Why I'm not touching gold miners with a 10ft pole (yet)

Gold, why I like it, why gold miners are awful investments, and when you should still buy them.

Gold permabulls are mostly idiots.

Actually, single asset, or sector permabulls are mostly idiots.

Investing works in seasons. Certain assets do well in certain environments, and others do better in other environments.

Being attached to a single asset like it’s a sports team, is a weird, puerile,

In this article, I will show you exactly why a lot of “investors” are misguided in their unabated bullishness in gold.

I’ll show you what, how, and when to make the most money in the gold trade.

Sound good? Let’s dig in.

(PS: before we do, if you haven’t yet, consider subscribing for free to the newsletter. Until August 15th I will be giving away a weekly supply of FREE in depth articles exposing my thesis, how I think about different investment opportunities, going from the macro read to the micro minutiae.)

Gold is money. Everything else is credit - J.P Morgan

When J.P Morgan testified in front of Congress he made a very clear argument. Money is gold, and nothing else. Money is a scarce, fixed, physical, finite thing, whereas credit is fluid, judgment based and relationship driven.

He was arguing that credit wasn’t something which was mechanical and controllable, and therefore wasn’t money.

Fast forward 114 years later, and we are now 55 years into a full-fledge fiat monetary system, where most of what we call “money” today, is nothing more than a bank deposit, or in other words, credit which depositors extend to their banks.

What’s more is that since 2009, we have moved from the private sector being the multi-node controller of credit creation, to the Fed having the most discretion over how much money moves in and out of the system.

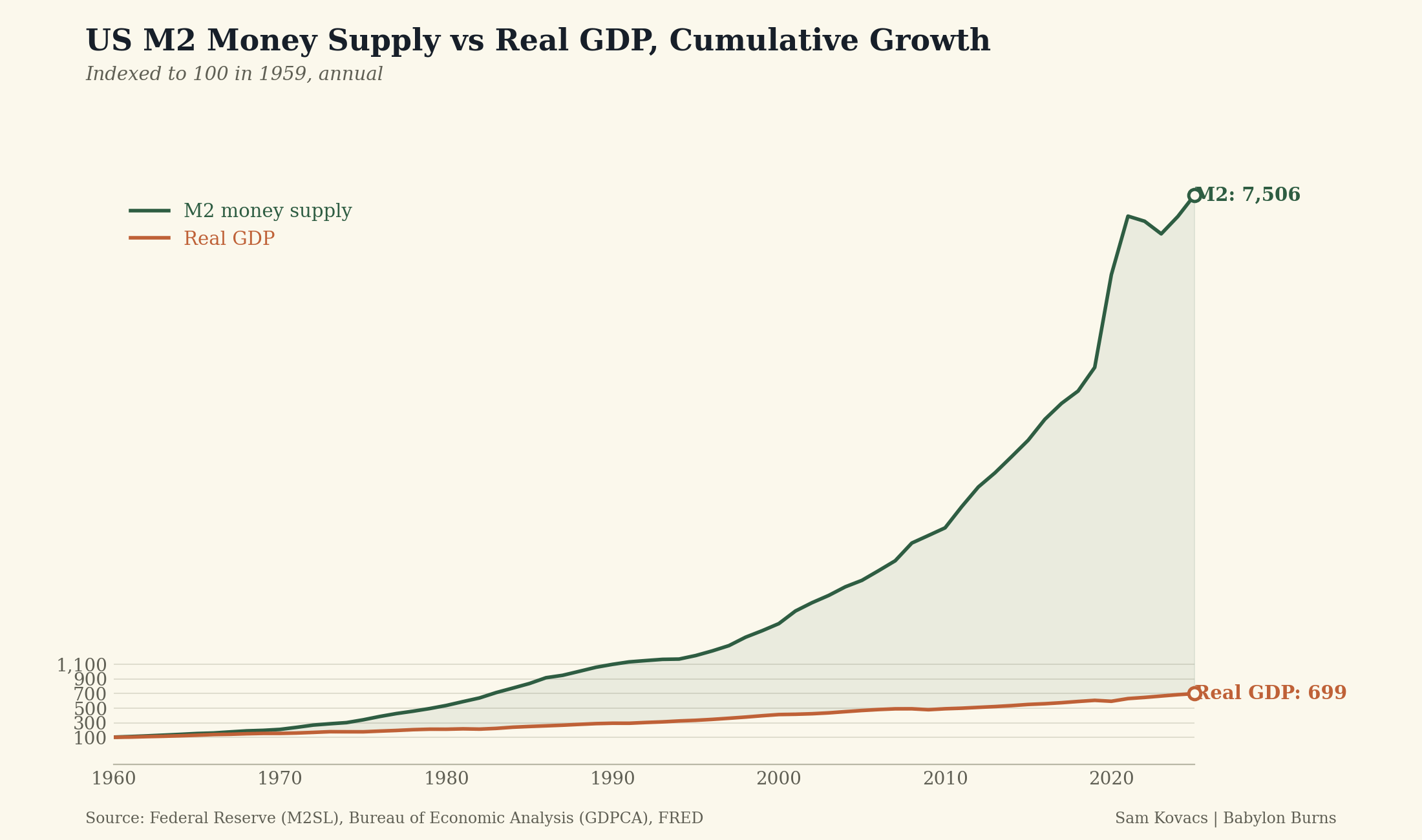

Consider that in the US, since 1959 while real GDP has 7xed, broad money (M2) has 75xed.

When we see the sharp changes in the amount of money in supply which occurred after the Great Financial Crisis of 2009, and then again in response to 2020 lockdowns, it is fair to say that those who control the money have not been doing so with your best interests at heart.

Money that is printed in excess of what the economy demands needs to go somewhere. It can go into prices (inflation), it can go into assets (stocks, gold, houses, land, bonds), or it can sit idle.

Gold is a brilliant asset to hold

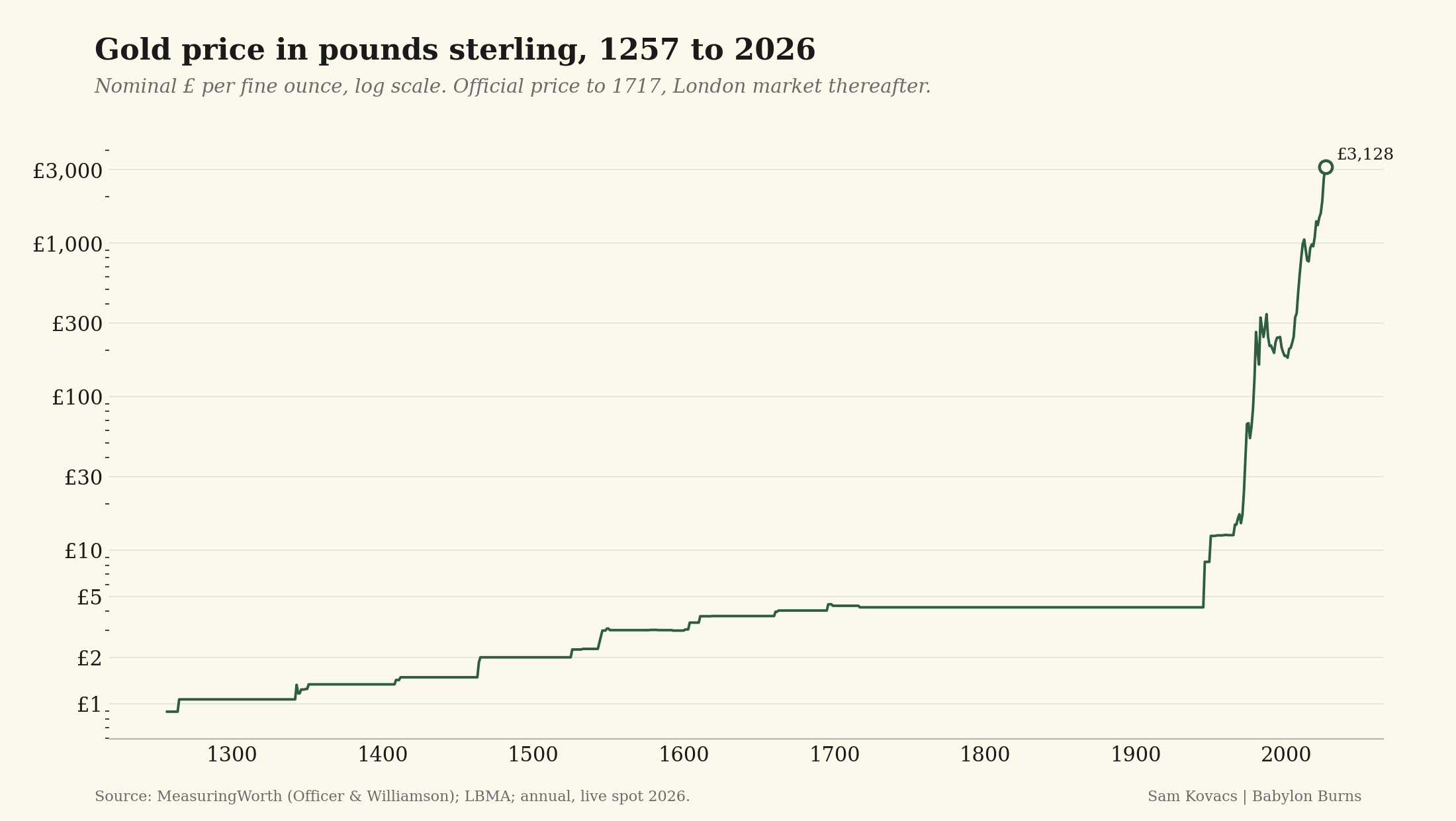

And governments debasing money is a tale as old as time. If we price gold in sterling pounds going back to 1257, we can see that that over the course of the first 500 years, gold 5xed against the pound.

Between 1971 and today, it 180xed.

I explained in my first article on Substack why governments worldwide would have no choice but to continue doing that, and why scarce assets, like gold, were imperative to hold.

Like Ray Dalio said: If you don't own gold, you know neither history nor economics.

And I do believe there is a certain amount of gold you want to hold yourself. One of the biggest draws of gold is that it has been used as currency for a very, very, long time, and that it does not depend on a counterparty.

With fiat, you depend on the corporate at which your deposits sit, and the sovereign which underwrites and dilutes the currency.

The gold bug in me believes it’s a good idea to own some physical gold: coins, jewellery, small bars, which you self-custody. This way, you depend on no other counterparty, gold you wear can move through borders more easily, and you have part of your wealth stored as a hedge against the current status quo.

But gold miners are not gold.

When I present this long term thesis and view to my peers, I am often met with the following question:

So what’s your favorite gold miner?

And they are surprised to hear that right now, my exposure to gold miners is absolutely zero.

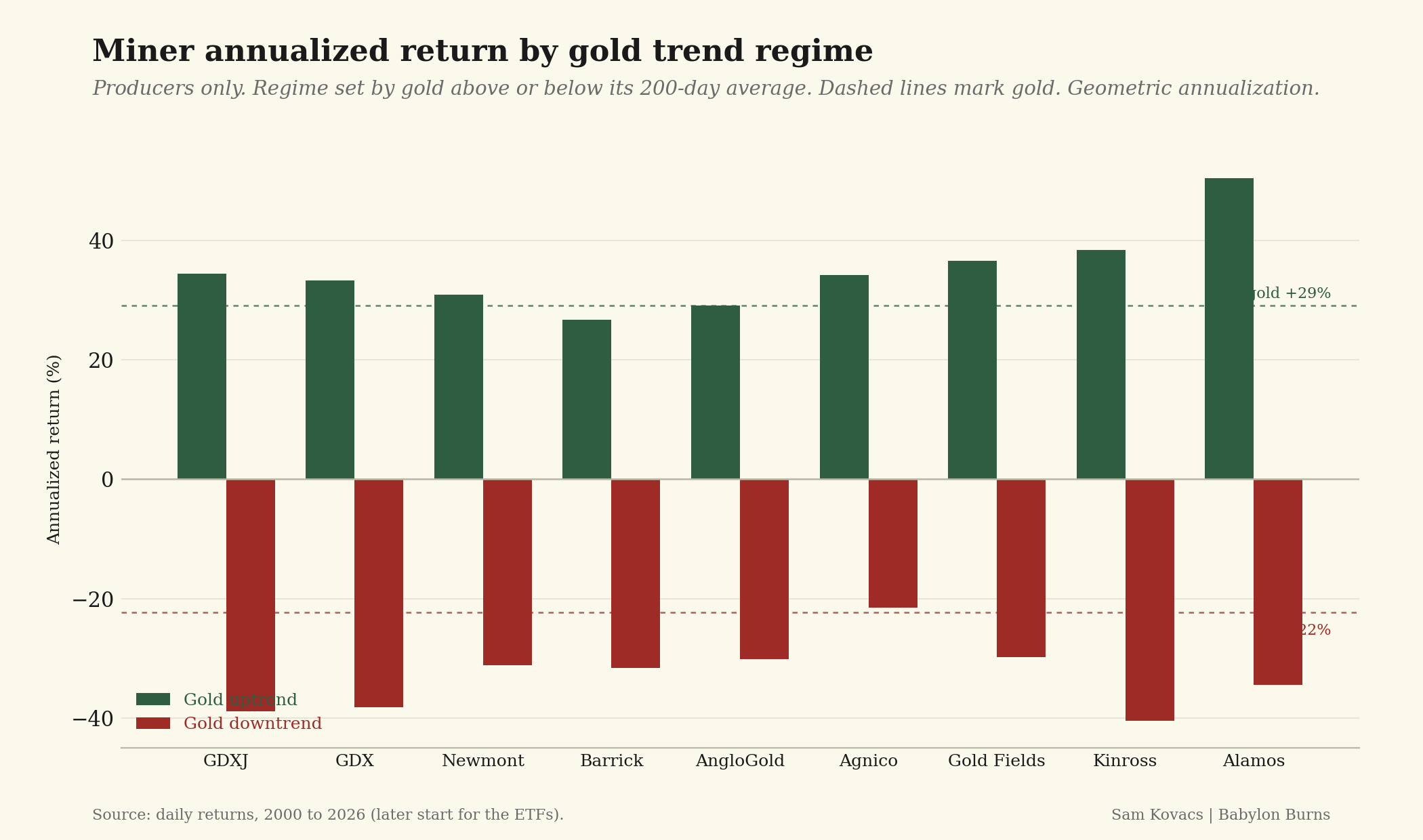

Gold miners are essentially a leveraged bet on gold which as you’ll see in this article decay when gold is either down or sideways.

A miner sells ounces of gold at market rates and spends a largely fixed amount to produce them. The spread is their margin, which bakes in considerable operational leverage, as a smaller move in gold leads to a disproportionate move in margins.

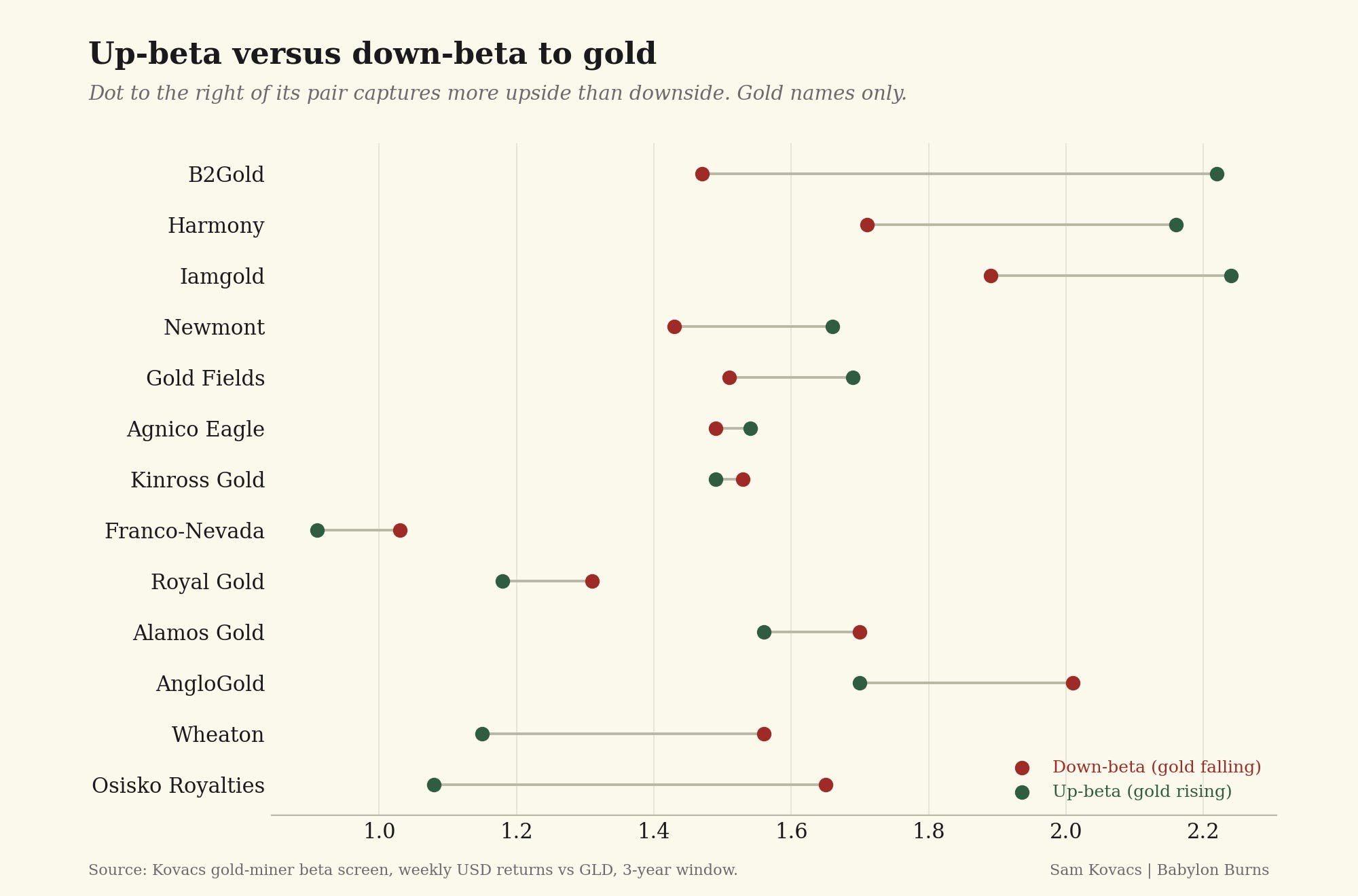

It’s no surprise then that miner ETFs have gold-betas of around 1.7x with the higher volatility names having betas of more than 2x.

In gold uptrends, miners have done better than gold, and in downtrends they tend to do worse than gold.

So you are dealing with instruments which amplify gold’s returns.

So why has holding them been a losing bet?

When you hold a gold miner, you hold a claim on its margin.

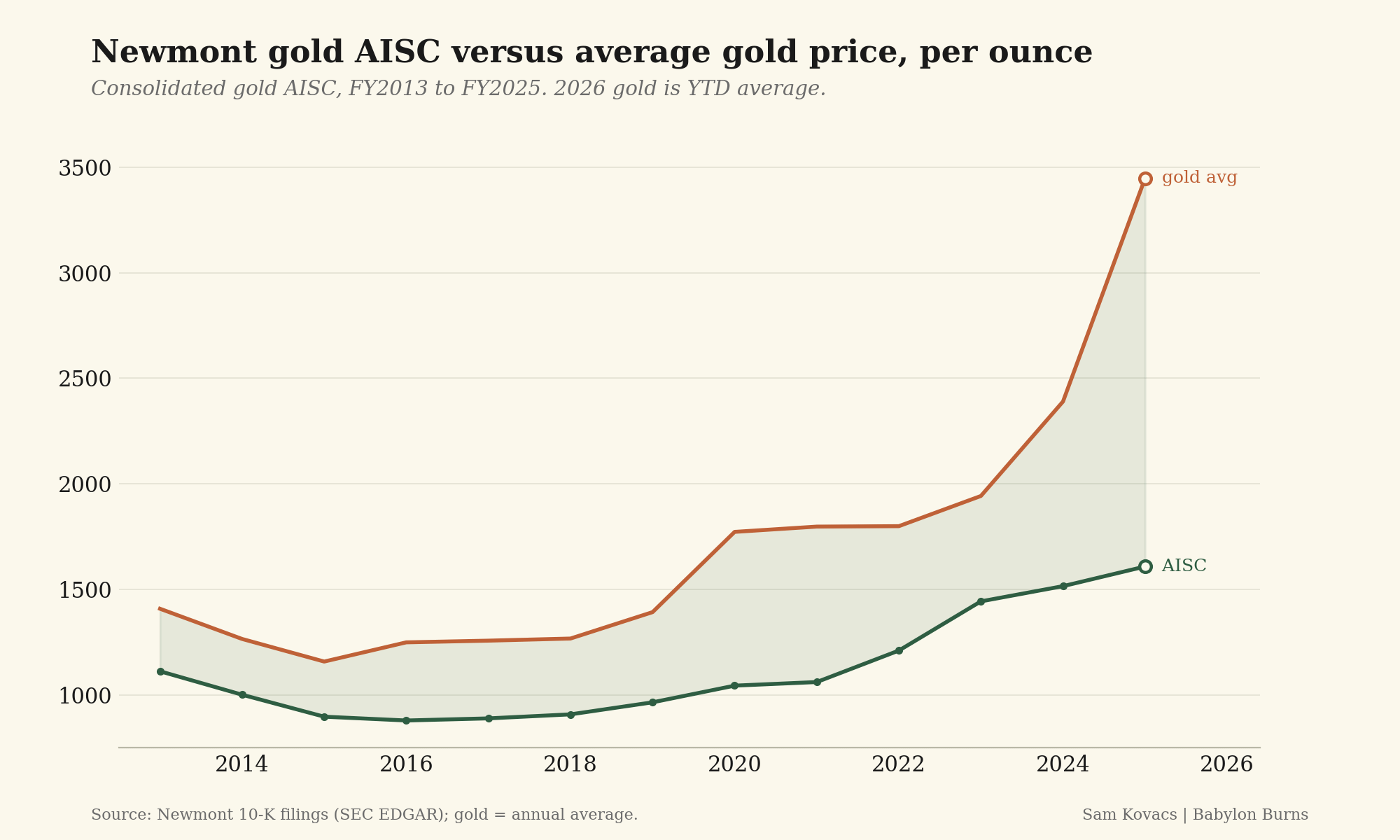

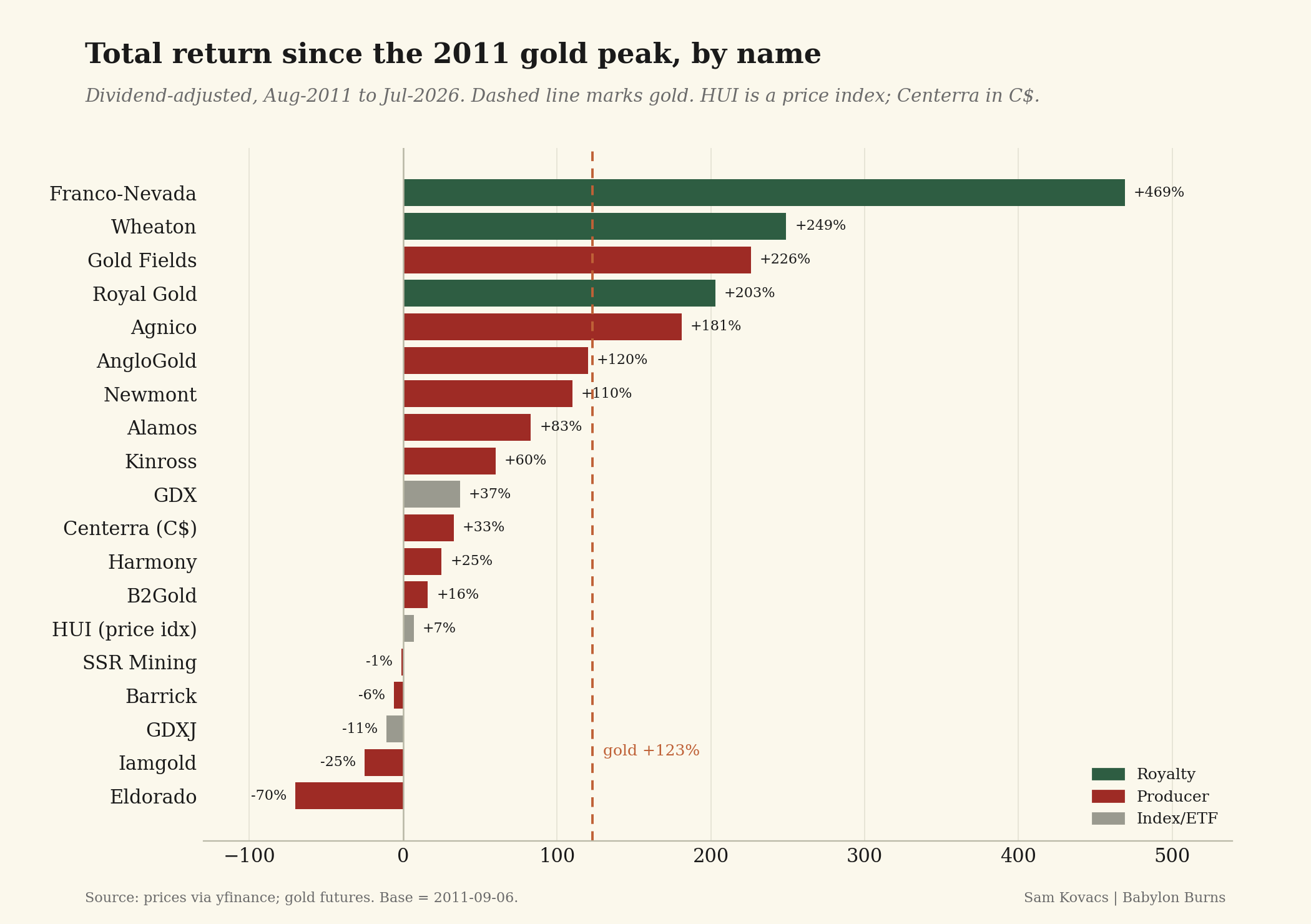

From the 2011 peak, gold price went from $1,900 to $4,100 or so today. If we look at Newmont ($NEM)’s all in sustaining cost (AISC), it went from $1,100 to $1,600. (although the concept of the AISC was first defined in 2013, the numbers still pretty much check out)

The margin went from $800 per ounce to over $2,575 per ounce. You’d think the margin exploding would imply that the stock would have returned much more than the return on gold?

Unfortunately, that would be wrong. Newmont returned 110% while gold returned 130% since the 2011 peak.

Most miners in fact, did worse than the metal, while the royalty companies did better.

Unfortunately the AISC masked things that could have gone wrong for investors and which ultimately did.

First, mining reserves deplete every year, maybe to the tune of 5-8% on average, and these need to be replenished with new assets. Growth CapEx does not make its way into AISC. In 2025, Newmont deployed $3.3bn in CapEx, but only $1.8bn got classified as sustaining. The boundary between what is sustaining and growth is blurred enough that even brownfield expansion of an existing mine can be classified either way.

So the industry standard reporting metric isn’t perfect and understates the margin.

The bigger problem is this one: Newmont’s gold production went from 5.2 million to 5.9 million in 2025, which was a 13% production increase in 14 years. Over the same time frame, share count went from 494mn to 1,068mn, so production per share actually declined by 48%.

Production is expected to decline to 5.3mn in 2026. Now to be fair to management, they are now buying back shares, and even adjusted for the hidden increase in costs and the dilution, based on prior peaks we could have expected more of a rerating than we did.

But by and far, over time, gold miners eat themselves, replacement costs more each cycle, this replacement bill gets paid with investors money, the operational leverage is diluted by increasing costs, and you’re exposed to human bias which torches cash.

Does that mean that I’d never buy gold miners?

No, and I want to be clear on this.

Gold miners are a structural losing proposition over time vs holding gold. So for passive long term investment, you want to prefer gold every single time.

But when you are riding a trend in gold, then trading miners can make sense for the amplified returns you can get versus the metal.

So when I do decide to buy gold miners for the trade, I am not so interested in buying the senior high quality ones. Buying Agnico ($AEM) gives you low-jurisdiction risk, reliable guidance, cost discipline, and defensive downside behavior relative to the sector.

All of those things are great if your plan is to hold throughout the cycle. As we have seen, there is little justification for holding gold miners throughout the cycle.

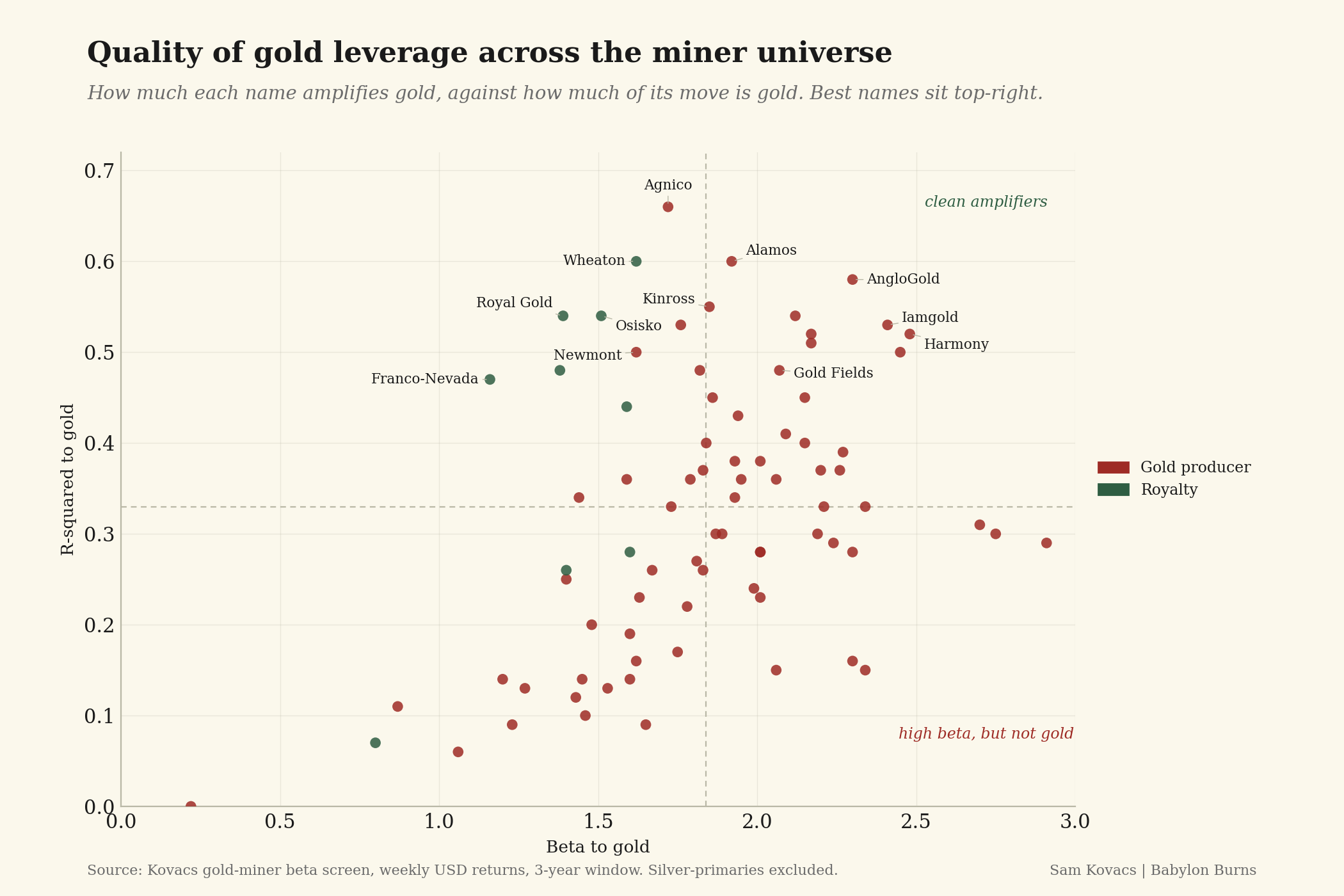

As the chart above shows, in such setups, it is the higher risk names like B2Gold, Harmony, and Iamgold which have cheap optionality embeded due to jurisdiction risk, turnarounds happening, or higher operating costs.

Beta to gold is one thing, correlation to it is the next you’ll look up. If you’re going to trade an explosive up move in gold, you want your levered miner to be as pure an expression of gold as possible. The upper quadrant of the chart above gives a decent universe to work from.

And I know someone is going to say “but gold miners are exceptionally cheap, and printing cash at the current rates.”

Yes that’s true. But as a trade, they are ultimately just gold beta, and in an environment where gold remains sluggish or trades sideways, they might be dead cheap, they’ll also be dead money.

What would it take to go long these miners?

For me to get excited about investing in gold miners, I would need to see movement in gold.

How do you value gold? Difficultly.

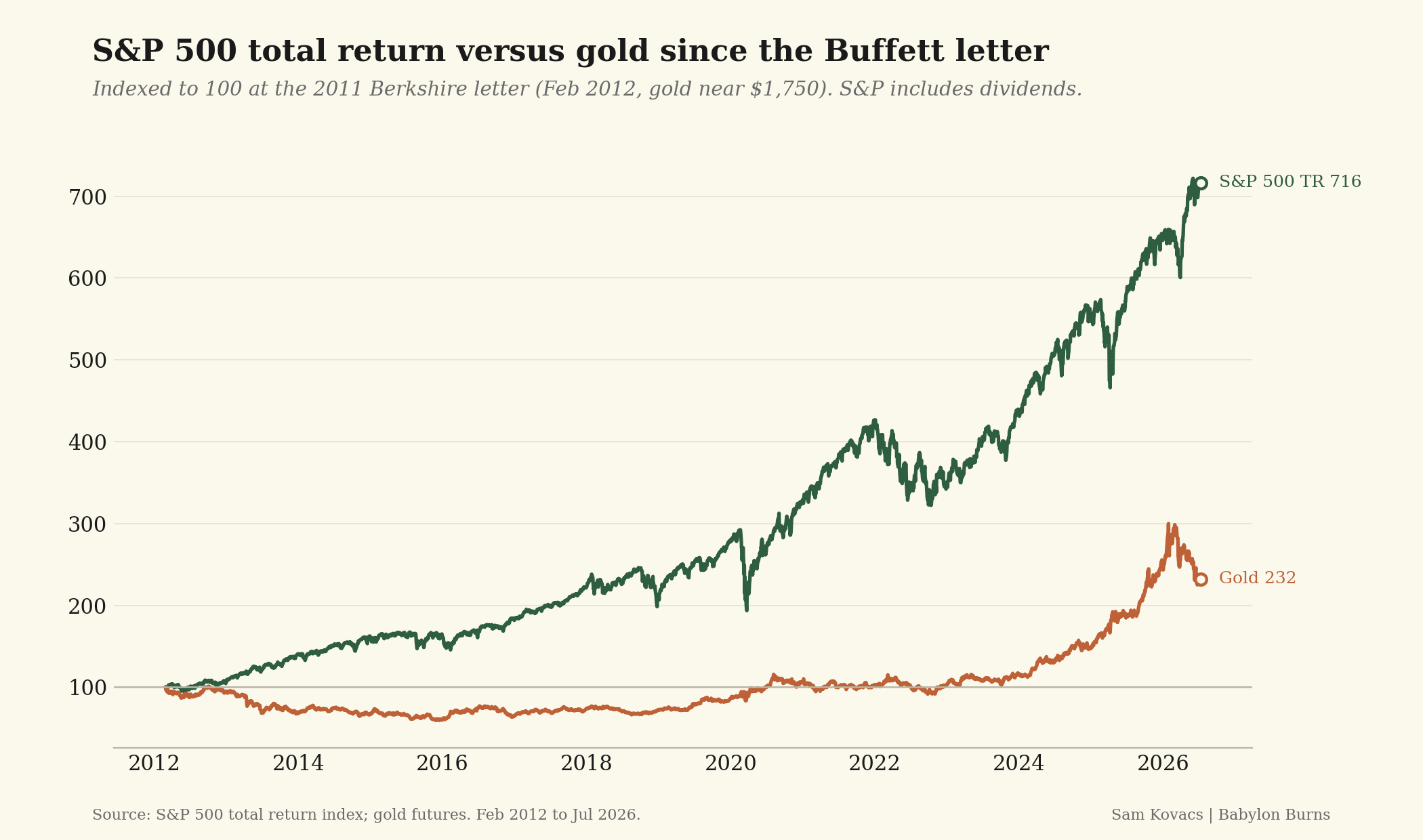

In Berkshire’s 2011 annual letter, Warren Buffett tried to do so with the following thought experiment.

Today the world’s gold stock is about 170,000 metric tons. If all of this gold were melded together, it would form a cube of about 68 feet per side. (Picture it fitting comfortably within a baseball infield.) At $1,750 per ounce – gold’s price as I write this – its value would be $9.6 trillion. Call this cube pile A. Let’s now create a pile B costing an equal amount. For that, we could buy all U.S. cropland (400 million acres with output of about $200 billion annually), plus 16 Exxon Mobils (the world’s most profitable company, one earning more than $40 billion annually). After these purchases, we would have about $1 trillion left over for walking-around money (no sense feeling strapped after this buying binge). Can you imagine an investor with $9.6 trillion selecting pile A over pile B?

-Warren Buffett, 2011 Berkshire Hathaway Shareholder letter

He was obviously vindicated as the S&P 500 did a lot better than gold did since then.

Gold is not productive. It is a function of fear, and a function of a reduction in value of the thing it’s measured in: dollars.

And gold works in spurts. It does nothing for a while, then it has a massive leg up..

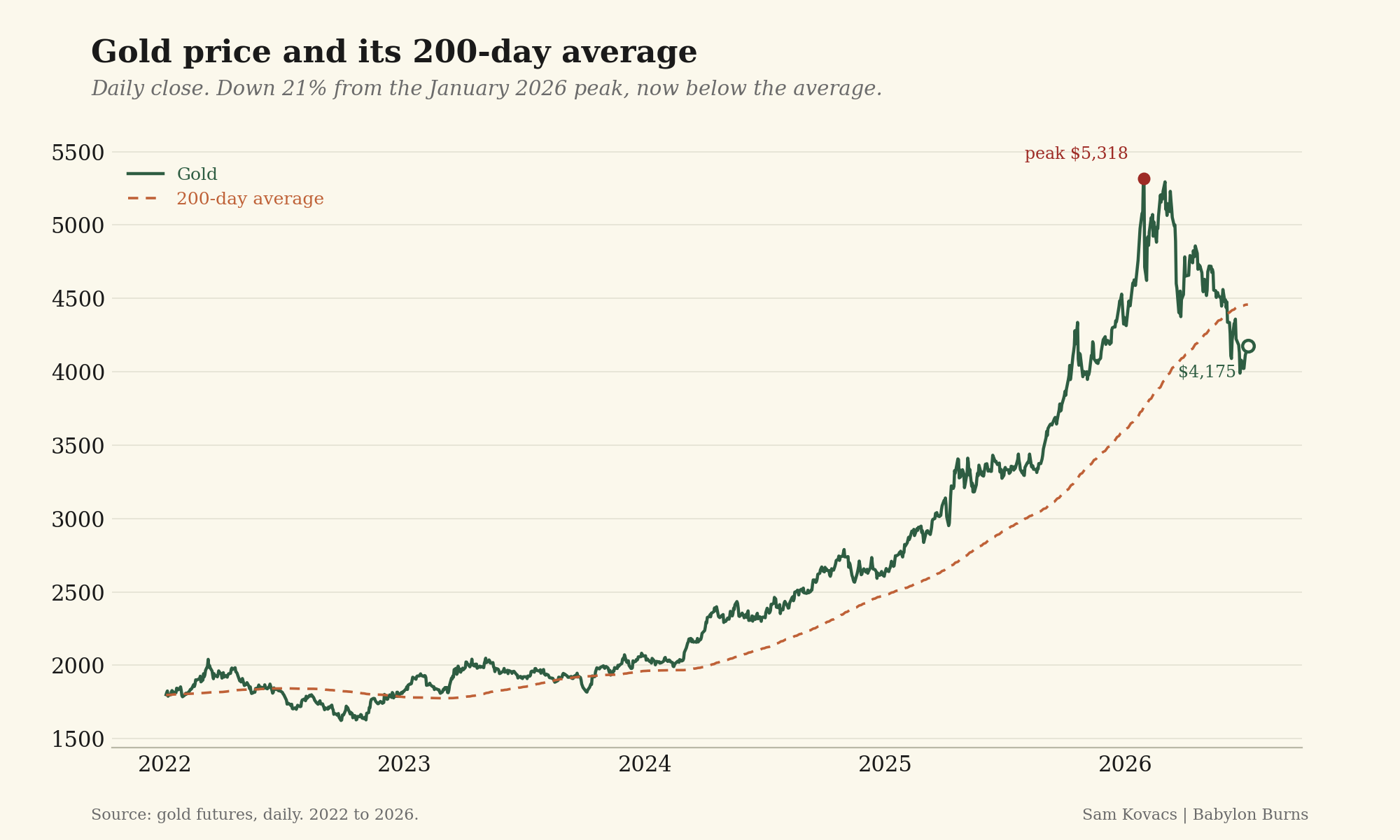

And recently, it reached a peak, rolled over, and dipped below its 200 day moving average.

In an interview in 2014, Paul Tudor Jones once said:

“My metric for everything I look at is the 200-day moving average of closing prices. I’ve seen too many things go to zero, stocks and commodities. The whole trick in investing is: “How do I keep from losing everything?” If you use the 200-day moving average rule, then you get out.”

The 200 day moving average isn’t a perfect line in the sand, but it can be comfortably used as a gauge of: is something trending or not?

And the answer here is no.

Technical analysis is beautiful for assets which can be difficultly valued because the chart gives us a pictorial record of the tug of war between buyers and sellers.

As Richard Schabacker, the modern founder of technical analysis said:

In the record of such trading all of these many and varied fundamental factors are brought to bear, are evaluated and automatically weighted and recorded in net balance on the stock chart. The trading in any stock is largely the result of the influence these fundamental factors have had on each buyer and seller of each share of stock. The stock chart is a pictorial record of such trading, so that it, in itself, is a reflection of all those other factors and, from a purely technical standpoint, need therefore concern itself no further with such fundamental considerations

I like to look at formations which build up over time. That’s where technicals prove value to me, as they give me a good idea of the general sentiment towards an asset.

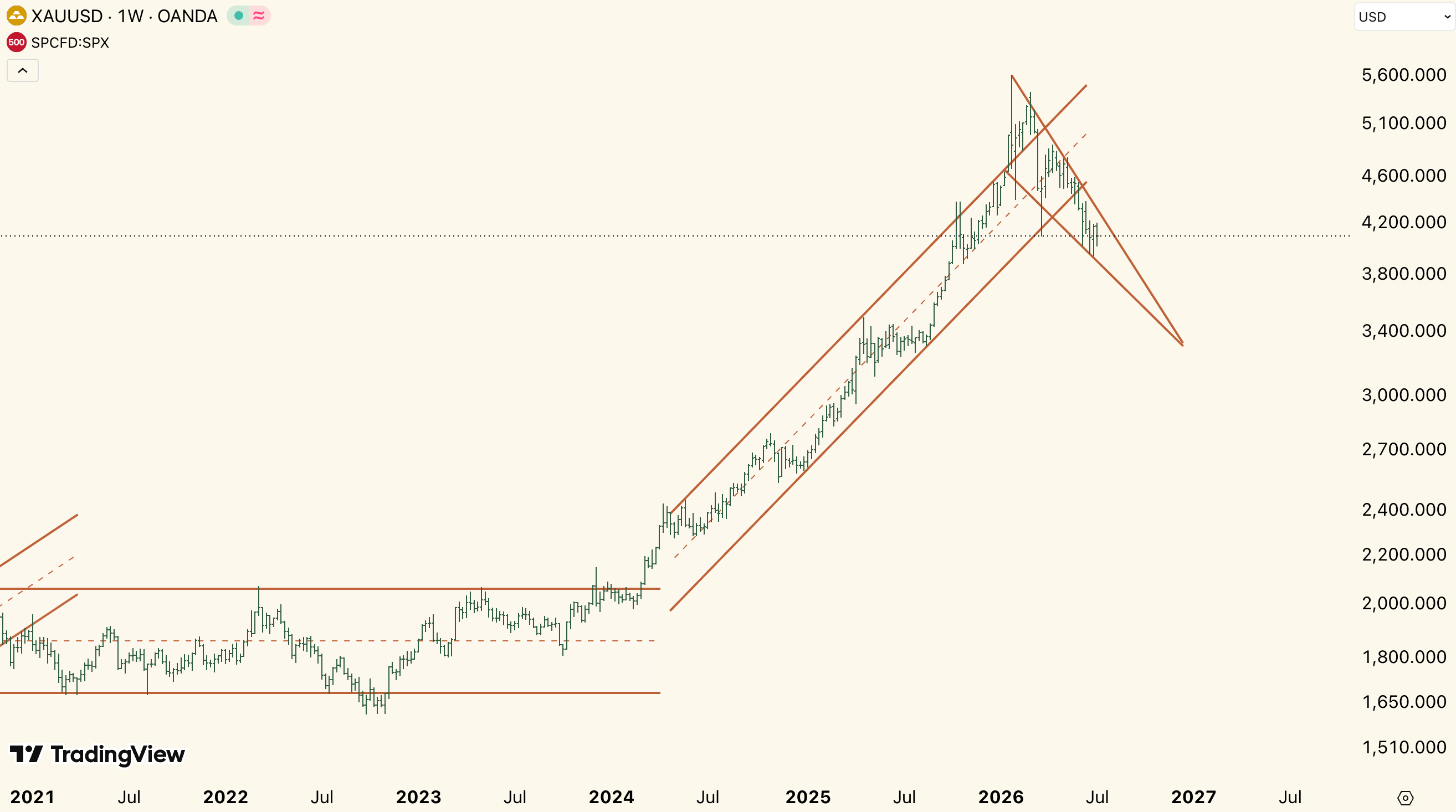

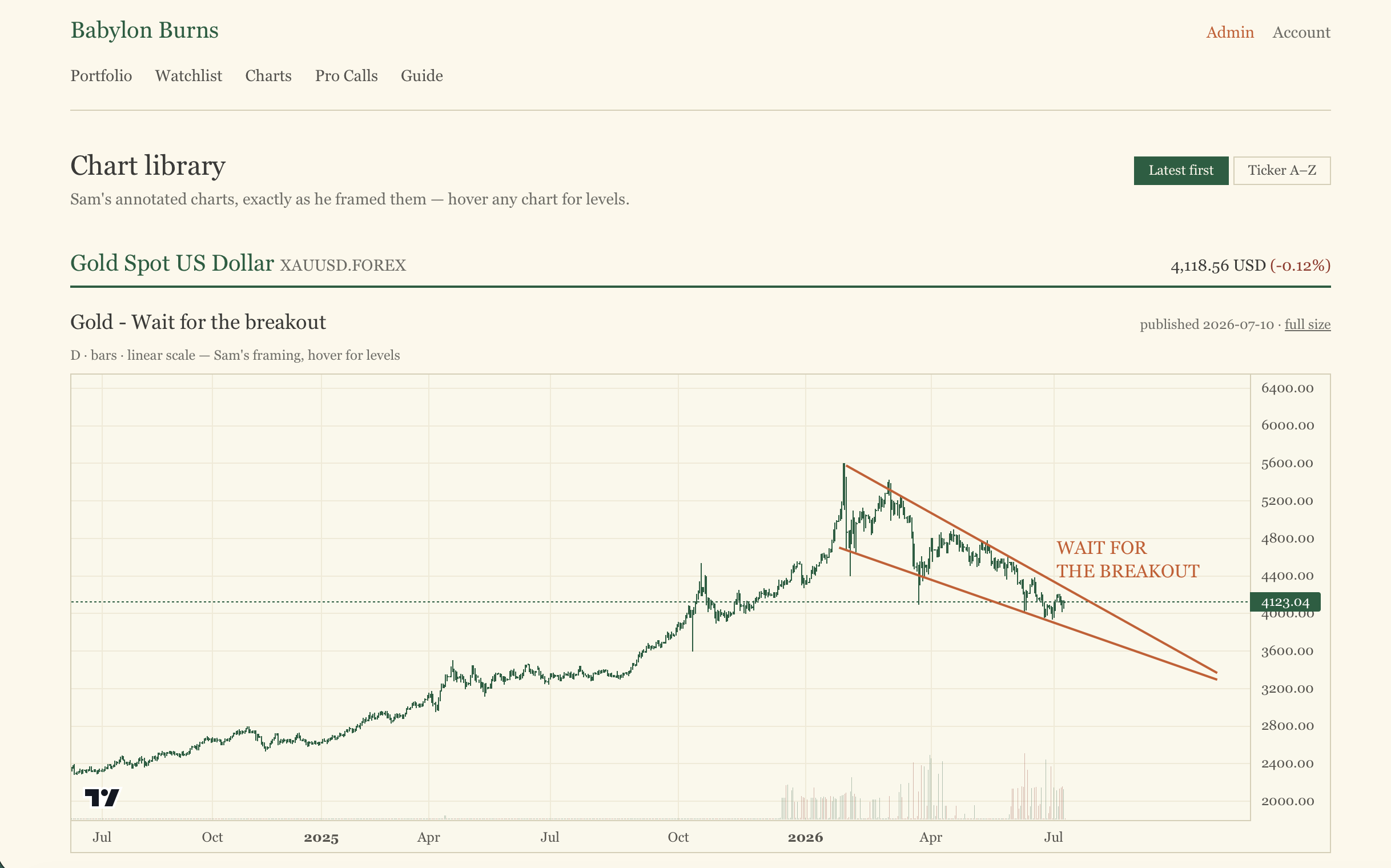

And Gold was basing in a rectangle between 2021 and 2024, mostly between $1,700 and $2,050. Then in 2024, it broke out and commenced a bullish ascending channel which brought it all the way to a blow of top at $5,318 on January 30th this year, just as Kevin Warsh was nominated chairman of the Fed.

Since then, it broke out of that channel (around the same time it broke below its 200 day moving average, which is interesting confluence), and has been forming a down-turned wedge ever since.

Here’s the good news: Down turn wedges are reversal patterns, so once they resolve, we expect the previous trend (up) to resume.

Here’s the bad news: They usually resolve very slowly, often staying within the formation until the apex is reached. And once a breakout happens, they tend to move horizontally for a while before a clear trend resumes.

You can view this as a period of lull when buyers and sellers are uncertain of quite where the asset is headed after a strong impulse up, and an aggressive correction down.

On the topic of this formation, Schabacker said:

“It presages a reversal of trend, but the move is delayed for an indefinite period in the case of many Down-turned Wedges. The practical trader will therefore take prompt action when his chart shows a breakout from an Up-Pointed Wedge Top; whereas he may safely delay action at a Bottom until the price and volume action indicate that the new uptrend is really started."

This formation could continue to play out until the fourth quarter this year, and the climb back from there could be slow for a long period of time.

Given that we have assessed that gold miners do well only during gold up regimes, we can comfortably conclude that for the time being, we don’t want to touch them with a 10 foot pole.

To be clear, technicals are not forecasts, nor do they inform us of probabilities, they only give us possibilities. And the possibility which is being painted by the current record is one where it will take a while before gold makes new highs.

Will I let you know when I change my mind?

Yes of course, that is why I’m launching this newsletter. On August 15th, on the 55th anniversary of Nixon moving away from the Gold standard, I will launch the paid version of Babylon Burns.

In the meantime until then I will be giving you a weekly drip of (I believe) high quality articles 100% free. You just need to put your email in below if you haven’t already.

Once I launch the paid version, for annual subscribers, it will include a web and mobile application with the portfolio, the watch list, and a custom chart library with my takes on assets, stocks, and so on, and the formations I am waiting to enter into positions.

I am getting clearer on what the offering will be although this isn’t set in stone yet.

The monthly tier will be priced higher, as I don’t think these newsletters are made to be followed monthly.

The annual tier will be priced between $299 and $499 and include the app mentioned above.

The Pro tier will be priced between $1,000 and $2,000, will be limited in spots, and include a quarterly call with me, a signed copy of my upcoming book and other perks.

For the time being, I have left the pledges well below those levels, as I want to do a little something for early readers and people who get with the program early.

So if you decide to pledge to a subscription now at the lower rates, I’ll honor those for you when we go live, even if the official rate is way higher.

In the meantime, please share this with anyone you think might benefit from reading it.

As Babylon burns, we’ll light the cigars.