Why I'm buying a Norwegian microcap to play the Permian (and getting paid 12% to wait)

The Permian is the only swing supply for oil, and the best rig operator is priced for a depression

On the 28th of February 2026, the US and Israel went to war with Iran… You know what happened next.

Oil spiked, then came down dramatically on the back of jawboning, a fog of war that extended into the media, and a control of the narrative which suggested that the ceasefire was a stepping stone towards durable peace.

My 2 main picks during the crisis, Petrobas ($PBR) and Frontline ($FRO) are up a meek 8% and 12.5% from when I said “buy”, which quite honestly is not enough compensation for the emotional rollercoaster we went through.

I held those positions and some calls on $BNO which still look like they will expire worthless. I chose to move my focus elsewhere and come back if I saw a setup which would revive the thesis.

The oil market didn’t respond as anyone would have expected.

Either the industry has stopped behaving rationally, or there is something that everyone is missing. Shale was supposed to be the world’s swing supply, but so far in this crisis, it hasn’t stepped up, with oil rigs still at historically low levels.

Nonetheless, I believe now, once again, the risk/return on the oil trade is in our favor, as long as we make it in a differentiated way.

This article will bring you through the logic of why I believe that a bet on rig count and daily rates in the Permian Basin is one of the most interesting setups right now.

I will also offer a stock pick which I believe is particularly interesting.

The only credible short term supply left is the Permian

We are all finding out in real time that the war is not resolved. Renewed strikes in the past week are likely cementing impairment in Hormuz which cannot forever be compensated with drawing of the SPR, in the US but also in China.

Incremental supply comes from only a short list of places: Guyana and Brazilian pre-salt will continue to provide more, but on a known schedule as there is nothing which can be decided today which will result in more barrels before the end of the decade at the earliest.

Washington has already used its trump card (no pun intended) of un-sanctioning barrels.

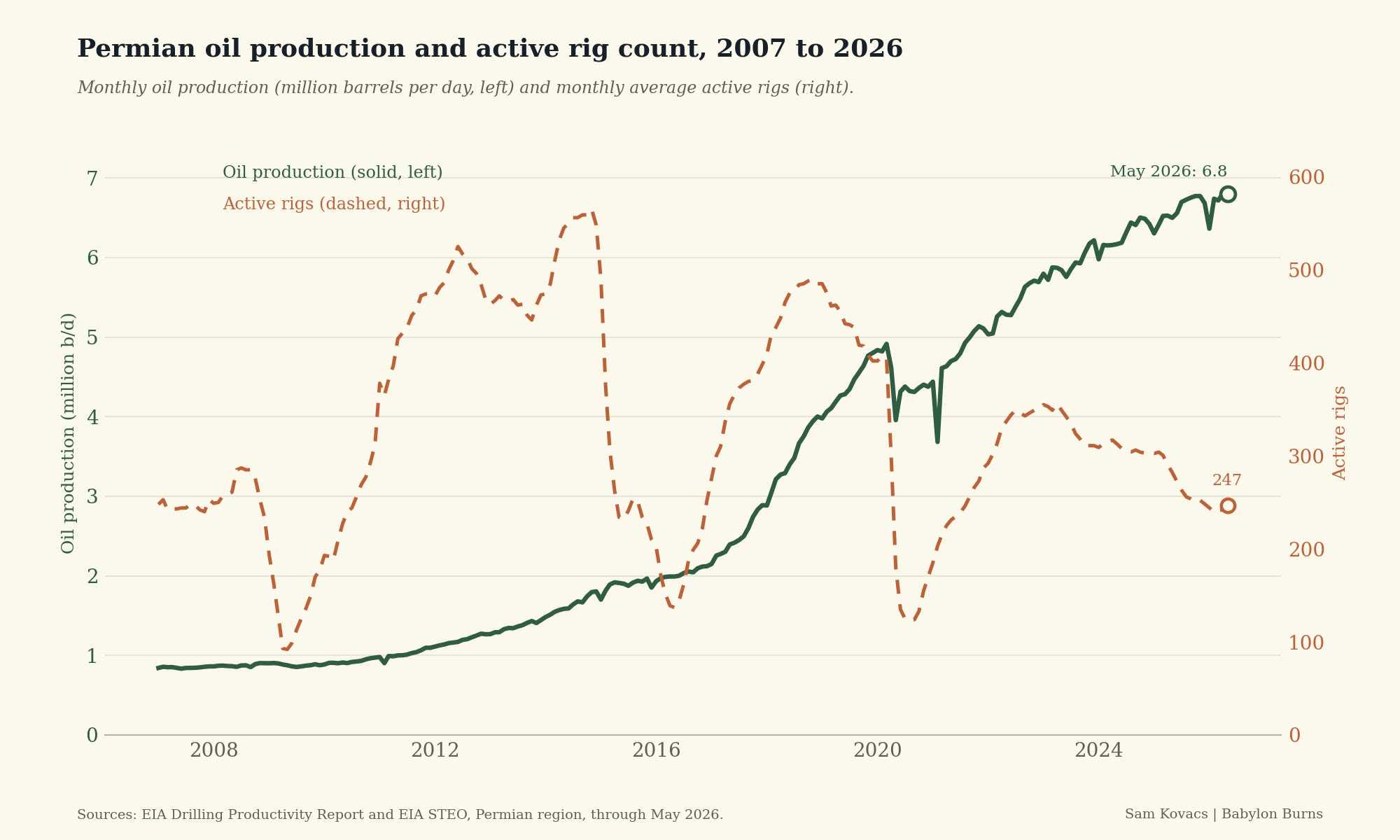

The only credible supply on earth that can turn a decision today into production within a year is the Permian.

And the Permian supply is a function of drilling rigs.

I believe that the current administration will continue to attempt to dunk on every rally in crude oil, and at times succeed.

As a lot of us found out in the first round of the conflict “we fought the law, and the law won”. China is and remains the wildcard that blindsided a lot of us.

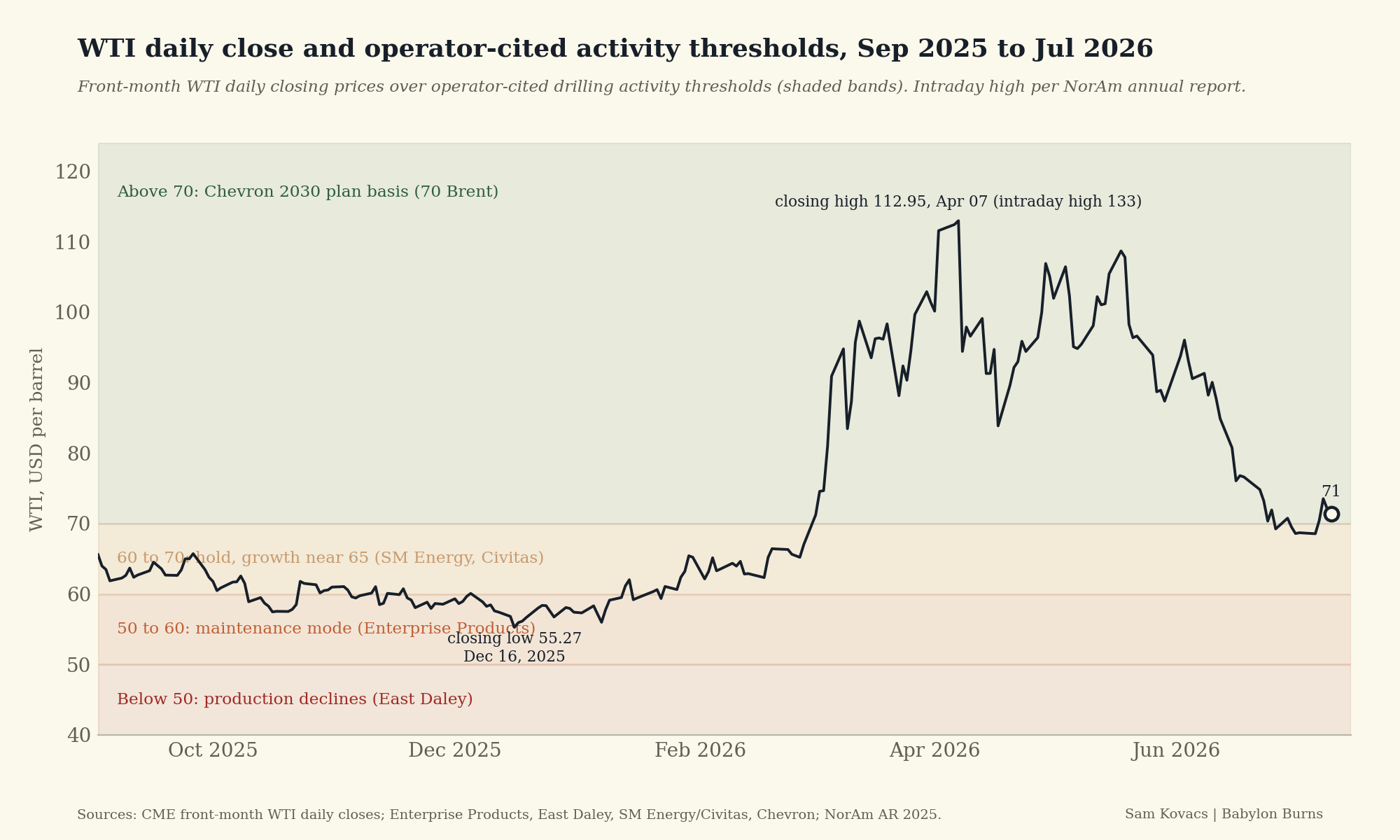

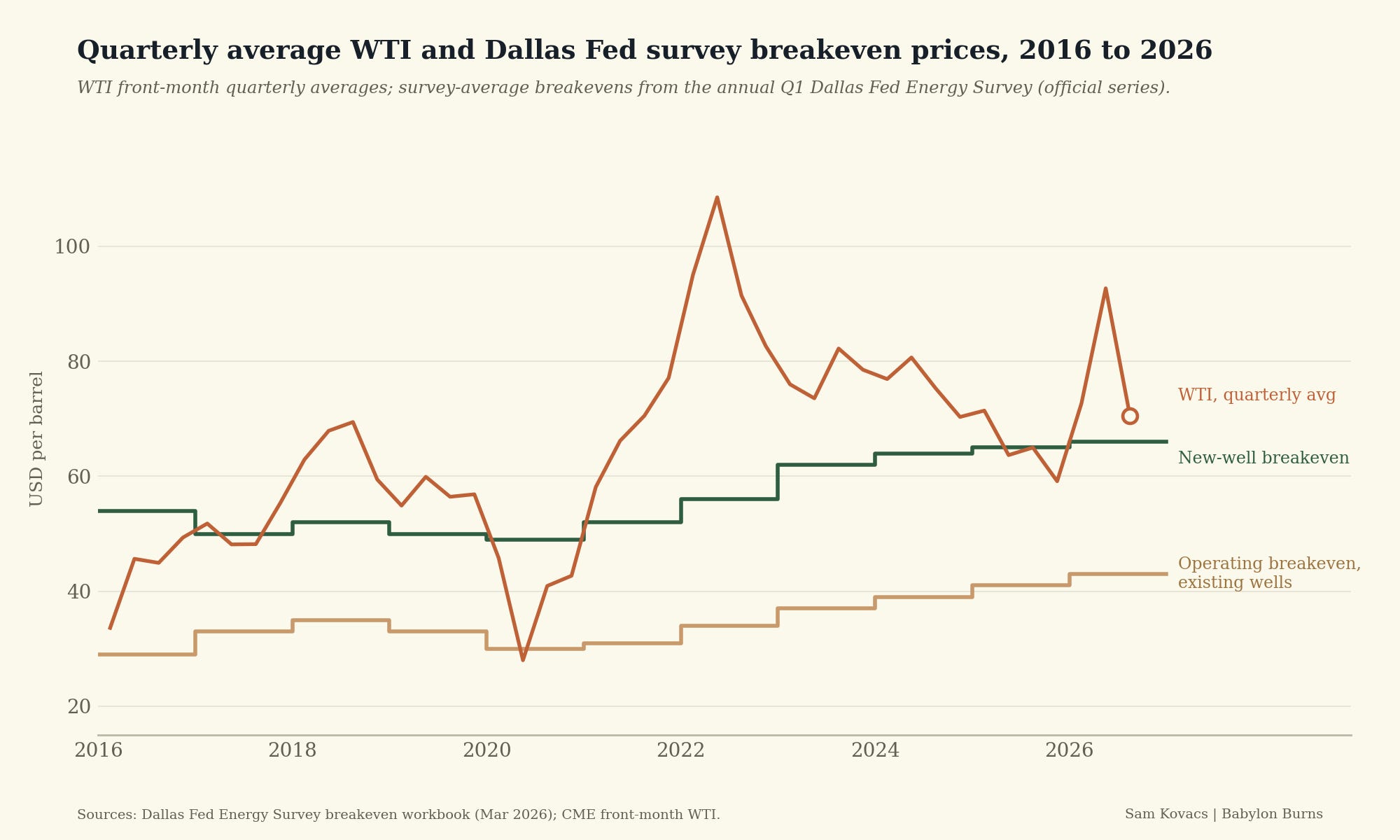

But the price of crude seems to have settled above the $70 Brent on which Chevron built its 2030 Permian plan.

The longer the price stays above this level, the more likely we will see an increase in the number of rigs, at the very least, it puts a floor under the number.

Chevron is one of the most conservative planners in the space. At $70+ its 2030 plan is fully funded. Exxon, which is the other major which dominates the basin, has committed to growing Permian output.

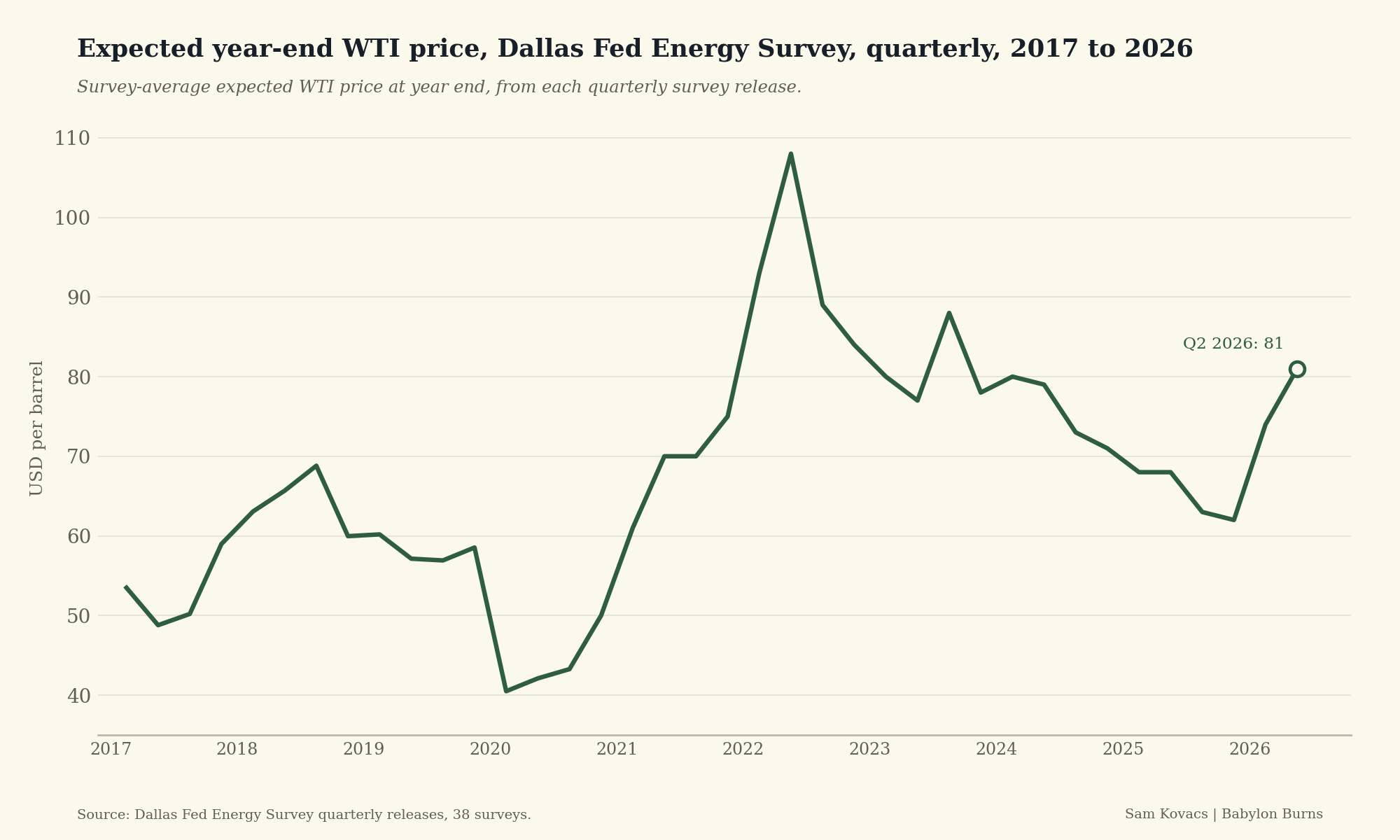

The Dallas Fed Energy Survey is seeing year end price expectations being reanchored higher, as operators are slowly forming a view in line with what I’m saying.

Understanding the decline problem in shale

Conventional wells produce oil at roughly stable rates for decade. But horizontal shale wells produce a surge upon project completion, which then declines by 65% to 85% within the first twelve months.

The consequence is that shale basins are flows which must be continuously rebuilt. The industry measures this rate by what they call “base decline”: the share of production which will disappear within a year if drilling stops.

The Permian basin’s base decline was approximately 34% in 2018, 40% in 2019, and is now between 45-50% as the current wells have gotten younger.

At the current production rate of around 6.8mbpd, that means that around 3mbpd of capacity is lost each year and must be replaced by new wells for any future growth to be possible.

So the rigs which are working the Permian are mostly replacing existing capacity rather than expanding capacity.

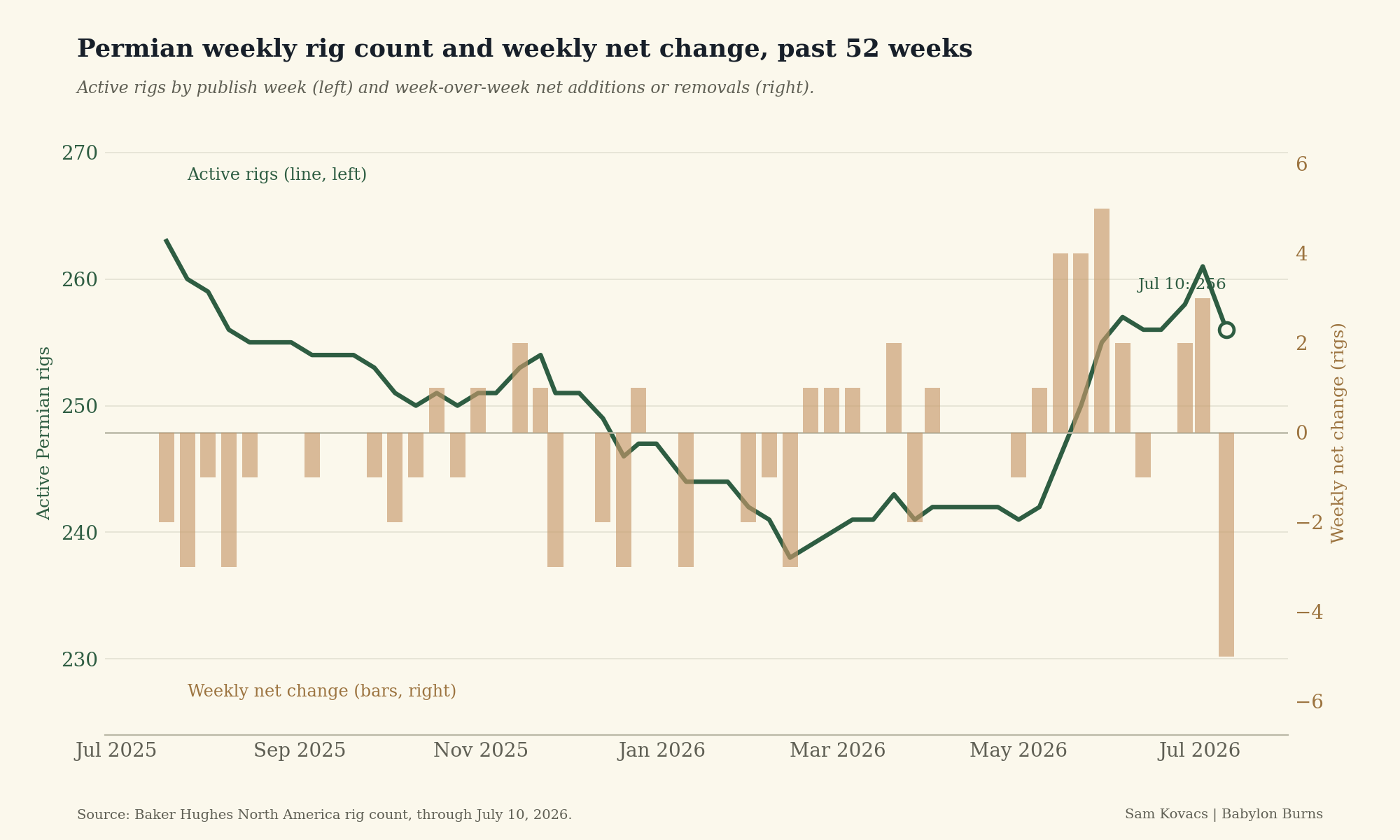

However, rig count fell by a third from 2023 while production increased by 16% since then.

Why are decreasing rigs leading to increased production?

There were two contributing offsets which allowed production to keep increasing while rigs have been in decline since early 2023, both of which are rolling over.

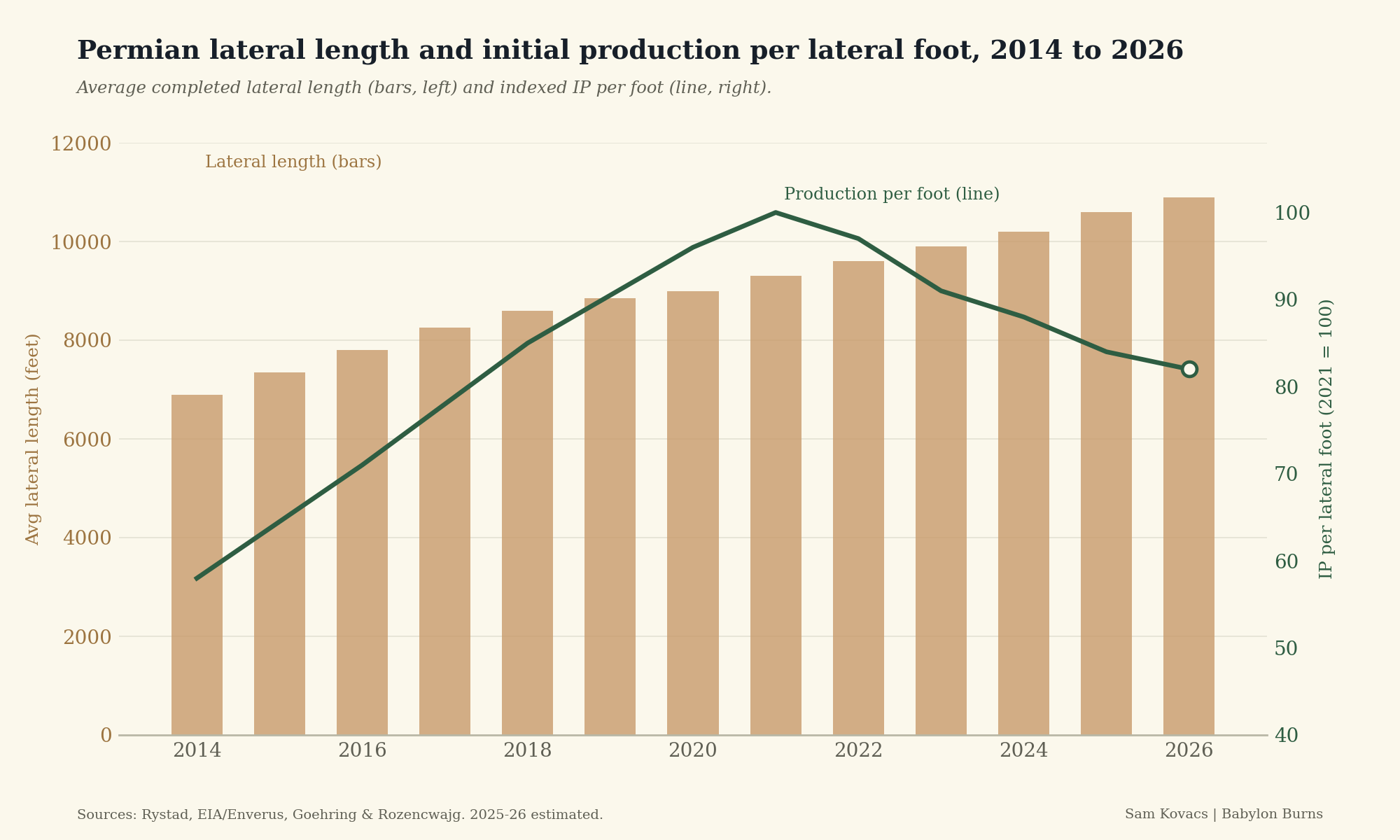

The first is: longer laterals have been masking lower quality rock.

Shale wells run vertically down to the target formation (where the oil is), then rotate and run horizontally through it (the lateral). You can roughly scale up output to the length of the lateral.

So while you might see headline numbers being reported as output per well, output per lateral foot measures how productive your rock is.

Until 2021, production per foot and lateral length both increased, as the 2015-2016 and 2020 price busts forced everyone to operate their absolute best rock to remain in business. Goehring & Rozencwajg's work explored this idea in detail: a large part of the shale miracle was simply selecting higher grade rock.

Of course, superior engineering also played a role, with each foot getting cracked much harder, with more and more sand (to let the oil come through the rock, you frack it, which means you put high pressure water and sand until it cracks, and the sand keeps those cracks open for the oil to flow). Better technology and tools also enabled superior extraction.

But since 2021, that number has been declining, as the best rock has been declining. The Permian is 60% through its tier 1 rock, and every year the average new well is on worse acreage than the previous.

This has been masked by laterals getting longer and longer, from about 5,000 feet ten years ago to over 10,000 feet today. 15,000 foot wells are now somewhat routine, but these are close to both the mechanical and economic limit, meaning that they are unlikely to continue increasing forever.

The second offset was the completion backlog.

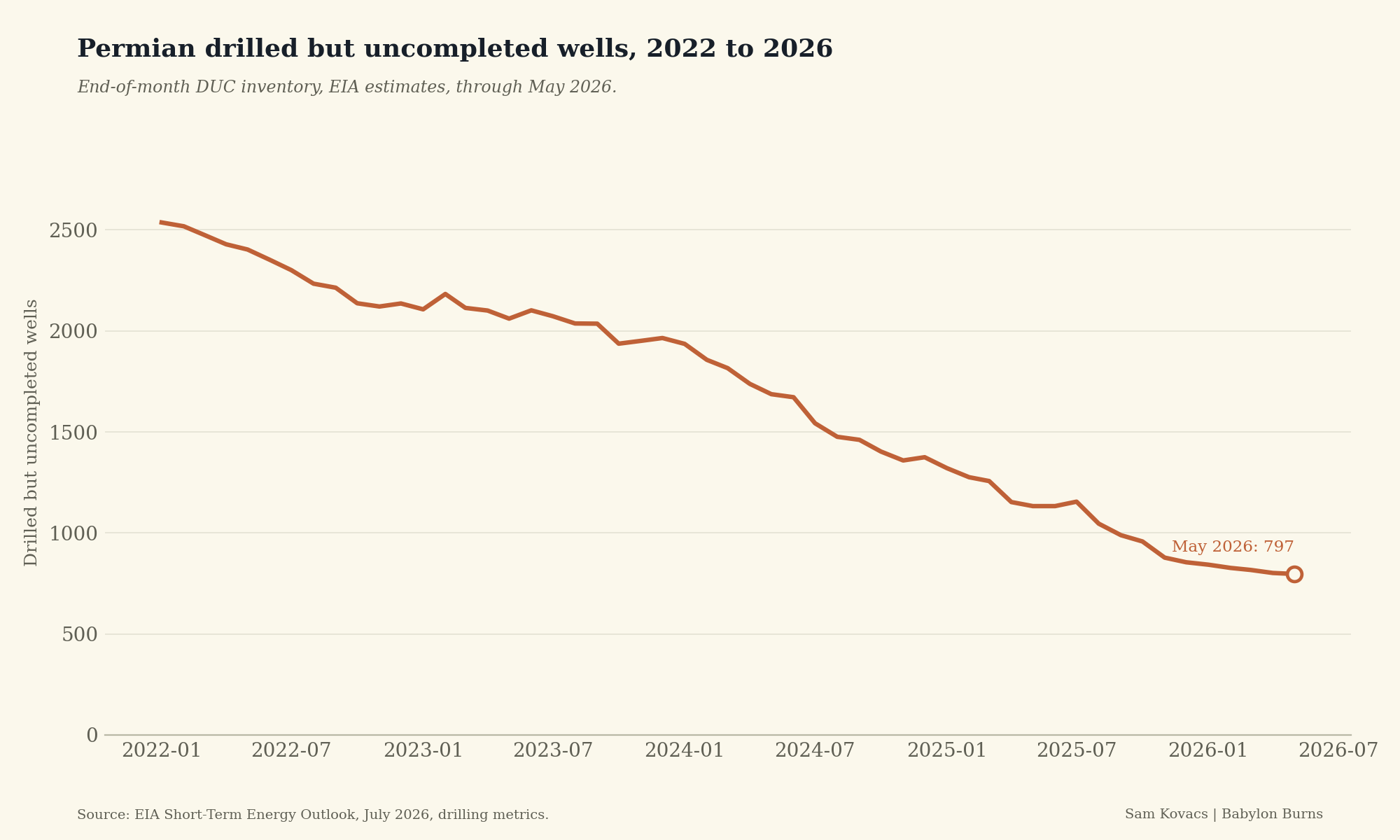

Shale wells are built in two steps. First the rig drills the hole, and then a seperate crew fracks and completes it later, at which point production starts. If you don’t complete it it’s considered drilled but uncompleted (DUC) and just sits in inventory. You can drawdown your inventory until you can’t.

In the Permian, DUCs peaked in 2020 as 3,500, and have been in freefall ever since, now down 75% to below 800.

(The chart below only shows since 2022 due to a change of methodology in counting at the EIA).

The DUC’s have mostly flatlined in 2026, as we are likely reaching the trough in the inventory drawdown. There are about 450 wells drilled per month, so you always have somewhere above 600 which are just waiting to be completed. Add in an extra buffer, and some dead stock, and the fact we went from drawing down DUCs at a rate of 49 wells per month in 2024, 43 per month in 2025, and only 11 per month in 2026, and the picture is clear: the drawdown is over.

So we managed to reduce the number of active rigs by always increasing the number of feet per lateral, and by using up the inventory of wells that were already drilled.

Both of those have expired now.

So what does it take to add back rigs?

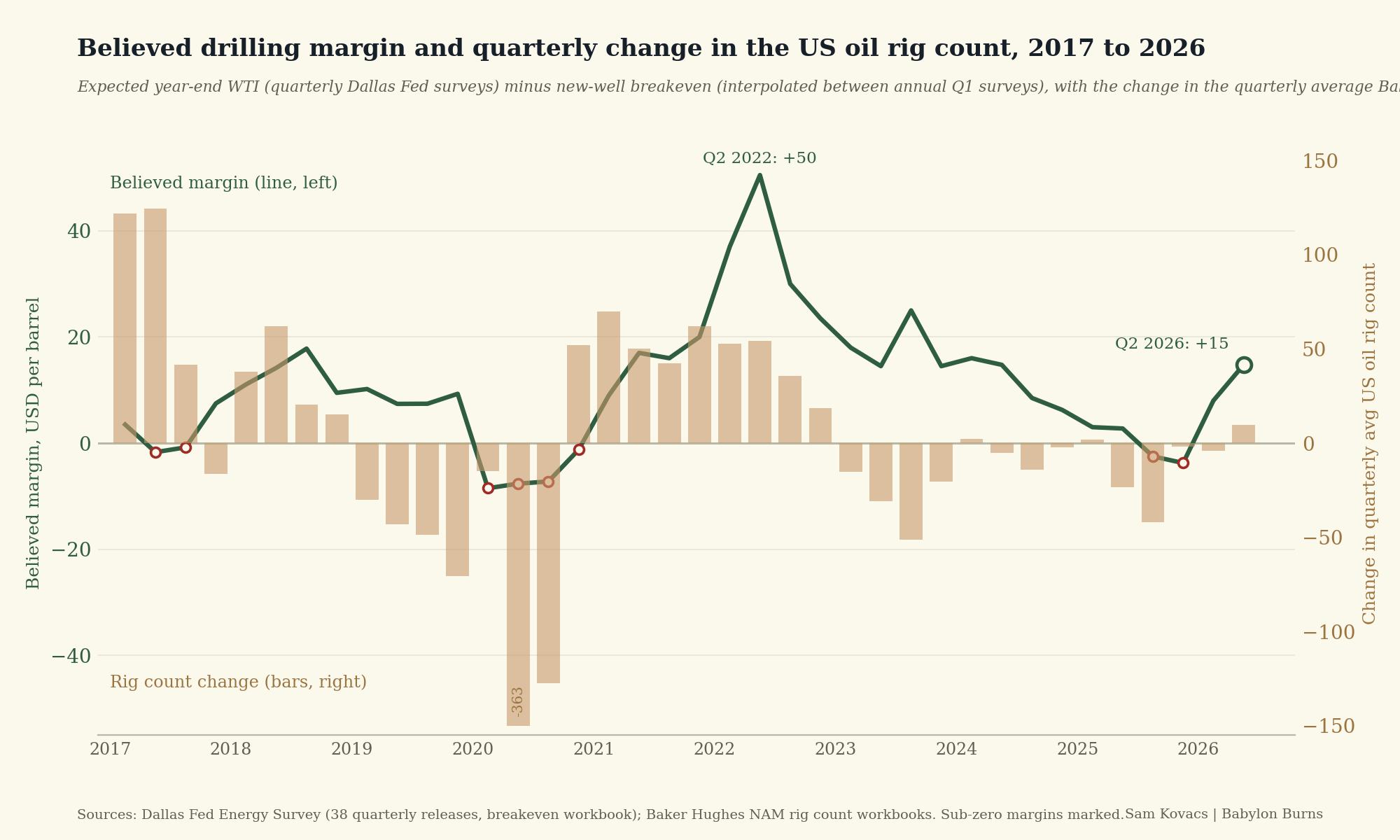

Oil went super high earlier this year but we didn’t start adding rigs until May. Why? Nobody is drilling a well if they do not believe that WTI will be high enough to cover operating costs.

And like I said above, the quality of the rock has declined, so the breakeven on a new well has gone from around $50 in 2016 to $67 today. The cheapest inventory has been drilled.

And thanks in part to jawboning and the promise that “peace was just around the corner”, nobody believed that WTI would sustain a very high price through the year end amid the conflict. Expectations reset higher, but not dramatically so.

In 2022 when everybody expected oil to be well above the breakeven, more wells were drilled which brought in more active wells. In 2025, new-wells were unprofitable on average so less were drilled and active rigs took a nosedive.

In 2026, with the expectation now above breakevens, we saw the first quarter with a meaningful increase in average oil rigs since 2022.

So to wrap up everything I’ve covered about the Permian so far:

Replacing output declines forces drilling or production cuts.

Replacement means that even in Q4 2025 we barely cut rigs despite unprofitable margins.

Reductions in rock quality and limits to efficiency mean more wells are needed to replace supply.

We have drained the inventories of DUCs.

The margin has now recovered and is likely to remain at a level which supports real activity.

But rigs are not all made equal

The top line analysis here has measured rigs as one fungible asset class. But treating the total count as a single market is a mistake which investors unwilling to go the extra analytical mile are leaving for us to pick up.

Drilling a 3 mile lateral through hard rock requires a specific class o equipment: enough horsepower and an AC electric drive to turn and steer miles of pipe, a walking system that moves the rig between wells on a pad without disassembly, and racking for the pipe itself.

These are known as super-spec rigs, and rigs below this spec are getting less demand. Of the 1,059 rigs in the US that are available, only 613 worked at all last year, and roughly 450 of these are super-spec.

When activity falls, operators start by releasing the lowest capability rigs first and keep the best ones working.

If activity picks up, then the demand for super-spec rigs is where all of the demand concentrates as the requirement for longer laterals can only be fulfilled by these.

Helmerich & Payne ($HP) is the market leader with about a third of these. But their operations span the full Lower US, Middle East, Latin America, and Australia.

So this thesis would be best expressed by a drilling contractor which owns only super-spec rigs, and operates primarily in the Permian.

There happens to be a stock which ticks all those boxes, pays you a 10% yield to wait, carries no debt, and is cheap as chips.

Of course this doesn’t come without a few risks.

It isn’t listed in the US, the dividend payout was cut by 72% in the previous downcycle, the controlling family has bankrupted a drilling company before.

Nonetheless, I think you will agree that this is an opportunity too good to skip.

How this idea came to be

Investment ideas never surface in a vacuum, and this one is no exception.

So before I unpack it, let me hat tip the gentlemen who were involved in me surfacing the idea.

I was talking on an X Space hosted by George Noble last month. During the call I was introduced to Matt Polyak of Hummingbird capital, who said he was particularly interested in oilfield equipment stocks.

The details of the thesis weren’t fully exposed, but it got me thinking:

If the Permian is to be the swing supply once we have emptied the SPR, then rigs come back, and this comes with orders for pumps, rig components, wellheads and other bits.

I didn’t act on the information, until I came across a post on X by Calvin Froedge, naming this little stock.

A lightbulb went off: Don’t trade the second order effect, trade the mispriced first order effect. Why go for the trickshot when you’re offered a couple free throws?

So thank you gents.

Introducing: NorAm Drilling

The company is NorAm Drilling, ($NORAM on Euronext Growth Oslo).

This is a Norwegian holding company, within which is nested a Texas Operator headquartered in Houston, which runs 11 rigs in the Permian.

The current market value of this company is around $170 million.

All 11 of its rigs are what the company calls “ultra super-spec” capable of drilling for both oil and gas.

Their fleet ranks near the top of the Permian’s rankings on feet drilled per day, and 7 of 11 rigs are contracted to major E&Ps.

Oh, and one rig even won rig of the year within a supermajor’s program… So they have the MVP of rigs.

The stock is as pure an expression of the thesis presented in this article you could hope for: No external debt, a two person executive team, just over 300 employees, and all-in cash cost of roughly $24K per day, making it the lowest breakeven in the industry.

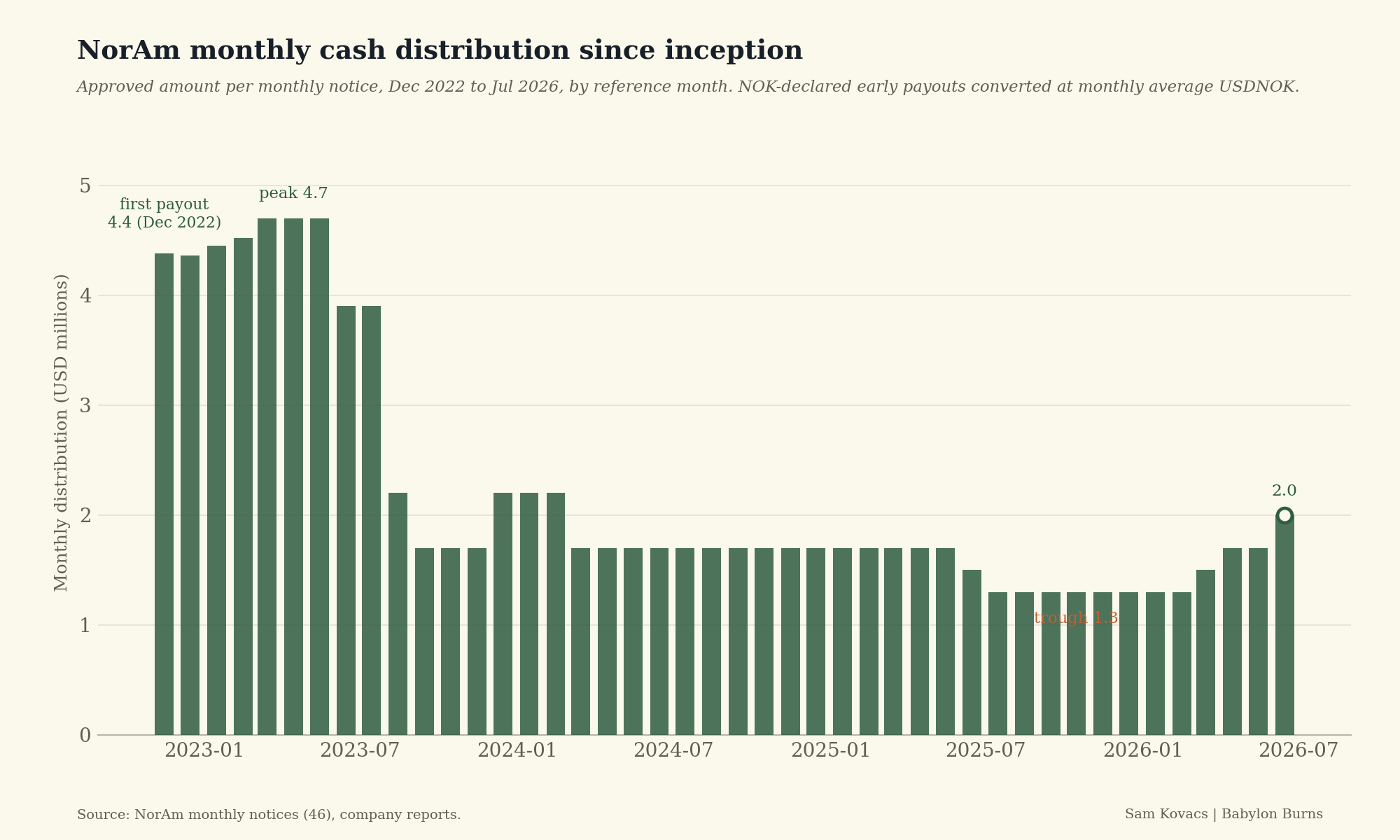

They distribute all their free cashflow as dividends monthly. The stock currently trades at 42 NOK, and they currently pay out 0.45 NOK in dividends per month which annualizes to 12.9%.

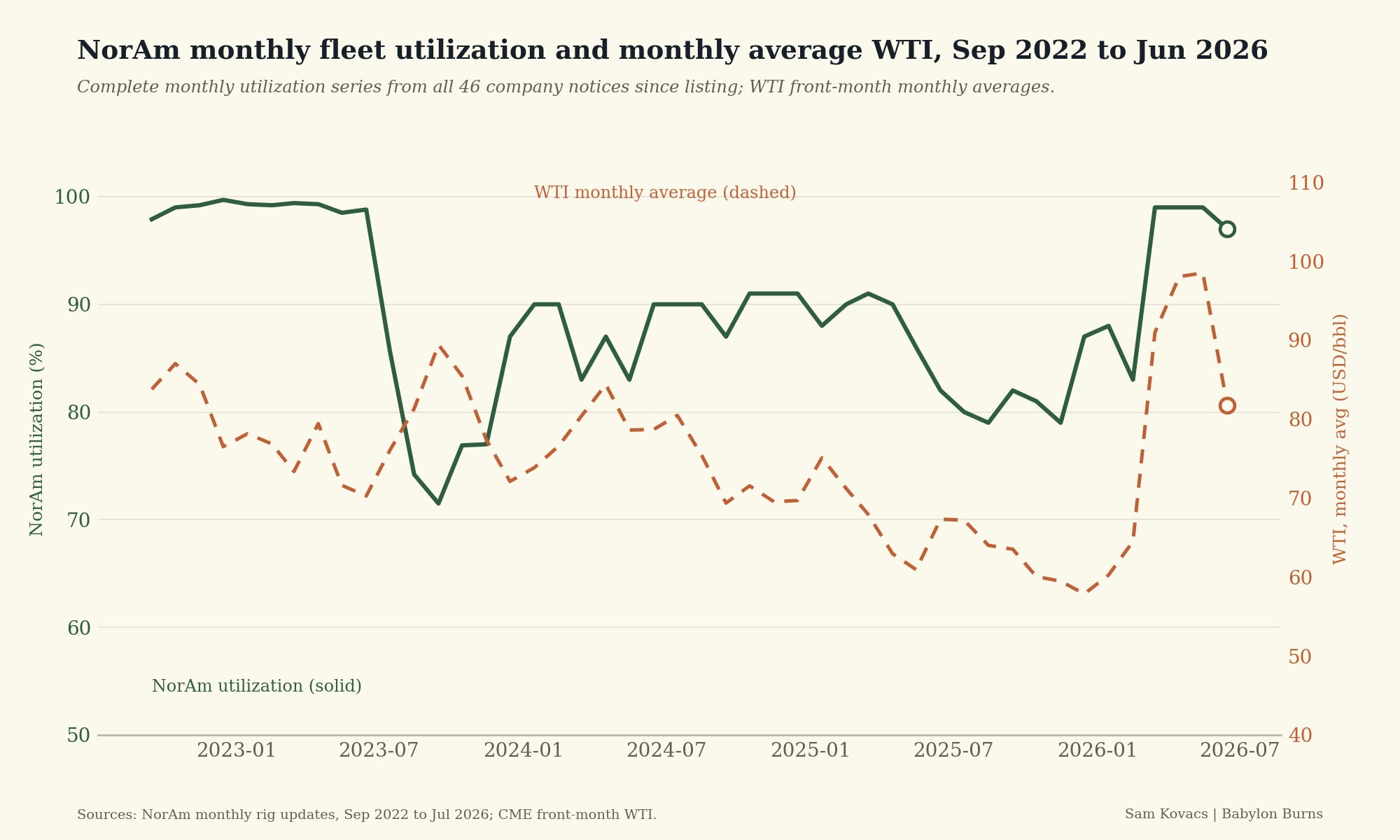

The economics on the stock are a function of two things: utilization rate and the day rate on their rigs. Utlization is currently at 100%, which works out to about 3,930 rig-days per year. This means that each $1,000 of realized day rate add about $3.9 million of annual EBITDA against a $178mn enterprise value.

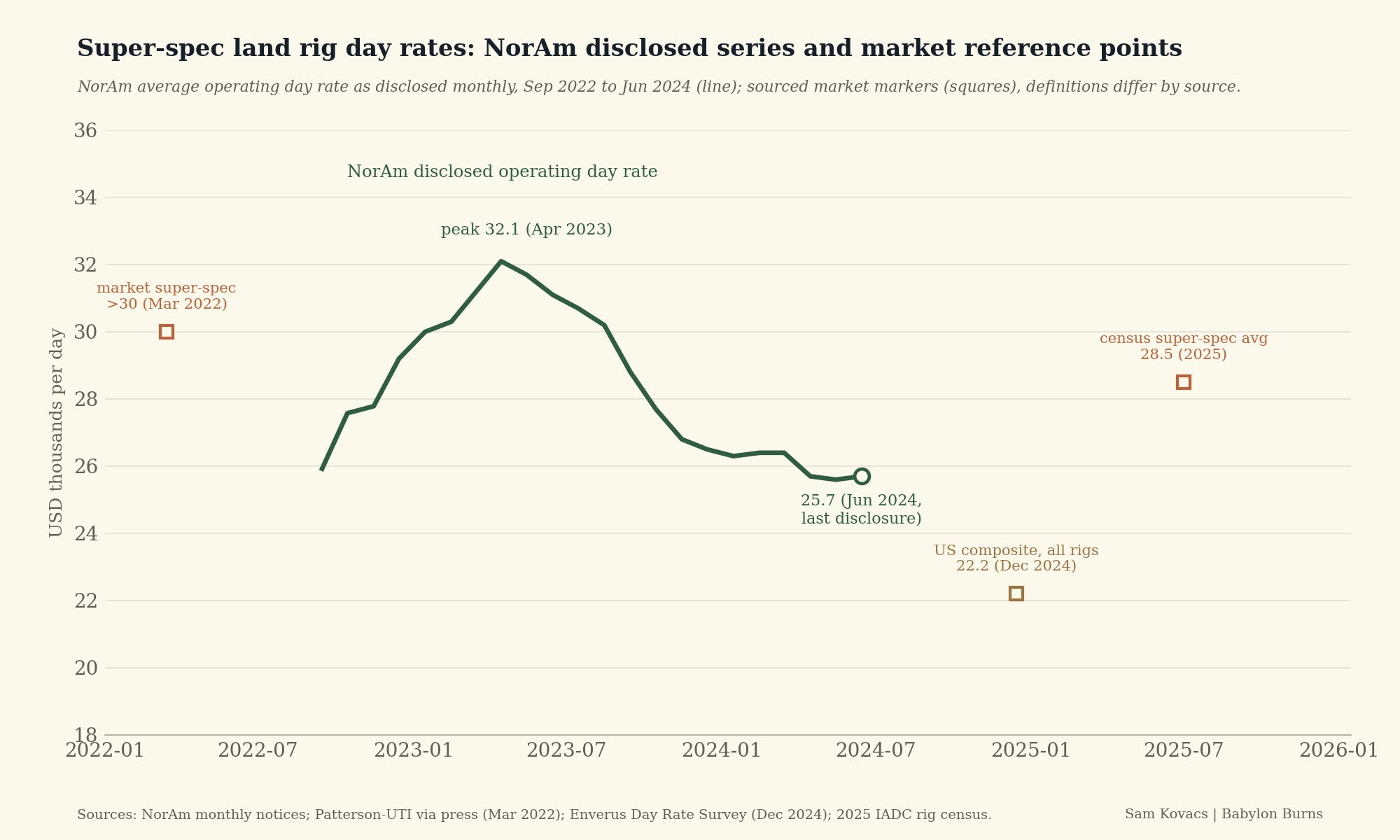

The company stopped reporting its day rates in June 2024, as it was the only company doing so monthly, and likely giving a clear signal to competition in a declining market of by how much they needed to undercut NorAm.

What is interesting though from the chart above though, is that we can see that the peak in day rates in the previous cycle came a full 10 months ater WTI peaked. Running a correlation against WTI confirms this: about 0% correlation against current price, but 0.8 against the price 10 months back.

NorAm’s utilization rate corroborates the replacement drilling thesis I established earlier. It continued drilling in 2025 at around 80% utilization whilst WTI was between $60 and $65. Premium rigs were hired at the bottom of the cycle because the drilling simply could not be deferred.

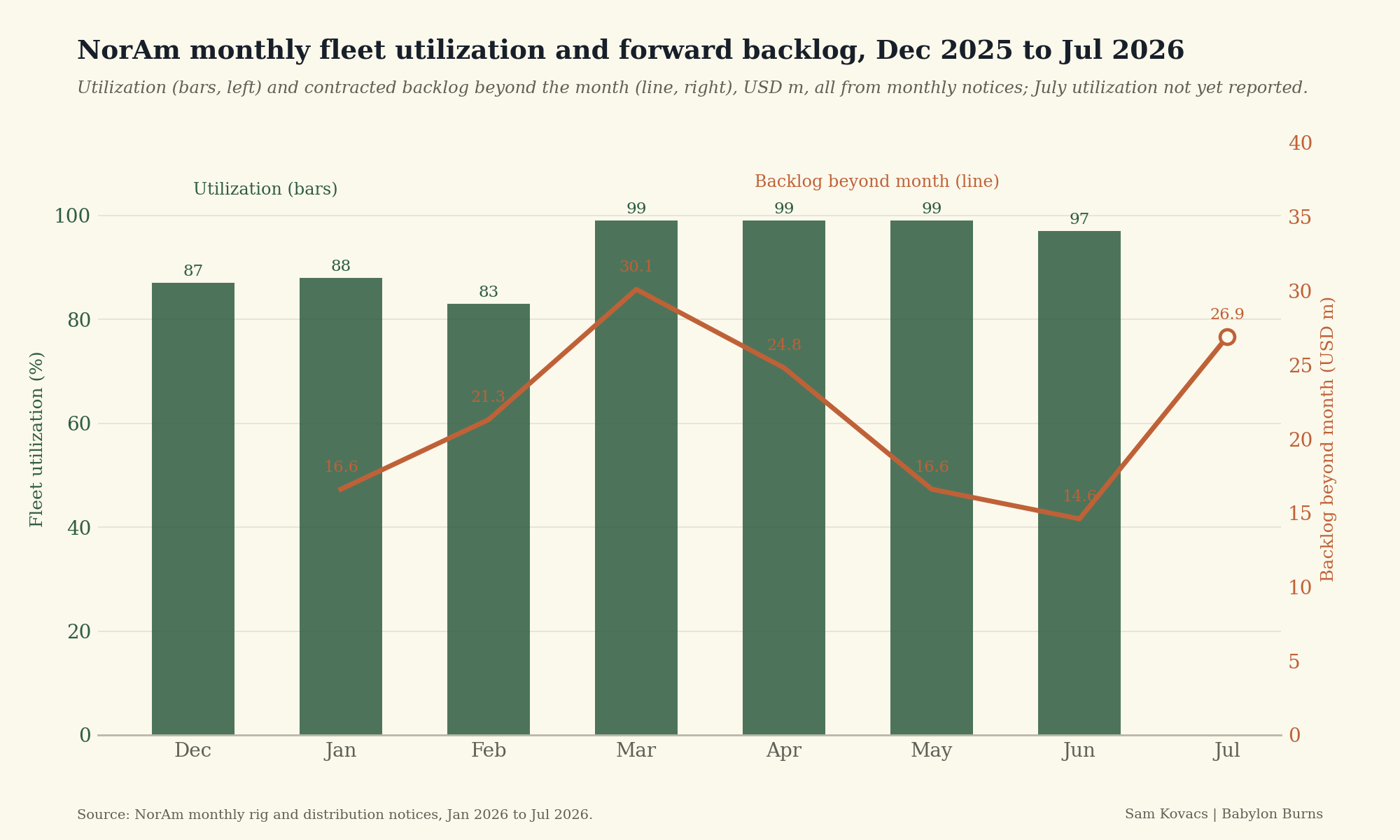

Utilization is at 100% or close to it, with the backlog a solid 16% of enteprise value. If what I said about realized day rates coming through with a log holds, then we’ve got a natural rise in EBITA which will flow through to shareholders as dividends over the next year.

The controlling shareholder

Geveran Trading and SFL Corporation own a majority of NorAm shares. Both are controlled by Fredriksen, who has a record of buying cyclical assets at a trough and taking investors along for the ride with him.

John Fredriksen was born in 1944 in Oslo, who left school in his teens and started as an errand boy at a shipbroker. He learned the oil trade in the 60s chartering tankers out of Beirut, and bought his first ships in the mid 70s slump.

He made his fortune in the 80s hauling crude out of Iran’s Kharg Island through the middle of the Iran-Iraq war, at great risk.

He built Frontline into a very successful tanker company, consolidated Mowi into the world’s largest salmon producer. His approach has been consistent over 50 years: buy cyclical assets near the bottom, distribute cashflows throughout the recovery, and take ownership of the same security class as minor investors.

His track record does have one chink in its armor, which comes in the form of Seadrill.

Fredriksen founded Seadrill in 2005 and built it, with debt, into the largest offshore driller in the world, worth more than $20 billion at the 2013 peak and carrying about $14 billion of liabilities.

When oil fell in 2014, the debt forced Chapter 11 in 2017; shareholders kept 2 percent. The recovery never came, because shale had taken offshore's role as marginal supply, and the company filed for bankruptcy again in 2021. Shareholders were wiped a second time, and this time Fredriksen let it go.

Mistakes force lessons, and I believe, with NorAm, these lessons were learned: financial leverage on-top of operating leverage is what will kill a drilling company, a drilling cycle can be misjudged for years, and you should not expect the owners to defend a losing position.

How is this thing so cheap?

At 42 NOK, as I mentioned above EV is around $178mn. I always reverse engineer valuation rather than project forward.

I try and answer the question: Given the current price, what growth rates and conditions is the market pricing? If my thesis disagrees with the market pricing, we can comfortably enter the position.

Let’s assume an 11% required return, which is appropriate for an illiquid, cyclical, microcap. That would assume $22mn in EBITDA. 2025, which was the worst year on record generated $20mn in EBITDA.

So the market is currently pricing the worst year on record as the permanent state of the market.

If we witness anything like a return to 2023 conditions, when NorAm generated $40mn in EBITDA, this stock would be worth double what it is today.

Of course with cyclicals it is always difficult to pinpoint valuations, but NorAm is trading at 8x trough EBITDA.

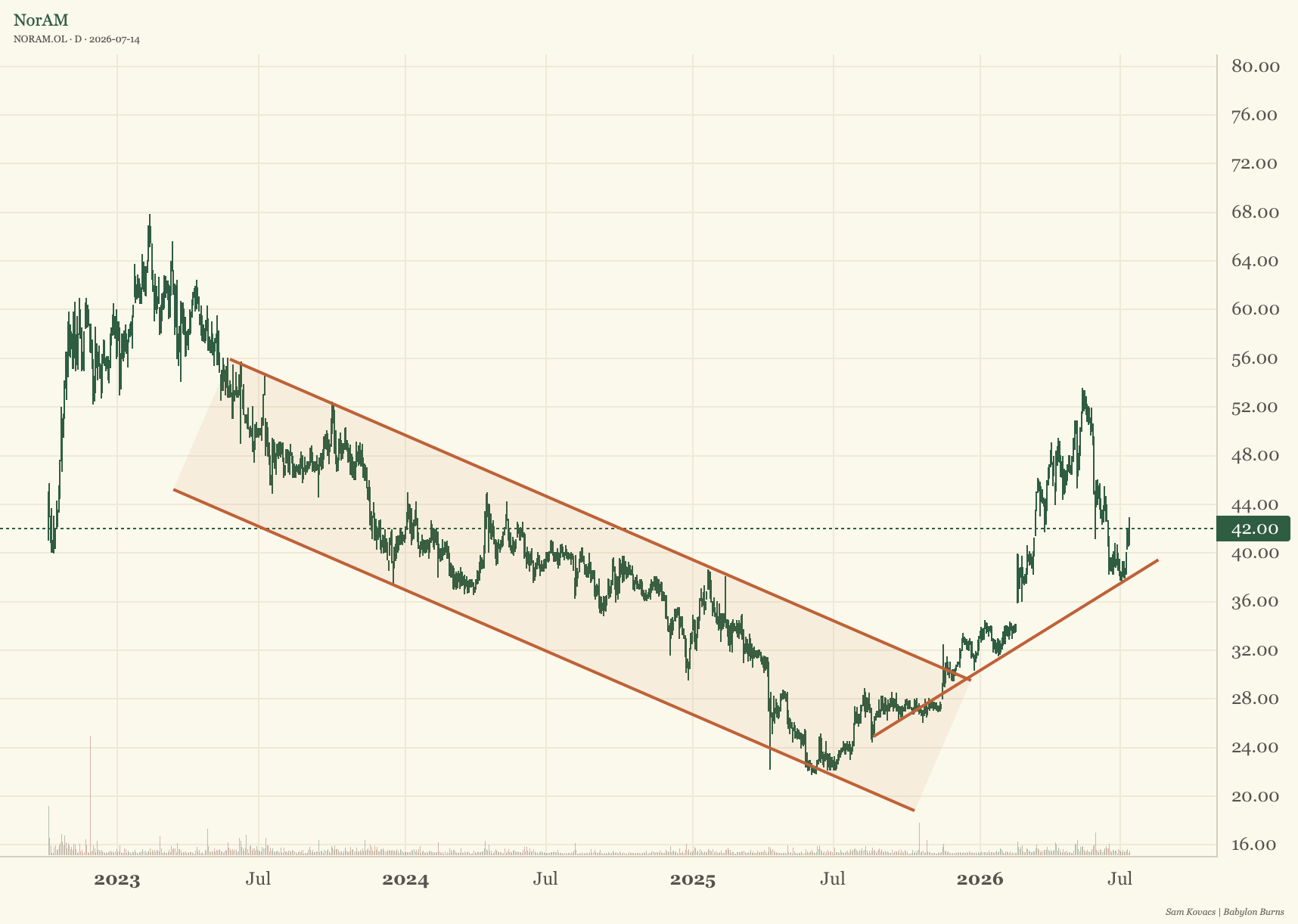

The stock repriced to NOK 53 in May before declining on the back of a perceived piece in Iran.

From the technical front, 2026 has marked a clear move away from the descending channel of 2023-2025, and while it’s still early, we seem to be seeing an emerging trend line which should give us support in the $38-$42 range throughout the third quarter.

I’d place a stop loss at NOK 35, which would be a break from the current environment and a return to the prewar pricing. If price goes there, we likely want to be out and reconsider what is happening. 17% below the current price means you can size at 5-6% if you want to put no more than 1% of your capital at risk.

I believe the market is pricing extreme bearishness on the conditions in the Permian which simply do not add up with a $70+ oil world.

At its 2023 peak, NorAm paid $4.7mn per month in dividends, but by late 2025, it was only paying $1.3mn. If WTI settles in the low $50s, then we’re looking at going back to those days and to the lower valuations.

I just don’t see that happening. I think that the current conflict, which let’s not forget, is the largest supply disruption in the history of oil, likely puts a floor under oil prices for a while. That’s what the price action has underwritten so far.

How long will China underwrite oil prices for the entire world by drawing down on its massive SPR?

Wrapping it up

I believe this stock is a perfectly fine way to play the world we are entering in. You get a double digit yield, optionality on a rerating to give capital returns of 50% to 100%, and a downside which is capped if you believe that the US Iran woes are more complicated than previously marketed.

If you enjoyed this article and it was of value to you, I will ask a couple things of you.

First please make sure if you haven’t yet to subscribe to this newsletter. You can opt-in for free and continue to receive all the free content I will be sending your way weekly for the next month.

You can also decide to pledge a subscription.

I am still deciding on the ultimate prices for the subscriptions.

In the meantime I have left the pledges well below whatever the launch price will be, as I want to do a little something for early readers and people who get with the program early.

So if this was valuable to you, subscribe, pledge, and share to someone who will enjoy this article.

As Babylon Burns, we’ll light the cigars.

I think it was the US and Isreal that went to war with Iran, (typo in the first sentence)?

Nice stock, but many people have been burnt by Frederiksen. FRO used to pay close to 30% dividends at some point and it was a warning signal. I own TALOS and while it’s a different story, both companies’ stocks correlate strongly with the oil price and with each other. Buying oil futures offers the same price action without the idiosyncratic risks.