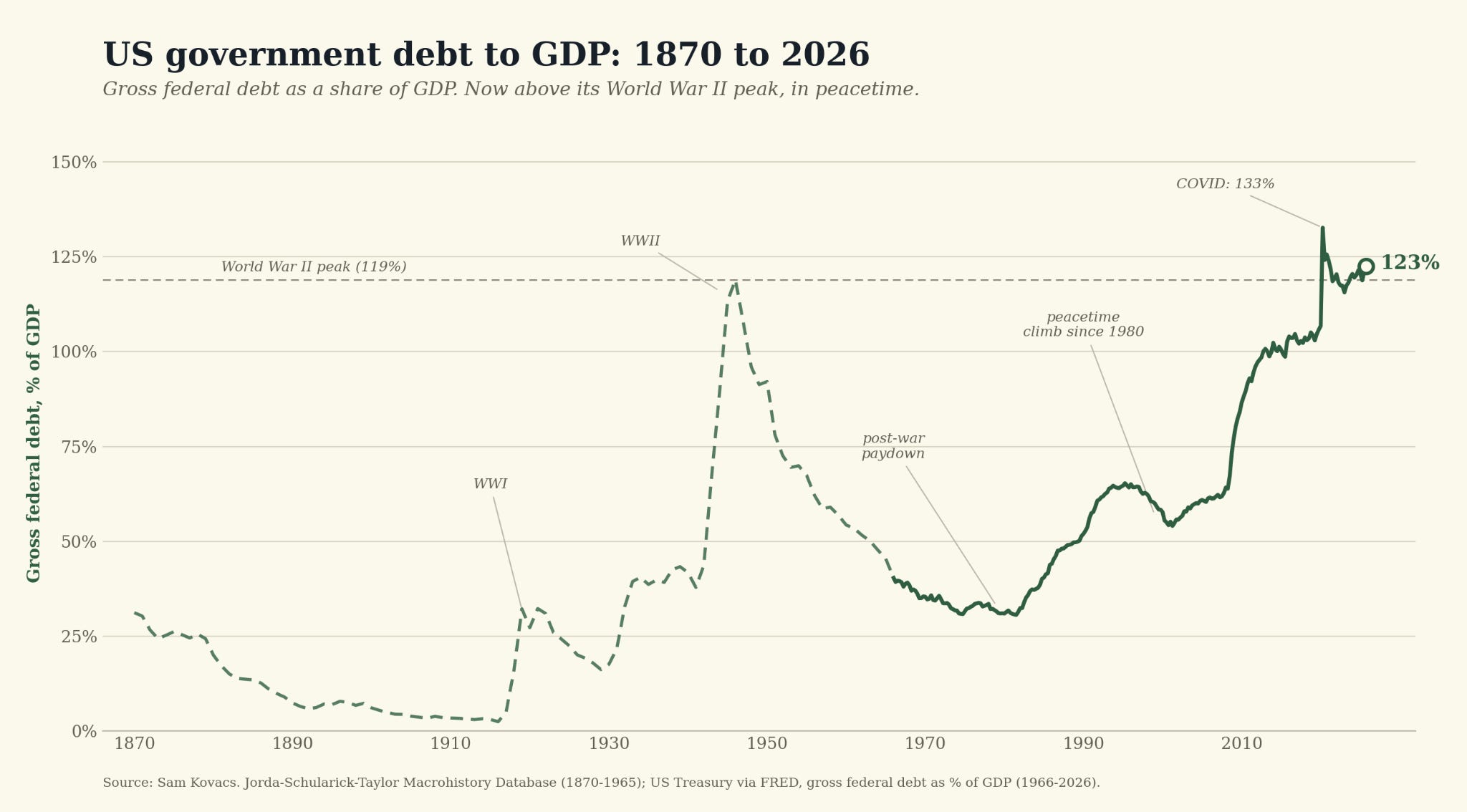

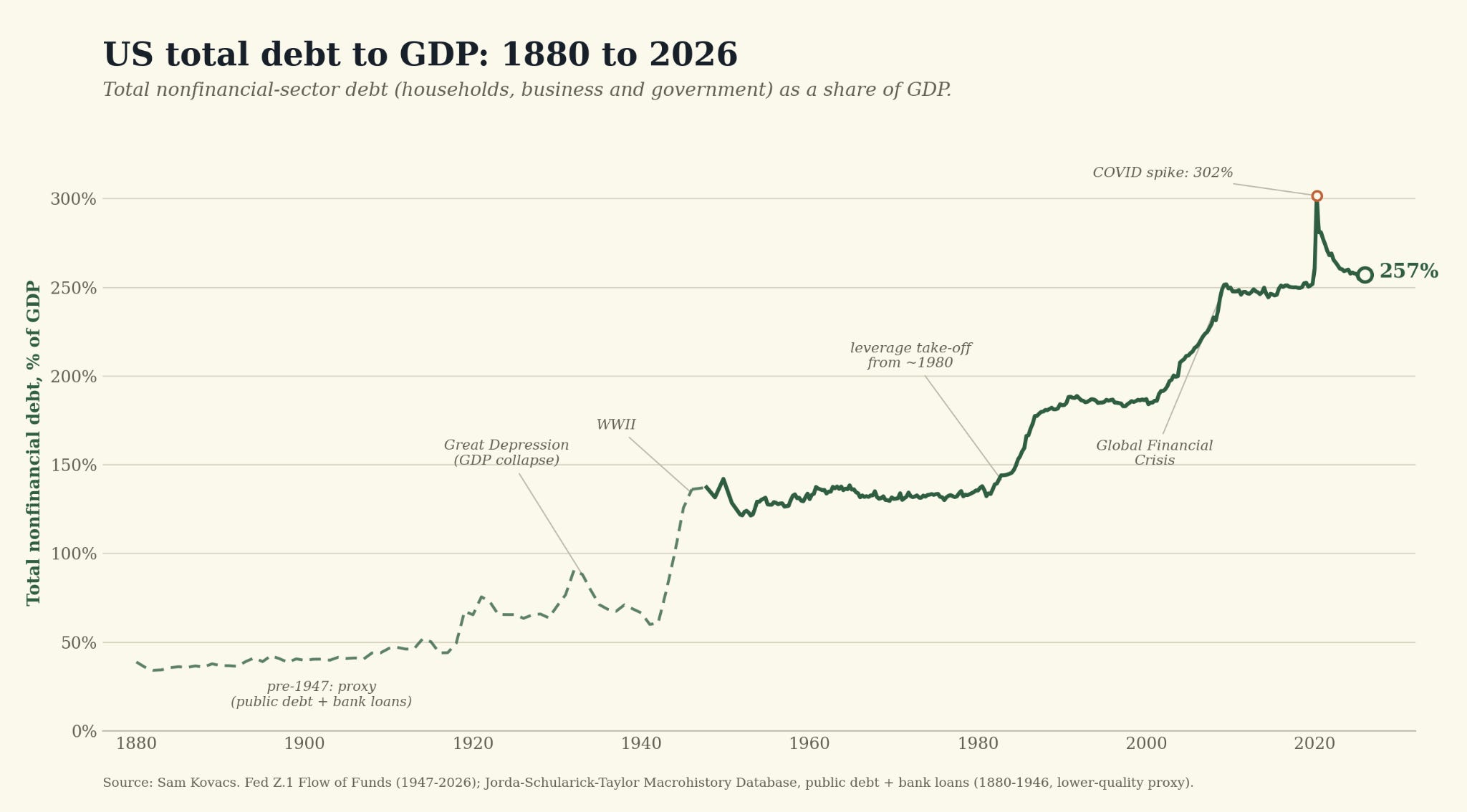

So governments, households, and businesses pulled the third lever: debt. Debt is future growth, spent now. When it builds something that earns more than it costs, it works. When it papers over the failure of the other two sources of growth, or is allocated to government expenses with no credible sources of return, then we eventually run into trouble. US federal debt has gone from 37% of the economy in 1970 to over 120% today.

The last federal surplus was in 2001, the year Gladiator won Best Picture. It’s only getting worse, as there are no other sources of growth. When you add household and business debt, it’s looking even worse.

When debt gets this big you eventually run into trouble and have to work your way out.

There are exactly four ways out, at least according to Ray Dalio of Bridgewater, who is the man behind the second framework we need to lean on: austerity, default, debasement, or a mix of all three.

You can try austerity: cut spending and raise taxes until the debt falls. At the scale required, that means cutting pensions, healthcare, and benefits that tens of millions of voters depend on. No government that tries it survives the next election, and every politician knows it. Half the constituency won’t take a tax increase, the other half won’t take a benefit decrease. It’s a political non-starter.

You can default: simply refuse to pay. For the issuer of the world’s reserve currency, that isn’t a viable solution. The Treasury bond is the foundation under global trade, banking, and pensions. Choosing to default would be catapulting the US away from the global reserve currency and seriously undermine its position in the global world order. It isn’t happening because unlike Lehman Brothers, Uncle Sam has an ace up his sleeve: Debasement.

The logic is simple. Debt is $39 trillion, and counting. But if a dollar could be worth less than it is now, then the government can repay its debt in the future with funny money that’s not worth what it was when they lent it.

The numbers on your statement still go up while each dollar buys less, and the pain is spread so thin, over so many years, that no one can name the day they were robbed. That’s why it gets chosen again and again by countries in this situation.

It was chosen after the Great Financial Crisis in 2009. It was chosen again in 2020. The US isn’t the first to try this. Rome, Weimar Germany, the Soviet Union before its collapse.

Or you can attempt what Ray Dalio calls a beautiful deleveraging: a careful cocktail of the other three, calibrated to bring debt down without crashing growth. Every government aims for it. In practice it’s like landing a plane with almost no runway left, and even when it works, most of the lift comes from debasement anyway. It’s what we achieved post 2009, and which allowed us to avoid a 1929 style crisis.

So: austerity is refused, default is unthinkable, and the beautiful version still leans on the printing press. Debasement gets chosen again and again, government after government, in every heavily indebted democracy on earth.

Dollars are constantly losing value, and it goes beyond the level measured by inflation. The most sensible way to measure the debasement rate is the gap between M2 and real GDP growth (the mechanics of which we’ll go into more detail in the future).

The fiscal writing is on the wall in the US, in Japan, in China, and in the EU. Currencies have been and will continue to be debased as we attempt to engineer our way out of a debt problem.

This is the backdrop against which investing must happen, and it explains why since the GFC, investing has gotten weird, with valuations moving away from common yardsticks, and old prediction models no longer working.

Multipolar fracture

Outsourcing has been a beautiful source of growth as our participation rates peaked and dwindled. It allowed us to stretch beyond what demographics would imply, and to substitute efficiency gains for geographic arbitrage.

But that dividend has been digested, and has now reversed. The post 1990 equilibrium which brought us globalization and single markets and safe oceans is crumbling one year at a time, one conflict at a time.

Marko Papic and Peter Zeihan have each mapped this terrain from very different angles, and both run all through my thinking here.

Papic’s biggest insight is that we should ignore narratives, and instead focus on the binding political, economic, and geopolitical constraints to assess outcomes.

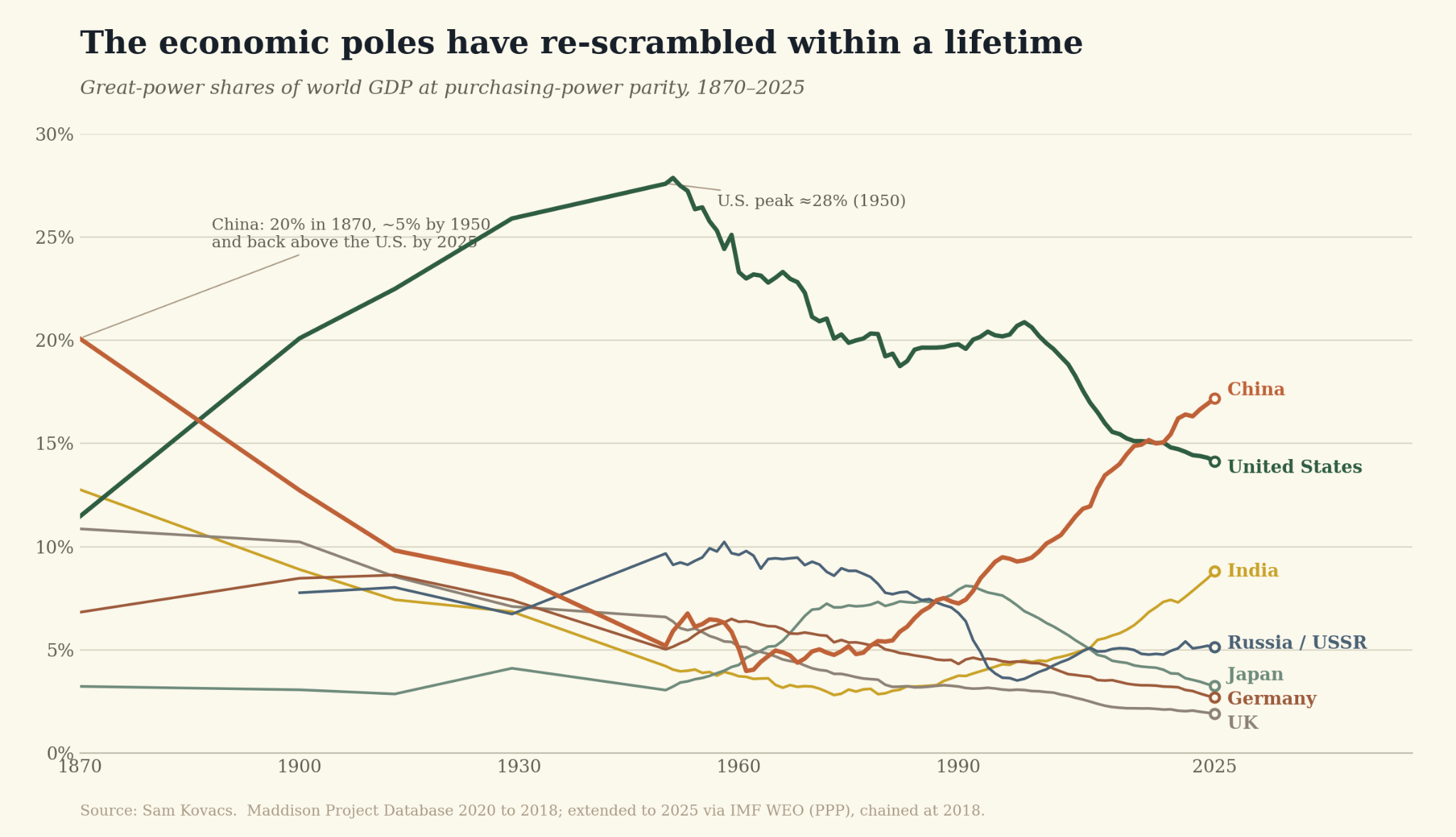

Zeihan’s biggest insight is that globalization is a temporary blip made possible by the US navy post WWII, but that as demographic stagnation and collapse (the same reason that is killing growth) accelerates, we will transition to a multipolar world.

I think we’re already half way there.

The clearest evidence is in what governments write about themselves. Read the recent national security and economic strategies of the United States, China, Russia, the EU, India, Japan, Iran, Saudi Arabia, the UAE, and Brazil side by side, and they agree on almost nothing, except the shape of the world they’re preparing for.

Even the United States now states plainly that it does not seek permanent global domination (NSS 2025 and NDS 2026 for those who care to check.)

The future is one in which: everyone needs to rearm, new payment rails and reserves get used, new supply chains are organized, and everyone enters a war on resources to fuel their regional economies.

A fractured world builds two or three of everything it used to build once. Multiple chip supply chains, multiple payment systems, munitions industries, etc. That duplication is staggeringly expensive, and expensive means inflationary when it comes from the top down, as it is suggested.

Debasement and multipolar fracture are the consequences of a demographic stagnation, insufficient productivity make-up, and years of pressing the debt button until it made us numb.

Investing as Babylon burns

Babylon was the original empire of accumulation: wealth, debt, grandeur, then decline.

Nothing is new under the sun, and once again it is clear that Babylon is burning.

Warren Buffett and Peter Lynch had it easy compared to you and me.

That means that investments must do two things: keep working whichever way the world splits and fractures, all while outrunning debasement (otherwise you’re just running on a treadmill, going nowhere).

If the currency loses 8% of its real value in a year and your portfolio gains 8 percent, you didn’t make money. Only the return above the rate of debasement is real.

Money has a half-life, which based on my research (which will be published also not so far in the future), the long term trending half-life is fourteen years.

A working life is forty to fifty years long which is three half-lives. Save a dollar at twenty and by your seventieth birthday it buys an eighth of what it did.

There’s only one way to clear a benchmark like that consistently: own things that grow faster than the money shrinks, or that cannot be compressed by printing money.

Cash loses by definition. Bonds pay you back in the very currency being debased. What outruns the fire is ownership of real, compounding assets, and the surest way to find them is to identify the secular trends, the forces so large and so entrenched that they’ll pull capital, revenue, and pricing power toward them for a decade or more, regardless of who wins the next election. Get the secular trend right and time does most of the work for you.

And here’s what makes this tractable instead of a guessing game: the trends flow straight downstream from everything described above. Governments that must debase create demand for assets they can’t print. A world that’s fracturing must rearm, must duplicate its supply chains, must secure energy and materials it used to buy freely. Societies that are ageing must spend on care, while younger ones build their first middle class. None of these are clever bets on what might happen. They’re consequences of what’s already happening, with budgets, laws, and demographics behind them.

The five themes

Follow that logic downstream and the field of what to own narrows to five themes.

Hard money. When governments inflate debts away, own what they cannot print: gold and the miners, silver, Bitcoin, and the few outlier currencies.

Resource scarcity. The world needs far more energy, metal, and materials for electrification, computing, rearmament, and rebuilt factories, after a decade of underinvesting in producing them. Demand is moving faster than supply can answer. Water is a resource. Oil is a resource. Cobalt is a resource. The grid is a resource. Semiconductors are a resource. This theme is defined quite loosely.

Global rearmament. Every major power is rebuilding its military at once, on a scale not seen in fifty years, and adding cyber defence on top. The spending is contracted years ahead and backed by governments. Some of the most beautiful Peter Lynch style growth stocks lie within this.

The demographic dilemma. The ageing that drives debasement also creates two trades: a rich world spending ever more on healthcare and elder care, and a young world forming its first consuming middle class. Both create opportunities of different scales

Restructured rails. The physical and financial plumbing of the world is being rebuilt for a fractured map: new factories, new payment routes, new exchanges, new places to clear capital. The owners of that plumbing get paid whichever side wins.

This was as compressed as I could do a presentation in this article, but I will obviously expand on all of them a lot in coming weeks.

It is by default a wide mandate, because in financial markets, the stories write themselves, and it would be foolhardy to lock ourselves out of too many assets.

Knowing what to own is half the job

Now of course here’s the thing. The gold bugs have been telling you to buy gold for decades. The Bitcoin maxis to go long bitcoin forever. The oil bulls to buy oil. The tech bros tell you to buy semis. The warmongers want you to buy defense stocks.

They are all right at times and all wrong at others. The greatest fallacy as an investor is to get married to an asset class, or worse an individual equity. Because known themes don’t pay out in straight lines.

A theme can be completely correct and still spend eighteen months going nowhere, or down, because it’s colliding with everything else that moves markets: interest rates, liquidity, the business cycle, sentiment.

Gold can spend years giving back gains after getting ahead of itself. Defense stocks can sell off in a recession no matter how full the order books are. Emerging markets can get crushed by a strong dollar even as their consumers multiply. Silver Tsunami investments can sometimes be just yield curve bets disguised, and not pay-off in the interim. The secular trend tells you what to own. It tells you nothing about whether this quarter is the moment to own it.

That’s why my commitment is to 1. not marry an asset class, 2. make positions time-bound with clear failure modes, 3. be brutally honest along the way.

My work will trickle down from the macro (theme, FX, rates), to the micro (fundamentals and price action).

Technical analysis will play the role where it belongs: at the last mile. At the end of the day you can have the best thesis and still lose money to poor timing. Price action is the synthesis of supply and demand for a given asset, and that carries information. My technical analysis is classical Richard Schabacker style, and it is used as a supporting tool once we’ve past an investment thesis through the waterfall of macro to micro tests.

One more thing, and it matters more than most investors realise: the portfolio is global by construction. Own a great business in a currency that strengthens against yours and you get paid twice. A portfolio confined to one country forfeits that entire dimension.

What’s next

On 15 August 2026 I’ll launch the paid edition of Babylon Burns.The date is the fifty-fifth anniversary of Nixon closing the gold window in 1971, the act that set this whole chain in motion.

Each week,there will be a macro read framed through one of the five themes and a deep dive into a single name investment. Behind it, a live global portfolio, concentrated, conviction-driven, every position disclosed, mirrored with my own money, with trade alerts,

Until then, there will be a steady run of free work. Next Letter, I put everything above on one live position for you to get the taste of the work for free: a single name where the theme, the chart, and the catalysts line up at the same time.

Two asks before you go. If you want the next letter when it publishes, subscribe, the free work alone will be worth your inbox.

And if this one was useful,, repost it wherever you found it, or send it to one person who you think will like it.

As Babylon burns, we’ll light the cigars.

Sam Kovacs

Babylon Burns is written for informational purposes and not to be construed as investment advice. I write about what I own and how I think. Your decisions are your own; do your own work before acting on anything here.

Sam, fantastic content. I will definitely be in this for the long haul. I am an old retired CPA/Economist/ long-term investor and you just gave us one of the most complete summaries of our current situation that I have ever read. I follow a number of brilliant people and YOU are now one of them. Thank you and I look forward to seeing more of your work

The part that resonates is not the usual “buy hard assets” conclusion, but the idea that the benchmark itself may be wrong.

If the unit of account is being steadily diluted, then nominal returns can create a false sense of progress. A portfolio can look successful in statement terms while failing in purchasing-power terms. That makes the debasement argument less about doom and more about measurement.

The multipolar fracture point adds another layer. If the old system was built around one reserve currency, one dominant security provider, and globally optimized supply chains, then a world of duplicated rails, regional blocs, reserve diversification, and strategic stockpiling is structurally more expensive. That cost has to show up somewhere.

The strongest caveat is timing. The secular theme can be right while the asset expression is wrong for long stretches. Gold, Bitcoin, commodities, defense, and infrastructure can all fit the story, but liquidity, rates, positioning, and valuation still decide when the trade actually works.

The key question is whether AI productivity becomes powerful enough to offset the debt and demographic drag. If not, the debasement/fracture framework becomes much harder to dismiss.